The topic of food security has gained prominence through 2022 and has highlighted the important role that Canada will play in meeting future demands for food production.

Clickhere to watch the team at Bonnefield discuss this important issue in a discussion moderated by Catherine Marshall of Real Alts.

We are often asked about farmland lease rates across Canada as well as the relationship between lease rates and farmland value. This recent publication from Farm Credit Canada (FCC) provides an interesting overview of the topic.

We are often asked what sets Bonnefield apart as a leading Canadian farmland manager. While there are many qualities that come to mind (our strong 10+ year track record, institutional quality reporting and administration, and our sale-leaseback model that attracts leading farm partners, just to name a few), diversification is one of the most obvious.

Geographic diversification has been a central theme in Bonnefield’s investment thesis since the firm’s inception over a decade ago. As Canada’s leading farmland investment manager, we invest in more Canadian provinces than any other Canadian agriculture-focused asset manager. We apply a granular approach to diversification, investing in over 30 unique growing regions across the country, and ensuring portfolio diversification across multiple climatic regions, crop types and tenant relationships.

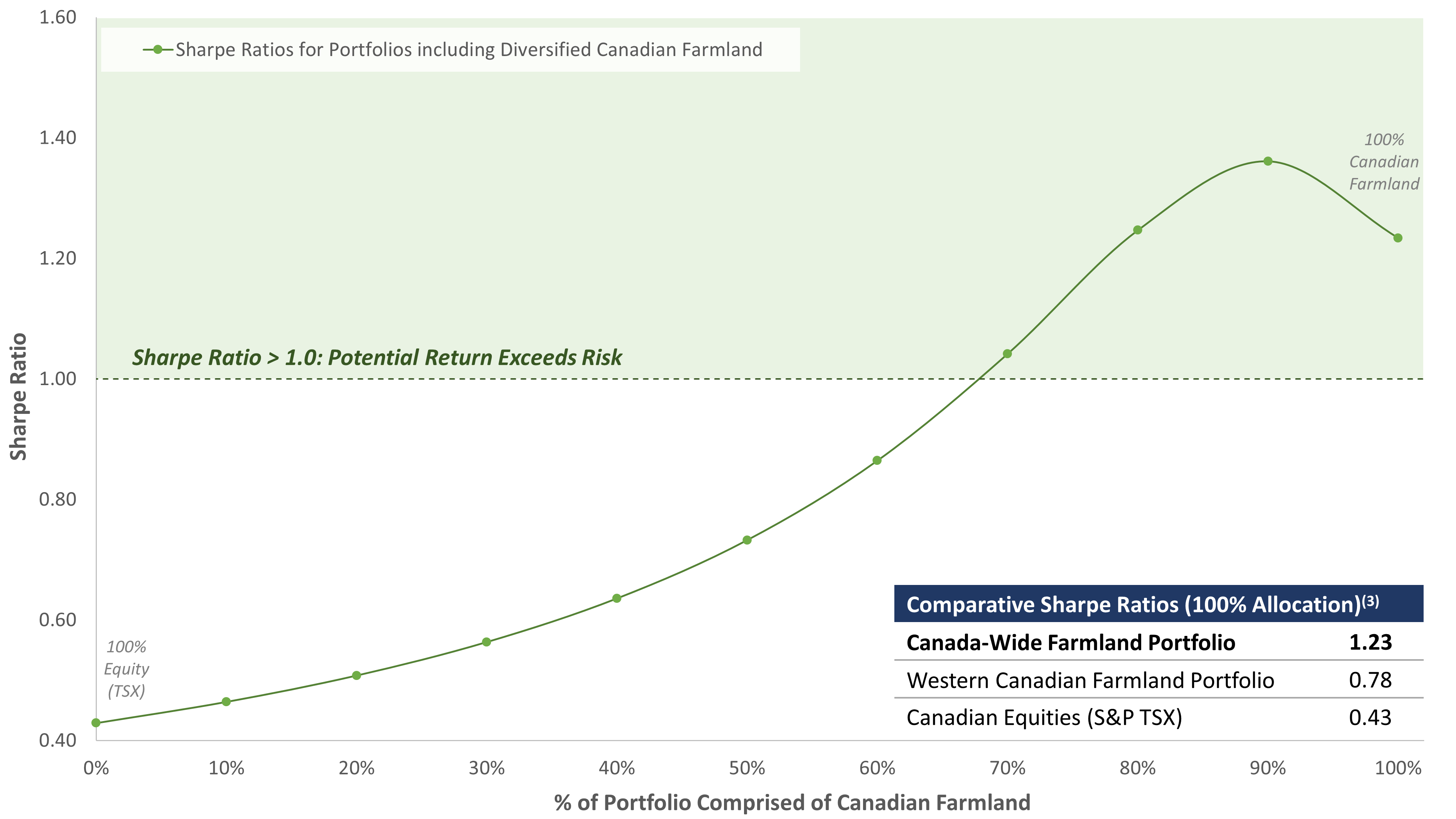

Assessing Risk & Return: Sharpe Ratio Analysis

To illustrate the value of diversification in an investment portfolio, we conducted a Sharpe ratio analysis(1) using historical Canadian farmland values between 1985-2019. This type of analysis is a staple of portfolio management theory and a relative measure of the trade-off between risk and return. A higher Sharpe ratio typically suggests a higher potential return per unit of risk taken on and therefore, many investors focus on improving / maximizing the Sharpe ratio of their portfolios.

Risk-Return Profile: Diversified Canadian Farmland in a Portfolio (Sharpe Ratio Analysis)(2)

The first takeaway from this analysis is the positive impact on the Sharpe Ratio as a result of increasing the allocation to Canadian farmland (regardless of its diversification) as opposed to holding only publicly traded equity. With its historically stable return profile, Canadian farmland reduces the volatility of returns and, therefore, improves the Sharpe ratio.

The second takeaway is the relative benefit of holding a portfolio with greater diversification amongst its farmland holdings. As seen in the chart above, portfolios consisting of farmland diversified across most provinces in Canada (Bonnefield currently invests in BC, AB, SK, MB, ON, NB, and NS) demonstrate higher Sharpe ratios, indicative of a favourable risk‐return trade-off, compared to those with farmland limited to only the prairie provinces. This illustrates the relative benefits of maximizing potential diversification within the farmland portfolio.

As noted in our Q1 2020 Newsletter, the Canadian agricultural community has been optimistic since the beginning of 2021 given:

The backdrop of increased feed demand from China;

The reduced crop supply from Brazil and Argentina; and

The Russian export tax on wheat.

Combined with a prolonged period of low interest rates, relatively low transactional activity for Canadian farmland in 2020, and the current multi-year high commodity prices for key crops, we continue to believe that Canadian farmland values are poised for an exciting period of strong growth.

As investors explore the benefits of Canadian farmland within their investment portfolios, we encourage them to consider the relative value of exposure to a well-diversified farmland portfolio to minimize volatility and maximize your potential risk-adjusted returns.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

(1) Sharpe ratios represent a relative measure potential returns compared to potential risk of an investment, and are calculated by dividing i) the excess return above a selected risk-free rate (i.e., average historical rate of return for an asset/investment less a risk-free rate such as the prevailing rate for a Government or Treasury-issued instrument) by ii) the standard deviation of those historical returns.

(2) Analysis contemplates hypothetical portfolios balanced between i) Canadian equities (S&P TSX index) and ii) Statistics Canada farmland values (weighted equally between selected provinces; Bonnefield’s investment provinces include BC, AB, SK, MB, ON, NS, and NB), between 1985 and 2019.

(3) Noted Sharpe ratios assume 100% allocation of a hypothetical portfolio to each of i) Canadian farmland in Bonnefield’s investment provinces, ii) Canadian farmland in AB/SK/MB only, and iii) Canadian equities (S&P TSX index).

Over the past decade, we have seen increased interest among the investment community in agriculture and farmland as an asset class. Not only are large, sophisticated, institutional investors across the globe evaluating (or already invest in) farmland and agricultural investments, so too, are increasing numbers of non-institutional investors.

Click here to read an article by Bonnefield’s Andrea Gruza that explores how farmland investments provide investors with a diversifying asset with strong ESG characteristics, climate change hedging capabilities and potential to support a move towards a net zero investment portfolio.

(Original article published in the spring 2021 edition of Radius European Investment Journal.)

Bonnefield’s Vice President of Capital Markets Andrea Gruza joined host Robert Arnason on the Between the Rows podcast recently to discuss ESG Investing and its relevance for Canada’s agricultural sector.

“ESG investing isn’t necessarily a widely agreed-upon term and the definitions and parameters around ESG in the investing community really are evolving. It stands for environmental, social and governance factors. The term certainly has become pretty widely recognized and adopted across multiple industries over the last few years, not just within finance, and you’re hearing [it] from the majority of large sophisticated investors across the globe.

“I think everybody’s situation is unique and I can’t speak [for] all farmers across the country, but I don’t think ESG is [just] a trend. I can imagine the terminology around ESG evolving and the set of considerations for each industry changing over time as it better reflects what’s happening in the world around us. I think that as we learn more, we’re more aware of what things we should be thinking about when we evaluate how a business is performing.

Listen to the podcast and full interview below, or by clicking here.

Note: This is the final article in an eight-part series published by GAI News that examines eight existing trends set to alter the structure of our global food system. Be sure to read the first seven articles here: Part I , Part II, Part III , Part IV , Part V , Part VI and Part VII.

“Economic growth won’t feed a growing population living on this finite planet.”– Phil Harding

Concerns about population growth have circulated through discourse since ancient times. Philosophers, such as Plato and Aristotle, questioned the sizes of their respective communities and their capacity to nourish additional people when the world had a population of about 162 million [i]. Writers from ancient Carthage had dwelled on population growth when global numbers had reached 200 million people, who were noted as “burdensome to the world which can hardly support us”. As we approach a global population that is fifty times larger than in Plato’s time, the same concerns come to light, albeit with different information.

Productivity improvements have typically remained one step ahead of food demand, allowing the world’s population to grow geometrically over the past two hundred years. Although the population continues to grow, crop yield productivity improvements have slowed considerably in the past several decades[ii].

While the preceding seven articles of our ‘Agriculture in a Changing Climate and Society’ series focus on secular trends affecting the supply side of the global agri-food system, this final piece delves into the demand side. A multitude of evidence points to a singular fact: nutritional demand is increasing rapidly on a global basis[iii]. Some experts question the world’s collective ability to nourish this demand in the long term[iv], while others speculate that new technologies will need to be developed and implemented in order to address the supply/demand imbalance. The World Resource Institute (WRI) indicates that while fulfilling nutrient requirements for an additional 2.4 billion people in the next thirty years is achievable, the global agri-food system will have to undergo significant changes in order to adapt[v].

As external factors, such as urbanization, water scarcity and pollinator loss, are set to reduce global food supply[vi], the earth’s population is projected to continue increasing for the next century[vii]. Sub-Saharan Africa is set to foster most of the world’s population growth, an area that is likely to become less suitable for crop production over the next century. In addition to increasing populations, a growing middle class will naturally continue to increase the global appetite for meat, dairy, and high-value fruit crops. These products are characterized by high production and overhead costs compared to other commodities of similar nutrient profiles. While this consumption shift is positive from the perspective of social mobility and will likely foster a period of robust demand growth for farmers in the short-medium term, the increased demand will come at cost to the environment.

Some estimate that we will have to increase arable land by 593 million hectares (more than twenty-four times the size of the United Kingdom) between 2010 and 2050 in order to bridge the gap needed to meet increasing food demands[viii]. The greatest concern lies in our collective food security in conjunction with global environmental sustainability. The socio-ecological trade-offs that arise from developing forested land lends itself to notions that our arable capacity is reaching its peak.

Food Spending and Disposable Income

Spending on food in the United States, as a percentage of disposable personal income, has been sitting near its historic low since 2004. This does not come as a surprise, but as a paradox, as calories consumed per capita in the U.S. reached the all-time high of 3,828 per day in 2005[ix].

Figure 1: Normalized food expenditures by final purchasers and users[x].

Source: USDA, 2019

Food cost compared to relative wealth is historically low throughout the world, largely due to commercialization of value-chains, historical productivity growth, and national subsidies. While consumers in developed countries are currently offered nourishment at relatively affordable prices compared to their historical income levels, these prices generally do not address the ecological externalities involved in producing the food[xi]. As such, a trend reversal is forecasted to begin in the next twenty years for net food expenditure, predicated on a declining basis of scarce resources, transitioning food demand patterns and a need to account for the environmental effects of food production.

The Malthusian Theory: Cropland Per Capita

Most significant, agricultural producers are losing cropland per capita[xii]. A typical Western diet requires about 1.2 acres of cropland per year to supply the types of calories to which we are accustomed. Emerging economies are now consuming similar diets to those of the West with more meat and dairy. This is creating a critical point of increased demand for energy intensive food products. Many areas of the world, namely Asia and Africa, will not have the arable land to produce nearly enough food to nourish its population. Figure 2 depicts each region’s cropland per capita.

Figure 2: Acres of Cropland Per Person, 2016

Source: History Database of the Global Environment (HYDE)

If every person had the appetite of an average individual in the United States at the current level of production, we would need to convert every acre of forest into farmland and would still be short of calories by about 38 percent[xiii]. With current Western food consumption, a diet that is becoming normalized by the world’s middle class, only a select few countries have the capacity to domestically produce more calories than they consume. The burden of production will be left to a handful of agricultural exporters with enough productive cropland to contribute to the global food stores, such as Canada and Australia. Admittedly, the Malthusian model of food supply versus cultivated land does not offer full explanatory power for the planet’s carrying capacity. It does, however, paint a general picture of the planet’s capacity to nourish different appetites at current technological levels.

Calories versus Nutrients

In assessing the issues surrounding global food demand, a distinction should be made between calories and nutrient-requirements. While about 800 million people globally are suffering from a means-based caloric deficit[xiv], over 2 billion do not have regular access to safe, nutritious, sufficient food[xv]. The developing world will continue to struggle with food accessibility as its population grows. Further, crop nutrient capacity in equatorial regions especially, is incredibly sensitive to rainfall variability and spells of extreme heat.

The developed-world’s farming system, which will likely provide the nourishment for most of the world’s growing population, is largely based on maximizing caloric production rather than nutrient density and diversity. This model has perpetuated throughout agricultural economies, as farmers are incentivized to maximize their yields in response to historic consumer and government interests in driving down food costs. Farmers act as rational participants, naturally responding to the markets they supply.

The developed world’s agricultural system is still incentivized with the same family of subsidies that were legislated at the dawn of the third agricultural revolution. In North America and Europe these subsidies typically offer support for a handful of crops with high caloric density such as feed-grains and oilseeds.

While global needs, production methods, and resource constraints continue to change, the policies surrounding the food system have remained largely unchanged since their inception. National subsidy programs are frequently reciprocated by similar or equivalent programs in neighbouring countries, leading to antiquated and sticky legislative movement across international value chains. Re-orienting farmer incentives from caloric density to nutrient diversity could be a fundamental step towards solving this issue by producing foods which meet the needs of a growing consumer base.

Solutions, Steps, and Goals

While the difficulties in feeding a growing population are considerable, there remains optimism that it can be achieved. There are 10 steps that would help us to address the challenges related to nourishing the food demands of a growing population. Each topic is complex, worthy of its own article, and many have been listed by the World Resource Institute as keys to “feeding the 10 billion”.

Food Waste Mitigation: Evidence indicates that the most effective mechanisms for supplying accessible and nutritious foods exists in reducing food waste rather than growing greater volumes of crops per acre. In the developing world, most food waste occurs at the production and storage levels, while in the developed world a staggering amount of food is lost at the consumption and market levels.

Investment in Aquaculture & Developing Sustainable Fisheries: Improved fish farming technologies including new genetics, infrastructure, and algae-based feeds have increased the competitiveness and investment merits of the aquaculture industry. Preservation of current fishery stock, alongside sustainable farming methods, will be the foundation from which we can offer omega-3 fatty acids in the future.

Climate-Controlled Agriculture: With so much emphasis placed in farmland per capita and the notion of declining scarce land assets, climate-controlled agriculture is consistently climbing towards profitability, and therefore viability, on a large, commercial scale. Investing in low-cost options such as warehouse conversion may prove to be the next frontier of effectively nourishing urban populations. With this being said, 95 percent of our food, even in the developed world, comes from farmland.

Improved Technology & Genetics: While crop-yield productivity growth has been slow compared to green revolution levels, new advances in crop genetics and molecular biology are remarkably promising. Further public and private investment in crop breeding, biologicals, and AI technology could make all the difference in feeding the next 2 billion people.

Enhanced Water Management: Water depletion in groundwater systems continues to be one of the most alarming aspects of modern agriculture. We will eventually have to shift to a process where crops are irrigated only through sustainable water sources, such as rain-fed reservoirs, rivers, and/or snowmelts. That shift should begin before aquifers are fully depleted.

Soil Health Preservation: Some scientists estimate that we are losing up to 1 percent of topsoil each year, with nutrient availability degrading as well. Nearly two-thirds of this degradation is derived from deforestation and overgrazing. Incorporating techniques such as no-till agriculture, rotational grazing, drill seeding, and certain organic production methods could significantly reduce the rate of soil loss.

Sequester Carbon in Soils: What benefits soil health may also create the opportunity to sequester additional carbon. Maximizing soil organic matter levels offers a multitude of effects, such as enhancing yields, sequestering more carbon, diminishing the required nutrients amendments, and enhancing ecosystem diversity. This can be achieved through the use of cover crops and healthier rotations, as well as no-till and conservational tillage methods.

Shift Diets Globally: While a sensitive argument in agricultural circles, the fact remains that reducing ruminant (beef and lamb) consumption would reduce the number of calories and land needed to produce that food-type by over ten times. If global diets slowly shifted towards plant-based proteins and nutrient-dense fruit/vegetable products, total stress on the environment would reduce. In addition, many farmers have the opportunity to improve pasture productivity with enhanced fertilizers and regenerative grazing techniques, which could increase the output of meat and reduce emissions.

Reforest Inefficient Lands: The second greatest contributor to carbon emissions is land deforestation, particularly in equatorial regions. Investing in direct efforts to bring these fallowed lands back to productive capacity or re-foresting the lands would promote carbon sequestration and a multitude of ecosystem services. Large food companies may also commit to plant trees and sourcing products from tropical deforestation-free value chains.

Re-orient Legislation: It may be time for consumers to take the burden of paying the ‘total price’ for food and water resources, which includes the cost of depletion and the externalities involved in using the resource. Further, subsidies and farm support should slowly start to shift towards food types that dovetail with the nutritional needs of our growing population.

Ultimately, addressing challenges pertaining to population growth and its nourishment will require active collaboration between businesses, policy makers, and consumers. Resources must be used more efficiently, and innovation will need to be spurred by public and private support. The above 10 points are topics that will exist throughout this century and likely beyond it. Many solutions to the nourishment issue are also investable opportunities, underpinned by global demographic trends. Those who have the opportunity to allocate capital also bear the responsibility to deploy their resources towards environmentally resilient strategies and regions. With investors in all asset classes assessing how they can limit their exposure to the effects of global warming, there are few industries more intertwined with climate change than agriculture. The effects of climate change are relevant to every aspect of the global food system. The long-term issues that affect the world’s agricultural output become opportunities to invest, thereby creating value for investors and society.