Those who follow the agricultural industry will be aware of the increasing attention that agriculture technology (AgTech) firms are receiving, and with it, significant investment dollars. In fact, one of Canada’s largest institutional investors, the Ontario Teachers’ Pension Plan (OTPP) recently made its first AgTech investment through its venture capital arm, Teachers’ Innovation Platform. With the spotlight on the AgTech industry, we wanted to review the role that technology has played in agriculture and explore how ongoing innovation can drive industry performance through the lens of a farmland owner / investor.

Technology in Agriculture: A Driver of Productivity & Farmland Values

Innovation and technological advancements in agriculture have been around for as long as farming itself. The search for increased efficiency to meet growing consumer demands is not going away and significant technological advancements have been made in the agriculture industry over the past several decades. Today, technologies such as GPS Guidance for farming equipment and Site-Specific Crop Management practices allow farmers to be more precise and efficient in crop production. As a farmland owner, this raises a key question: how do technological advancements affect producer income and subsequently, farmland values?

For a conventional crop producer, farm income is a function of underlying commodity prices, expected crop yields, and the cost of crop production. Commodity prices are determined by the global market and, while producers can use certain marketing strategies to help reduce risk, individual producers cannot ultimately influence commodity prices. As such, farm operators looking to improve productivity, and thus profitability, can be better served by finding ways to boost crop yields and lower production costs to increase income.

Since farm incomes are a key driver of farmland value, the result of sustainable increases in overall farm profitability can be seen through appreciation of farmland values, making new advancement in AgTech interesting for not only the farm operator but the farmland investor as well.

Examples of AgTech Areas of Focus

Plant Breeding

While longer growing seasons resulting from climate change certainly play a role in increasing crop yields in certain geographies, advances in agricultural technology are also widely acknowledged as being a major driver of improved yields. Notably, there have been significant advancements in plant science and breeding over the past 30 years. Varieties of certain key crops, such as corn, soybeans, and canola can be engineered to mature over a specific number of growing days to accommodate local growing conditions and allow farmers to plan for crop maturity at desired times, or to be more resilient against certain diseases. This allows farmers to select and seed optimal plant varieties that are best suited to their location and the characteristics of their land.

Precision Agriculture

Precision agriculture (also referred to as Site Specific Crop Management) uses aerial and satellite imagery, weather data, and crop health indicators to enable farmers to be more exact in the planting of seeds and the application of fertilizer. For example, variable-rate fertilizer application allows producers to apply the ideal amount of fertilizer to different regions of a single field to maximize crop health and avoid unnecessary overuse of fertilizer. Beyond increasing crop yields, this technology also has considerable benefits from an environmental perspective as it reduces the overall amount of fertilizer required thus preserving supply and limiting unnecessary run-off. Other technologies, such as GPS guidance, have allowed for more accurate planting of crops and fewer wasted acres.

Larger, More Efficient Machinery

Technological advancements have also created significant cost savings in agriculture, and farming operations are larger and more efficient than ever. This is made possible by new technologies such as the large machines that allow producers to plant, fertilize, and harvest greater acreage in less time. Today, large tractors with planting implements spanning over 60 feet in width can cover over 300 acres in a single day, whereas the smaller 15-foot no-till drills of the past would have taken more than four days to cover the same amount of land.

What This Means for Farmland Values

Technological advancements have helped producers to increase yields, reduce costs and have ultimately had a positive impact on farm income and farmland values. As noted in our Q1 newsletter, there has been much excitement in the Canadian farmland market in the first half of 2021, attributable to commodity prices rising to multi-year highs, low transactional activity in 2020, and the prolonged low interest rate environment. However, these factors are cyclical and can shift in a relatively short period of time. In contrast, activities by farm operators and the agriculture sector as a whole, to develop and implement new technologies, increase yields, manage costs, and reduce their environmental footprints are something we believe will support the ongoing capital appreciation of Canadian farmland.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

We are often asked what sets Bonnefield apart as a leading Canadian farmland manager. While there are many qualities that come to mind (our strong 10+ year track record, institutional quality reporting and administration, and our sale-leaseback model that attracts leading farm partners, just to name a few), diversification is one of the most obvious.

Geographic diversification has been a central theme in Bonnefield’s investment thesis since the firm’s inception over a decade ago. As Canada’s leading farmland investment manager, we invest in more Canadian provinces than any other Canadian agriculture-focused asset manager. We apply a granular approach to diversification, investing in over 30 unique growing regions across the country, and ensuring portfolio diversification across multiple climatic regions, crop types and tenant relationships.

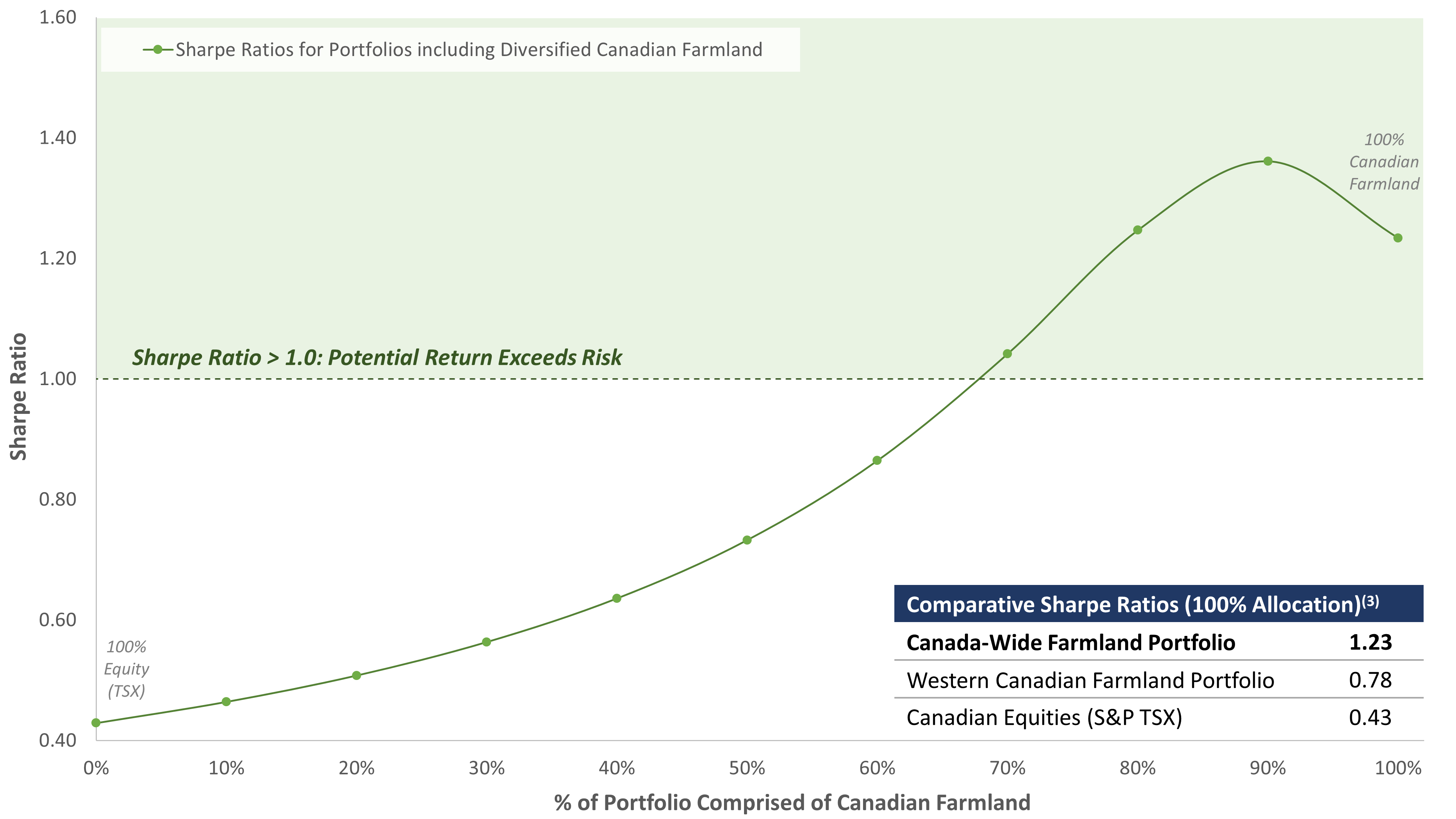

Assessing Risk & Return: Sharpe Ratio Analysis

To illustrate the value of diversification in an investment portfolio, we conducted a Sharpe ratio analysis(1) using historical Canadian farmland values between 1985-2019. This type of analysis is a staple of portfolio management theory and a relative measure of the trade-off between risk and return. A higher Sharpe ratio typically suggests a higher potential return per unit of risk taken on and therefore, many investors focus on improving / maximizing the Sharpe ratio of their portfolios.

Risk-Return Profile: Diversified Canadian Farmland in a Portfolio (Sharpe Ratio Analysis)(2)

The first takeaway from this analysis is the positive impact on the Sharpe Ratio as a result of increasing the allocation to Canadian farmland (regardless of its diversification) as opposed to holding only publicly traded equity. With its historically stable return profile, Canadian farmland reduces the volatility of returns and, therefore, improves the Sharpe ratio.

The second takeaway is the relative benefit of holding a portfolio with greater diversification amongst its farmland holdings. As seen in the chart above, portfolios consisting of farmland diversified across most provinces in Canada (Bonnefield currently invests in BC, AB, SK, MB, ON, NB, and NS) demonstrate higher Sharpe ratios, indicative of a favourable risk‐return trade-off, compared to those with farmland limited to only the prairie provinces. This illustrates the relative benefits of maximizing potential diversification within the farmland portfolio.

As noted in our Q1 2020 Newsletter, the Canadian agricultural community has been optimistic since the beginning of 2021 given:

The backdrop of increased feed demand from China;

The reduced crop supply from Brazil and Argentina; and

The Russian export tax on wheat.

Combined with a prolonged period of low interest rates, relatively low transactional activity for Canadian farmland in 2020, and the current multi-year high commodity prices for key crops, we continue to believe that Canadian farmland values are poised for an exciting period of strong growth.

As investors explore the benefits of Canadian farmland within their investment portfolios, we encourage them to consider the relative value of exposure to a well-diversified farmland portfolio to minimize volatility and maximize your potential risk-adjusted returns.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

(1) Sharpe ratios represent a relative measure potential returns compared to potential risk of an investment, and are calculated by dividing i) the excess return above a selected risk-free rate (i.e., average historical rate of return for an asset/investment less a risk-free rate such as the prevailing rate for a Government or Treasury-issued instrument) by ii) the standard deviation of those historical returns.

(2) Analysis contemplates hypothetical portfolios balanced between i) Canadian equities (S&P TSX index) and ii) Statistics Canada farmland values (weighted equally between selected provinces; Bonnefield’s investment provinces include BC, AB, SK, MB, ON, NS, and NB), between 1985 and 2019.

(3) Noted Sharpe ratios assume 100% allocation of a hypothetical portfolio to each of i) Canadian farmland in Bonnefield’s investment provinces, ii) Canadian farmland in AB/SK/MB only, and iii) Canadian equities (S&P TSX index).

Over the past decade, we have seen increased interest among the investment community in agriculture and farmland as an asset class. Not only are large, sophisticated, institutional investors across the globe evaluating (or already invest in) farmland and agricultural investments, so too, are increasing numbers of non-institutional investors.

Click here to read an article by Bonnefield’s Andrea Gruza that explores how farmland investments provide investors with a diversifying asset with strong ESG characteristics, climate change hedging capabilities and potential to support a move towards a net zero investment portfolio.

(Original article published in the spring 2021 edition of Radius European Investment Journal.)

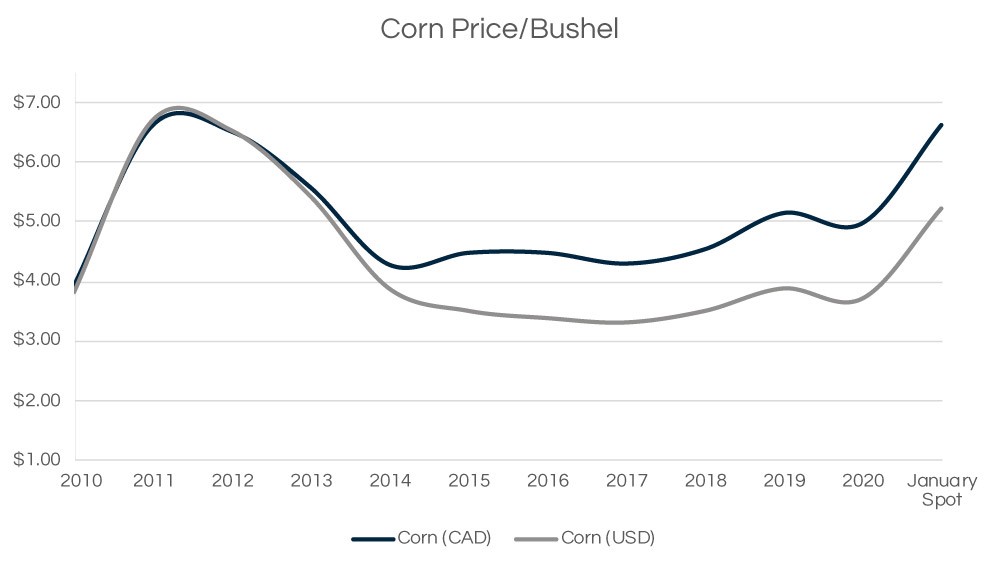

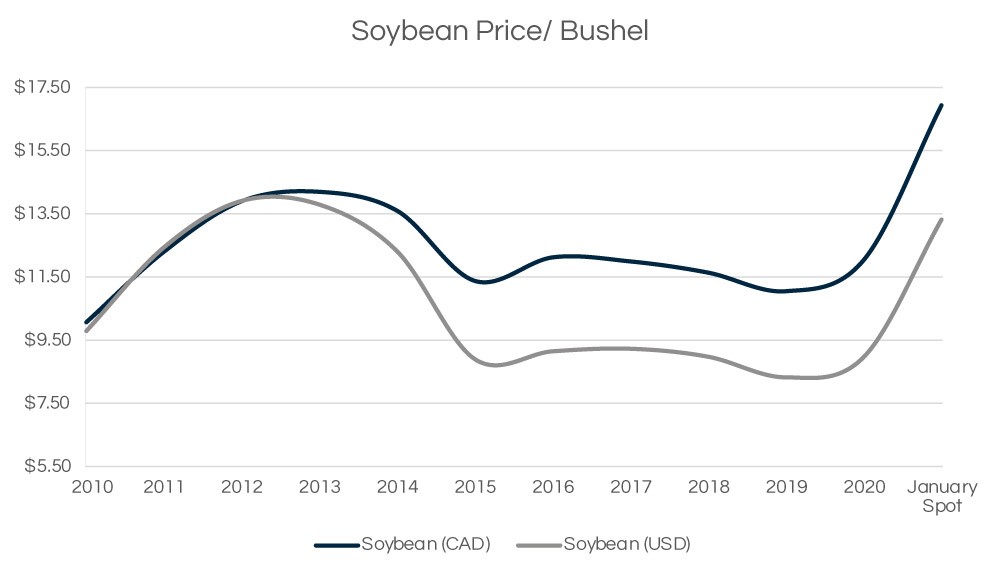

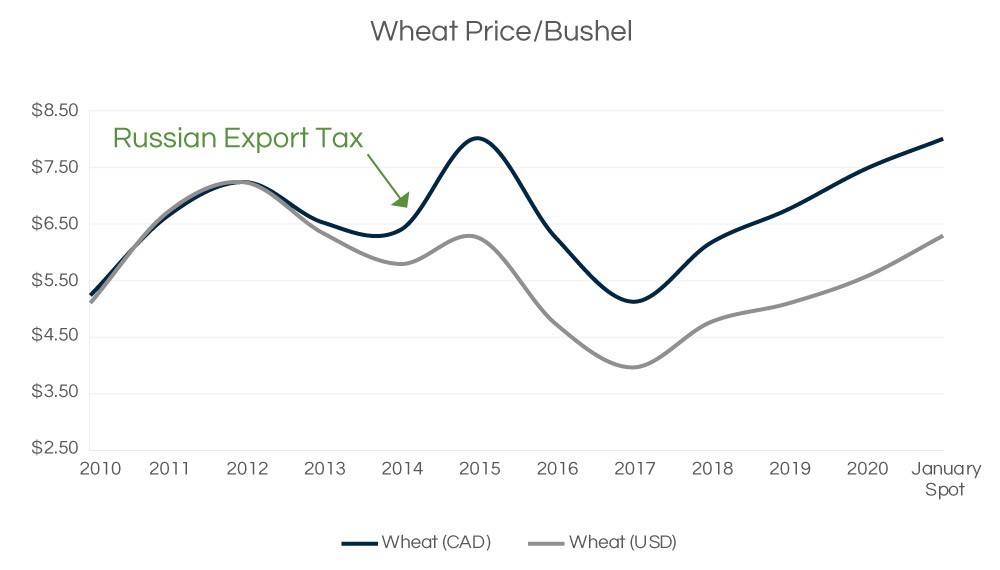

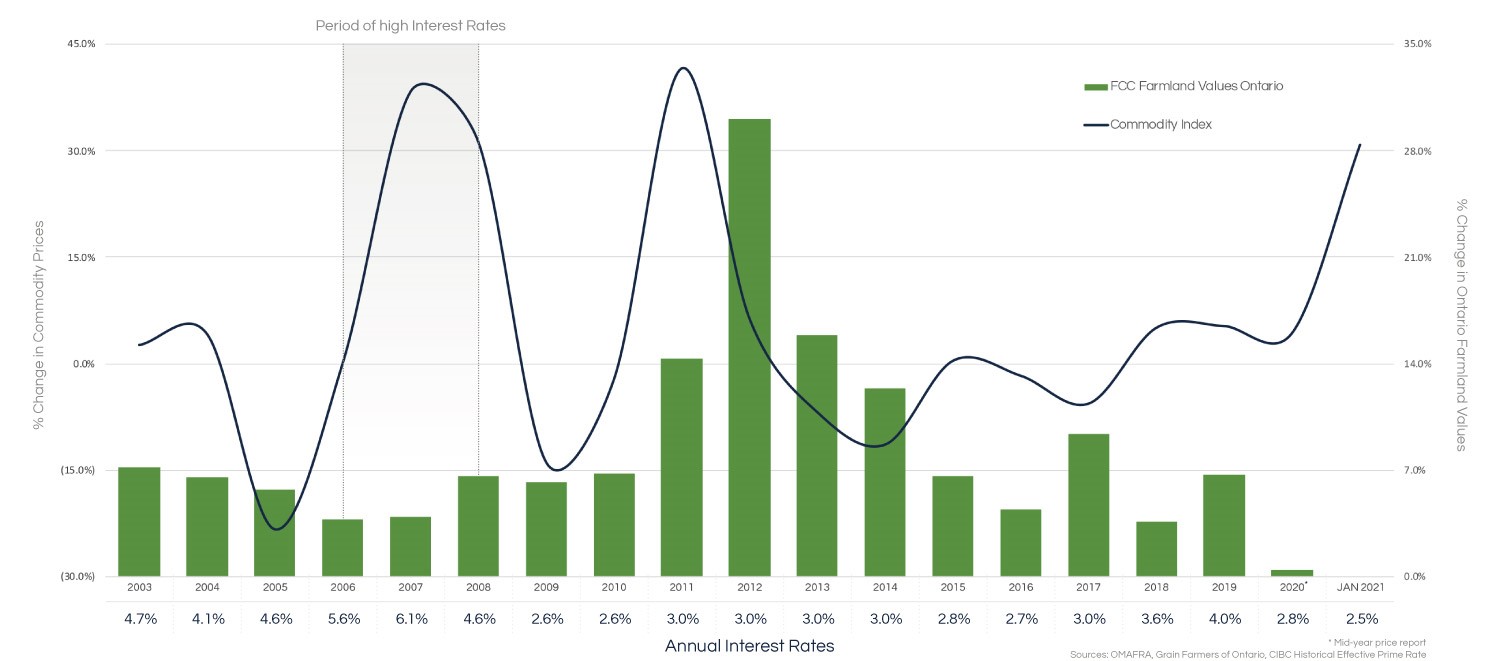

The mood in much of the Canadian agricultural community has been positive lately. Following several years of depressed agricultural commodity prices, there is a significant rebound in prices across multiple commodities. The last time we saw similar commodity price growth, combined with low interest rates was in 2011 which marked the beginning of several years of double digit increases in farmland values. While there is no guarantee that we will have the same outcome, the signs are very encouraging.

1. Increased Demand from China

The catalyst for this rebound has been a massive increase from China for feed, as it rebuilds its hog herds following the devastating impacts of the 2018 swine flu that resulted in a ~60% reduction of the country’s breeding sows by the second half of 2019 (1). We expect that the increase in demand from China should be longer lasting as it will likely take two to three years to rebuild the pig herds back to pre swine flu levels.

2. Severe Drought in South America

A severe drought in South America since last October drastically reduced supply from Brazil and Argentina – two major corn and soybean producers. While this offers short-term support to pricing, recent rains in the region should provide positive conditions for the current harvest.

3. Russian Export Tax on Wheat

Finally, prices are also seeing an impact from a recently announced export tax that Russia placed on its wheat producers in an attempt to reign in recent domestic food price inflation resulting from COVID-19. In 2015, this had a major impact on global wheat supply. We expect a similar impact this year with wheat prices increasing materially.

Sources: OMAFRA, Grain Farmers of Ontario

Commodity Price Impact on Farmland Values

Given the magnitude of recent commodity price increases we took a look back to see what effect commodity prices have had on farmland values historically. Two notable characteristics emerge from this analysis.

1. Significant upside potential for farmland values resulting from a combination of high commodity prices and low borrowing costs.

This creates a favourable environment whereby farm profitability increases, leaving farm operators with more cash in their pockets. The combination of greater cash on hand and low borrowing costs facilitates an increase in farmland acquisitions. Having this combination of factors is important because, as we saw in 2007, an increase in commodity prices against the backdrop of high borrowing costs, did not see meaningful farmland value increases.

2. Farmland values have had historical downside protection through several years of significant commodity price decreases.

Not only have farmland values failed to track the declines in commodity pricing, they have actually continued to increase in value (albeit at a slower rate in years of significant commodity price declines.) This trend can be attributed to the favourable supply and demand dynamics that exist due to a limited supply of global arable farmland with an increasing demand for food. From 1961 to 2016 there was a 48% decline in hectares of arable land per person (2). This is attributable both to a growing population as well as a decline in total arable land from desertification and urbanization.

It is evident, based on historical analysis, that commodity prices can influence farmland values through enhanced farm profitability. Based on our experience of the last two decades, that influence is far more significant on the upside than it is on the downside.

What This Means For Farmland Values

While there is always potential for unforeseen events to arise, a review of current market conditions provides support for a positive outlook on farm prices. The combination of increasing commodity prices and low borrowing costs shows the potential for a return to farmland valuations reminiscent of the early 2010’s.

A Note on the Analysis

We focused our analysis on Ontario using the three main cash crops grown in the province: wheat, soybeans, and corn. According to data from the Ontario Ministry of Agriculture, Food and Rural Affairs (“OMAFRA”), these three crops represent roughly 71% of the total cropland in Ontario based on seeded acres which makes this a meaningful, albeit simplifying, analysis for evaluating general trends in the province. In addition to commodity prices, we have also included the prime rate as a proxy for farmers’ borrowing costs, as this also has a significant influence on land values. The graph above illustrates the annual percentage change in commodity prices and Ontario farmland values against the prime rate. To capture historical commodity prices, we used a hypothetical commodity price index comprised of 40% soybeans, 40% corn and 20% wheat. This is representative of a typical five-year rotation for an Ontario farmer of two years planted to corn, two years planted to soybeans and one year to wheat.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

Bonnefield’s Vice President of Capital Markets Andrea Gruza joined host Robert Arnason on the Between the Rows podcast recently to discuss ESG Investing and its relevance for Canada’s agricultural sector.

“ESG investing isn’t necessarily a widely agreed-upon term and the definitions and parameters around ESG in the investing community really are evolving. It stands for environmental, social and governance factors. The term certainly has become pretty widely recognized and adopted across multiple industries over the last few years, not just within finance, and you’re hearing [it] from the majority of large sophisticated investors across the globe.

“I think everybody’s situation is unique and I can’t speak [for] all farmers across the country, but I don’t think ESG is [just] a trend. I can imagine the terminology around ESG evolving and the set of considerations for each industry changing over time as it better reflects what’s happening in the world around us. I think that as we learn more, we’re more aware of what things we should be thinking about when we evaluate how a business is performing.

Listen to the podcast and full interview below, or by clicking here.