Note: this article first appeared in Global AgInvesting on September 4, 2019 globalaginvesting.com. This is the fifth article of an eight-part series published by GAI News that will examine how the global food system is set to be altered by eight existing trends. Each month a new installment will be released. Click the following links to read the first four installments: Part I , Part II, Part III and Part IV.

Written by: Jeremy Stroud, Bonnefield, Agricultural Investment Analyst, and Michael DeSa, AGD Consulting Founder

With the advent of sprawling wildfires throughout Brazil’s Amazon rainforest, politicians, businesses, and investors in timber and agriculture within the region are prompted to sincerely consider the ramifications of their asset management practices and investment decisions. While many forest fires occur as a natural and beneficial reaction of the local ecological cycle, this is not the case for the Amazon. Despite the fact that these fires have taken place in Brazil’s dry season, INPE, the Brazilian national space agency, has documented an 83 percent increase in fires since the previous year,[1] while deforestation has increased by 67 percent since January 2019.[2] The El Niño dry period likely contributed to the severity, although INPE has directly connected these fires with the recent onslaught of deforestation and greenfield agricultural development.[3]

The Amazon basin supports over half the world’s tropical rainforests and currently acts to offset approximately one quarter of human-caused greenhouse gas emissions.[4] Events taking place in Brazil serve as a vivid reminder of weather volatility and its intersection with global agriculture. This issue explores severe weather events, natural disaster risk in farming regions and the implications for investors. The findings reaffirm similar themes in past installments: those who have the opportunity to invest in land and water resources also bear the responsibility to allocate their capital towards environmentally resilient regions and strategies.

While we previously wrote about global warming, carbon emissions, and the long-term growth of global surface temperatures, this article reflects the opposite side of the climate change coin. It pertains to the immediate consequences of severe weather events and natural disasters. As temperatures increase, additional moisture is retained in the air which leads to heavier downpours and a higher frequency of extreme precipitation events.[5] On the other hand, warmer weather also accelerates the pace of evaporation, leading to circumstances where droughts and wildfires may prevail. Agriculture has always succumbed to the forces of unsettled weather behavior, although trends project increased volatility in each of the next several decades. Extreme events are accelerating at a tremendous pace, and Figure 1 exhibits just how fast it is happening.

Figure 1: Occurrence of Global Natural Disasters[6]

Source: International Disasters Database (EM-DAT), GMO Investments, 2018

According to the UN’s Food and Agriculture Organization (FAO), over 20 percent of economic losses due to natural disasters are absorbed by agricultural businesses worldwide with natural disasters accounting for approximately one quarter of annual crop losses.[7] Beyond losses to farm yields, severe storms and droughts also constrain logistical systems that service the agri-food industry. River traffic throughout the Mississippi River, for example, was reduced significantly after a drought in 2012 narrowed the route. We also witnessed substantial flooding this spring in the U.S. Midwest where farmers experienced delayed planting, destroyed facilities, and increased spoilage for crops in storage.

Although natural disasters are indiscriminate in their movements, each geography faces a different level of risk. Figure 2 depicts each country’s susceptibility to natural disaster risk from the 2018 World Risk Report by the United Nations Institute for Environment and Human Security. It offers insight on a country’s exposure and vulnerability to potential natural disasters by analyzing historical data. The study ranks 173 countries by measuring an average citizen’s probability of being exposed to natural hazards such as floods, storms, droughts, sea level events, and earthquakes.

Figure 2: World Risk Report – Risk of an Extreme Natural Event Leading to Disaster[8]

Source: United Nations – Institute for Environment and Human Security (UN-EHS), 2018

The multi-year United Nations analysis identifies Central America, West and Central Africa, Southeast Asia, and Oceania as the areas with the highest global disaster risk. It indicates that while many countries are improving their disaster preparedness, extremes in weather systems are expected to occur more frequently with heightened potential for negative consequences.[9] Although the concern is growing throughout the world, Canada and Europe’s diversified geography and cooler climate position them as some of the lowest risk regions in the world. Countries with robust national emergency management systems have also helped to partially mitigate the devastating effects of severe weather and geological systems.

The Modern Investor’s Response to Catastrophe

The Cambridge Centre for Risk Studies uses a series of scenario analyses to assess the impact of hypothetically likely natural disasters on financial markets and investment portfolios.[10] The study forecasts significant economic consequences for equity markets if any of these events were to occur. For example if Mount Rainier, an active volcano in the state of Washington, were to erupt, the S&P 500 and Dow Jones Industrial Average are expected to suffer a 20 percent loss.[11] Other scenarios that were studied include floods, hurricanes, and earthquakes, and although each have a low probability of occurrence, they collectively exemplify the potential for a large destructive event.

There are few winners in the wake of catastrophe, as production capacity, investor confidence, and local infrastructure all suffer. As such, traditional portfolios consisting of public equity and fixed income assets are particularly vulnerable to natural disaster events due to their global interconnectedness. In the event of an extreme disaster with over US$1 trillion in damages, returns are expected to suffer in a non-linear manner with their risk-tolerance as global markets are perturbed. Investing in a diversified portfolio of real assets such as infrastructure and farmland in low-risk geographies may act to offset economic losses brought forth by severe environmental events and fluctuations.

Investors may also consider allocating capital towards regenerative agricultural practices and land portfolios with disaster prevention infrastructure in place. Regenerative agriculture, which works to increase soil organic matter content, will increase the resilience of soil structures, thereby increasing moisture retention during times of drought and reducing topsoil erosion in heavy downpours.

Recent events have provided all agricultural investors, no matter their exposure to specific geographies, commodities, or strategies, with the opportunity to consider the long-term ecological consequences of their actions. Preservation of capital with positive environmental and economic returns may be achieved with careful due diligence and investment discipline. Critically acclaimed investor, Jeremy Grantham, may have best articulated the matter in his most recent report:

“We’re racing to protect not just our portfolios, not just our grandchildren, but our species. So get to it.”

Note: this article first appeared in Global AgInvesting on July 24, 2019 globalaginvesting.com. This is the fourth article of an eight-part series published by GAI News that will examine how the global food system is set to be altered by eight existing trends. Each month a new installment will be released. Click the following links to read the first two installments: Part I , Part II and Part III.

Written by: Jeremy Stroud, Bonnefield, Agricultural Investment Analyst

“The global average temperature for June 2019 was declared the hottest ever recorded for the month.” [1]

Headlines such as these occur with such regularity that we tend to become desensitized to the magnitude of the statement. News of record-high temperatures, melting glaciers and unprecedented carbon dioxide (CO2) levels have become so commonplace that they are now a focal point of political discourse and investment decision-making. Investors in all asset classes are assessing how they can limit their exposure to the effects of global warming, and there are few industries more intertwined with climate change than agriculture. Capital deployed in the agri-food industry, and more specifically in farmland, is set to face structural challenges in the long-term. Structural challenges such as these naturally lead to opportunities for investors with the foresight and patience to execute on long-term investment theses. This article explores how rising temperatures and CO2 levels are projected to affect global land suitability over the course of this century, and present the select few regions which may benefit from these new climatic conditions.

Carbon Dioxide and Heightened Temperatures

Temperatures are set to accelerate at a pace greater than we have seen since the glacial retreat of the last ice age as atmospheric CO2 has reached its highest level in the past three million years[2]. Warming occurs when certain greenhouse gases, such as CO2, restrict heat from escaping the atmosphere[3]. In the short term, higher CO2 levels may benefit crops such as soybeans and wheat due to increased photosynthesis capacity and water retention; however, the greater picture appears quite different[4]. Figure 1 portrays the earth’s average CO2 levels over the past 800,000 years.

Figure 1: Historical CO2 Levels in Parts Per Million

While global surface temperatures have already increased by about 1ºC since 1950, global temperature is projected to increase by another 2.5ºC in the next 40 years[5] and up to 4.5ºC by the end of the century, at the current pace of emissions[6]. This is poised to cause depletion of water resources, rising sea levels and severe pressure on our collective environmental system. Figure 2 demonstrates the historic global surface temperature compared to the 1951-1980 average since 1900.

Figure 2: Global Surface Temperature Compared to 1951-1980 Average

Source: NASA Goddard Institute for Space Studies, GMO Investments, 2016

Dropping Yields and Changing Fields

As each plant variety has a designated temperature range within which it can grow and reproduce, additional heat stress caused by global warming will stunt various crops’ ability to pollinate, retain moisture, and develop roots. Increasing temperatures, therefore, are expected to decrease the land area conducive to the production of high-calorie crops such as wheat, soy, and corn. A National Academy of Sciences study estimates a 5 to 15 percent decrease in grain crop production for each degree Celsius over current levels[7]. With temperatures currently rising, a rebalance of the agrarian equilibrium and a loss of biodiversity in oceans and forests is already taking place.

Overall crop yields are expected to begin their decline by 2030, and certain northern regions will be relied on to meet global nutritional needs[8]. Diseases, weeds, and insects, which thrive in warmer conditions, are expected to multiply and further restrain yield growth, while food nutrition is set to drop. Total yield decline is attributed in part to water scarcity and greater rainfall variability, the proliferation of pests, extreme heat events, and the reduction of multi-cropping in equatorial regions[9]. The International Food Policy Research Institute also recently published a study which found that plant nutrient availability is forecasted to significantly decline as a result of growing atmospheric CO2 levels[10]. Protein, iron, and zinc could each decline by between 15 and 20 percent in global availability over the next 30 years according to their model. In short, the world’s growing demographic will require more food to supply consumers with the same nutritional profile that we currently enjoy. Our collective ability to achieve this depends on an increase in crop yield per unit of farmland, in addition to an increase in global farmable land base.

Figure 3 depicts the forecasted change in farmland suitability to grow the 16 most common crops from averages in 1981–2010 to 2071–2100. Green areas exhibit an increase in suitability, while yellow and brown colored regions reveal where a decrease in land suitability occurs.

Figure 3: Change in agricultural suitability between 1981–2010 and 2071–2100.

Source: Zabel, Putzenlechner & Mauser, 2014

The researchers who produced this map use an internationally recognized climate scenario model to determine the climatic and topographic changes that are expected by the late 21st century[11]. The findings from this study are clearly stated: higher latitude areas such as Canada, Norway, China, Russia, Mongolia, and parts of the United States are expected to grow in suitable land area by 2100. On the other hand, many warm-climate regions, which are accelerating in population growth and therefore nutritional needs, will face reduced land suitability.

Investing Where It’s Cool: The High Latitude Thesis

A longer growing season and additional heat units for crops such as wheat and corn will increase the area in northern regions that are conducive to temperate cereal cultivation. Figure 4 shows the boreal forest in green, along with the estimated movement of agricultural suitability boundaries in the northern hemisphere.

Figure 4: Northward shift of the agricultural climate zone under 21st-century global climate change King et al., 2018

By 2099, about 76 percent of the area shown in green above is expected to reach crop feasible growing conditions compared to the current 32 percent[12]. For long-term investors with investment horizons of over 20 years, boreal regions such as the Clay Belt in Ontario and the Northern Prairies of Alberta are forecasted to become viable for large-scale grain and pulse production as temperatures increase. In these regions, the sparse populations and significant levels of capital needed to prepare the land for production have kept asset prices reasonably low. With the correct local knowledge and capital flows, tens of million acres in Canada and Russia that were previously untouched could emerge as the final frontier of scalable farmland use.

The high latitude investment thesis is not only underpinned by an increase in suitable land, but also an expected increase in crop yields. Figure 5 demonstrates the projected change in yields by sub-region between 2010 and 2050 considering a 3ºC increase in temperature from pre-industrial levels.

Figure 5: Projected Impacts on Crop Yields in a 3°C Warmer World

Source: World Resource Institute, The World Bank, 2010

The high-latitude investment thesis calls to immediate question the fact that many forested areas, which act as carbon sinks, would need to be converted to scalable crop production. It is then crucial for investors and policymakers to consider alternatives for preserving global ecosystem services, perhaps by investing in carbon offset programs or tree re-planting projects. With the knowledge and technology now available, investors are also urged to promote and implement production techniques that preserve and enhance affected ecosystem services. Evidence indicates that investment in regenerative agricultural practices, sustainable intensification, and maintaining soils with high levels of organic matter may mitigate some externalities of a warming planet[13]. Investment in foundational infrastructure strategies such as community development, transportation, green energy, and processing facilities could create opportunities for investors to diversify cash flows while integrating synergies with their farmland investments. A portfolio such as this would be a sustainable step forward to providing the world with the food it needs.

Note: this article first appeared in Global AgInvesting on June 10, 2019 globalaginvesting.com. This is the third article of an eight-part series published by GAI News that will examine how the global food system is set to be altered by eight existing trends. Each month a new installment will be released. Click the following links to read the first two installments: Part I and Part II

Primary authors: Jeremy Stroud, Bonnefield, Agricultural Investment Analyst, and Michael DeSa of AGD Consulting

“In all affairs it’s a healthy thing now and then to hang a question mark on the things you have long taken for granted.” – Bertrand Russell

There is every reason for us as consumers to pause and consider something that is far too often taken for granted – water. It has become a truism to say that civilization would not exist without the reliability of our earth’s accessible water resources. Our species’ ability to evolve past a Paleolithic state is a direct result of our advances in freshwater use, from leveraging gravity for flood irrigation to controlling water flow with aqueducts to the implementation of digitally integrated irrigation systems.

Societal reliance on fresh water has been presupposed for so many centuries that many of us overlook the ongoing constraints set to fundamentally alter the way we use this scarce resource. This article aims to review a few of the many water challenges affecting the global agri-food sector and places a spotlight on investable regions which may weather the storm most effectively.

When assessing freshwater availability, it is essential to consider the components of the water system within and beyond human control. The thought of addressing all water challenges may be an overwhelmingly broad topic, so the conversation becomes more actionable when we focus on components that can be changed rather than those that cannot. Of freshwater stores, ‘blue water’ is the most pertinent topic to international agriculture as we have little control over deviation in rainwater occurrence and quantity. Water scientists place particular emphasis on blue water within the context of a changing climate – namely as it pertains to projected increases in the frequency and severity of global drought [1].

Common Freshwater Classification [2]

Less than three percent of the earth’s total water stock is fresh water and nearly four-fifths of the three percent are permanently frozen and inaccessible[3]. After factoring in areas of excessive pollution, acidity and salinization we are left with less than one-tenth of a percent of fresh water supply available for human, agriculture and industry use[4]. In other words, this equates to about 10,000,000 cubic km of fresh, accessible ground and surface water[5]. While freshwater is limited in volume, humans are continuing to increase consumption per capita on an annual basis,[6] and at a pace that far exceeds the rate of replenishment.[7] Here lies the bone of contention. It is not a question of whether we are using scarce water resources at an unsustainable pace, but rather a discussion of what can be done about it.

Blue Water – Consumable and Irrigatable

Water use for irrigation is among the most heavily contested aspects of the modern agricultural system. Agriculture and blue water depletion are inextricably linked. According to a recent report from IPBES, nearly 75 percent of the world’s accessible freshwater consumption is dedicated to crop and livestock production and nearly 40 percent of the planet’s current food supply is reliant on irrigation [8]. This issue becomes further pronounced when we consider that nearly half of the world’s population is living within immediate proximity to river basins and aquifers with the ‘severe water stress’ classification [9]. Evidence suggests that over-usage and maltreatment of accessible freshwater resources could cause a contraction in global productivity growth and therefore a potential decline in living standards [10].

Most of our planet’s accessible fresh water is confined in shallow aquifers beneath the earth’s surface. A high proportion of these non-renewable aquifers are reaching critical points of depletion, and they are commonly located in areas which fall beneath the world’s most populous and important agricultural regions. A study from the Proceedings of the National Academy of Science estimates that up to 100 million irrigated acres may be unable to draw sufficient water resources to support production by the end of the century[11]. This could lead to drastic decreases in crop yields if rainfall averages cannot make up the difference. The Ogallala aquifer beneath the US corn belt, for example, is particularly threatened by overuse and pollutant contamination. A reversal of irrigated land to dryland is expected to occur in regions such as California’s central valleys, the US Mid-West, the North-China Plain, and the Arabian Basin. In each of these regions non-renewable groundwater is a primary source of irrigation. It is not coincidental that each of these regions have been subject to significant water stress in the past decade.

Blue water depletion is a complex issue that demands collective action – not solvable by implementing any single policy, action or framework, but rather it requires a cooperation between all levels of business, government and society. Irrigated farms which source their water from continually measured, renewable deposits (such as sustainably disbursed lakes and river systems) may be the most productive, economical and sustainable solution to the forthcoming water scarcity challenges.

Virtual Water

Consumers may look at food-induced water depletion as a direct product of farm activity, while the reality more complex and integrates all facets of society. Farmers, like any other business, are economic entities that aim to optimize output, scale and profitability. In the agri-food sector this is accomplished by efficiently fulfilling the needs of consumers. With a growing population and an increasing appetite for high-quality proteins, fruits and vegetables, consumers tend not to realize the macro-effects of their individual purchasing decisions but rather focus on the needs of the household or community.

As it stands, we have a developed consumer base that is unaware that we effectively outsource water depletion through our demand for high water-footprint foods[12]. An often cited example is China’s import of water-intensive soybeans from areas such as Brazil which has led to indirect pressure on deforestation of the Amazon[13]. We have historically been able to purchase food and industrial products with the cost of water extraction embedded in the price, but often not the true cost of water depletion. This distinction is vital to the topic of global water management, where governments often subsidize industry water use as a regular cost of doing business in order to provide consumers with food options that meet their demands.

Most experts believe these consumer trends towards high-footprint foods are firmly established, although as shoppers begin to realize the increased demands on water a result of their decisions, they too may begin to search for more sustainable and renewable ways to use the available water supply. It is here where we see a long-term investable opportunity.

Farmland Investing: Go Where the Renewable Water Flows

The pursuit of a sustainable and profitable agricultural investment portfolio may be achieved through consideration of macro-climatic indicators, strategic selection and rigorous due diligence. While this article refers to agricultural investing from a farmland perspective, there is also a case to be made for investments in agricultural technology, including efficient irrigation, wastewater reuse, soil moisture sensing and seed resilience technologies.

A structural decline in crop production is expected to create supply shocks in the future, potentially raising agricultural commodity prices in the long term. The Intergovernmental Panel on Climate Change (IPCC) estimates that crop yields could decline by up to 12 percent as a consequence of water scarcity in the next three decades [14]. The thesis of investing in ‘water-rich’ regions is predicated upon their capacity to weather an incoming storm of potential water issues:

~ Invest where irrigation is less necessary for productive agriculture: Less than four percent of Canada, Brazil, Russia and Australia’s farmland is irrigated compared to about ten percent in the United States and 37 percent in India [15] (See Figure 2). Productive agricultural regions that are less dependent on irrigation tend to hedge the risk of groundwater depletion and/or pollution.

Figure 2: Percentage of Farmland Under Irrigation [16]

Source: The World Bank World Development Indicators, 2015

~ Analyze metrics to determine where water shortages are expected to fall: Statistics such as renewable fresh water per capita are helpful in determining where water crises are expected to occur. Other helpful statistics include aquifer replenishment rates, variable on-farm water requirements, and the legal parameters of water resource allocation. While Canada, Russia, Australia, and Brazil use relatively little water for irrigation compared to the rest of the world, they hold the most fresh water reserves per capita of all agricultural exporters with 80,200 cubic meters [17]. Further projections suggest that warm-climate regions are likely to experience decreasing precipitation levels in the next century while polar and continental regions may encounter more rainfall [18]. Although each country’s water rights laws and natural precipitation levels may vary, the thesis holds over a long-term geographic perspective while political frameworks may change. This sentiment should be further examined at a regional level to assess where irrigating farmland may be achieved most sustainably.

Figure 3: Global Freshwater Resources per Capita [19]

Source: The World Bank, 2014

For as long as humans inhabit the planet, unpolluted, fresh, water will be a finite resource with limited supply and consistent demand. Although specific water reserves appear to have promise over the next several decades, it is a responsibility for farm owners, governments, consumers, and investors to responsibly regulate withdrawal and avert contamination. Freshwater depletion is an agricultural issue just as much as it is an environmental one. Here lies a rare circumstance where economic returns may be matched by environmental impact. Agricultural investors have a distinct opportunity to allocate capital towards efficient irrigation and farmland portfolios in regions that have the replenishing capacity to withdraw water resources sustainably.

Note: this article first appeared in Global AgInvesting on April 23, 2019 globalaginvesting.com. This is the second article of a series published by GAI News. The first installment can be found here. The eight-part series will examine how the global food system is set to be altered by eight existing trends.

Primary author: Jeremy Stroud, Bonnefield, Agricultural Investment Analyst

Contributing author: Michael DeSa, AGD Consulting

“The nation that destroys its soil destroys itself.” – F.D. Roosevelt

The oft-imagined idea of fertile, pristine farmland as far as the eye can see is drifting towards the past. Land loss is more than just a blow to those who grasp on to a pastoral ideal of the countryside; rather it marks a shift in the global supply dynamics of land resources. The literature presents a singular case: more topsoil is removed from production than is added, with some academics estimating a reduction of about 1 percent each year[1].

Healthy topsoil is home to billions of thriving micro-organisms which allow crops to be optimally produced. As the top soil is physically eroded or disrupted, its biological matter also declines, and therefore its capacity to produce optimal yields is compromised.

Land scarcity is not a new concept, although with the level of impact it is expected to have on society, it is a topic that deserves more discussion. In the first article of this series, we discussed the effects of urbanization on the global agricultural system. This commentary will examine another piece of the farmland usage puzzle and its impact on our collective accessibility to food: land degradation and soil erosion.

Land degradation refers to human-derived processes which lead to the decline in ecosystem functions[2]. It manifests itself in three different forms:

physical: compaction, desertification, and soil erosion (which is the largest contributor to productivity loss)

chemical: soil acidification and salinization

biological: soil organic matter reduction and loss in biodiversity

Farmers work in different ways to combat chemical and biological forms of land degradation, although the most persistent and arguably the most difficult to mitigate of these, is physical degradation of topsoil. While usually considered as a local concern, soil erosion, compaction and other types of land degradation are globally consequential issues and evidence suggests they will have direct implications for the world’s food supply.

The Inter-Governmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) is widely considered the international authority on bio-ecological matters[3]. The organization recently concluded a three-year study analyzing the status of global land and soil quality, which collected insights from over one hundred of the world’s leading subject experts. They found that approximately 3.2 billion people, or nearly 43 percent of the world’s population, experience negative economic impacts from land degradation in industries varying from agriculture to tourism, to mining[4]. The effects of land degradation are expected to accelerate in magnitude as the degree of high-volatility weather systems increase[5].

The Causes and Status of Land Degradation Globally

Erosion takes place when soil is left uncovered and the particles are washed or blown away. Heavy downpours, surface water ponding, intensive land use and mechanical human activities are continuing to reduce top soil – particularly in the most intensively farmed regions. For example, China and India are losing topsoil at three to four times the rate of North America[6]. Land erosion and degradation also occurs due to tillage, deforestation, and an increase in rainfall intensity. One study indicates that there has been a 53 percent increase in the number of extreme rainfall days recorded globally over the past 30 years, thereby leading to record levels of erosion and runoff[7].

In the past 20 years, a greater proportion of rainfall has arrived in the form of extreme single-day weather events than has ever been recorded. Figure 1 demonstrates the percentage of land area in the contiguous United States affected by extreme precipitation in each year as reported by the National Oceanic and Atmospheric Administration. The orange line represents a nine-year trailing average, highlighting a significant fact for soil erosion: the average percentage of US land affected by extreme one-day rain events has increased from 7 percent in the 1970’s to 18 percent in 2015.

Figure 1: Extreme One-Day Weather Events in the Contiguous United States, 1910-2015[8]

Erosion naturally leads to further soil compaction, nutrient degradation and impaired water drainage, which reduces the overall productive capacity of the land. With nearly 60 percent of the world’s farmland considered degraded, our arable land base is steadily declining[9].

Figure 2 demonstrates where the greatest soil erosion concerns are expected to occur in the future based on a detailed joint study by the European Commission and the University of Basel. The R-factor is the rainfall-runoff erosivity factor, or an annual summation of erosion index (EI) values (erosion force of rainfall) in a normal year’s rain.

Figure 2: The Geo-Spatial Pattern of Soil Erosion, 2018[10]

Opportunity Amidst the Loss

As soil degradation increases the scarcity of fertile land, it also creates the need to incorporate sustainable farm management practices and pursue responsible investment goals. Farmland investors and stakeholders should consider five primary categories in their path to mitigate soil erosion effects and potentially reap the upside potential that follows:

1.) Deal Sourcing & Region Identification: Investors should look to identify farming regions with topsoil abundance, low wind and flood risk, and relatively flat or rolling terrain. Investment teams have the responsibility to review an area’s historical and forecasted climatic risks in advance of deal selection. This includes past precipitation and temperature averages, available soil and yield mapping data, historical input usage, previous environmental issues and/or remediation measures. Investors may also want to consider geographic regions that successfully practice no-till land preparation, such as Argentina, Australia, and Canada.

2.) Due Diligence: Most farmland asset managers should be able to leverage geo-spatial information data and measurement tools to determine how past farm imagery compares to the current status of the field. It is also worthwhile to consider warning signs such as noticeable compaction, dispersed ponding, and natural drainage flows.

3.) Sustainable Farm Management Practices: Farm operators have the opportunity to replenish topsoil quality through the implementation of practices such as no-till and low-till farming, as well as the regular use of green manure crops to enhance soil biodiversity, structure, and to replenish nutrients. Further, integrated pest management (IPM) plans leveraging biological and mechanical processes can control pests while reducing chemical pesticide use.

4.) Investment in Loss Prevention & Restoration: Capital expenditure in ditching, tile drainage, external tree-borders, berms, and riparian-buffer maintenance can control soil erosion effects while also mitigating natural disaster risks such as flooding, wind damage, and surface ponding. For permanent and specialty crop strategies, the implementation of technology and products offered by groups like the Land Life Company – a startup that is working to restore ecosystems in degraded soil regions through reforestation efforts – should be considered CapEx well spent.[14]

5.) Long-term Tenure Mindset: Investors who plan to own and/or operate farmland for the long-term will be naturally incentivized to adopt sustainable land management practices which can promote the health and productivity of soil. Farmland owners should be cautious of short-term (less than three year) lease structures which may create the risks of nutrient mining or high-intensity agricultural practices.

With land degradation on the rise, the tools to reduce soil loss and protect these investments are slowly becoming more available and adoptable. As soils from intensive agricultural regions continue to deplete, we hypothesize that land managed with sustainable practices shall prove to be significantly more valuable in the decades to come.

Note: this article first appeared in Global AgInvesting on March 21, 2019 globalaginvesting.com. This is the first article of a series published by GAI News. The eight-part series will examine how the global food system is set to be altered by eight existing trends.

Primary author: Jeremy Stroud, Bonnefield, Agricultural Investment Analyst

Contributing authors: Michael DeSa, AGD Consulting and Solomon Tiruneh, AGD Consulting

It is no secret that our global food system is in a state of flux. In the next century, we will be challenged to produce more food with less land, by fewer farmers, and with increasingly scarce water resources. Although evidence suggests that we as humans have the capacity to achieve this, it is imperative to explore what changes can be expected from the planet’s climatic and demographic variability. The purpose of this article series is to provide insight on these changes and place a spotlight on the regions which may weather the change most effectively. While other parts of the world are projected to experience comparatively strenuous conditions, parts of the Canadian and U.S. agricultural systems are positioned to endure and even prosper in the face of a changing climate and demographic.

A combination of industry and academic literature indicates eight existing trends that are set to alter the structure of our global food system. A growing body of data indicates that these factors may determine our collective success or failure:

1. Urban expansion

2. Land erosion and degradation

3. Fresh water scarcity and agriculture’s reliance on irrigation

4. Increasing temperatures and CO2 levels

5. Volatility of weather systems

6. Global phosphate over-use

7. Bee fatalities and pollination

8. Population growth in proportion to arable land

As with any changing market, structural movements can lead to inefficiencies which are then corrected by the activities of market participants. In this case the global agri-food sector could face extensive resource constraints and shifts in pools of capital over the next half century. This may establish the environment for public and private entities to create efficiencies by allocating capital to new infrastructure projects, accessible financing alternatives, synergistic consolidation, progressive policies, and industry-led innovation.

Let’s start with a topic that is close to many of our homes – urban expansion:

Urban Expansion

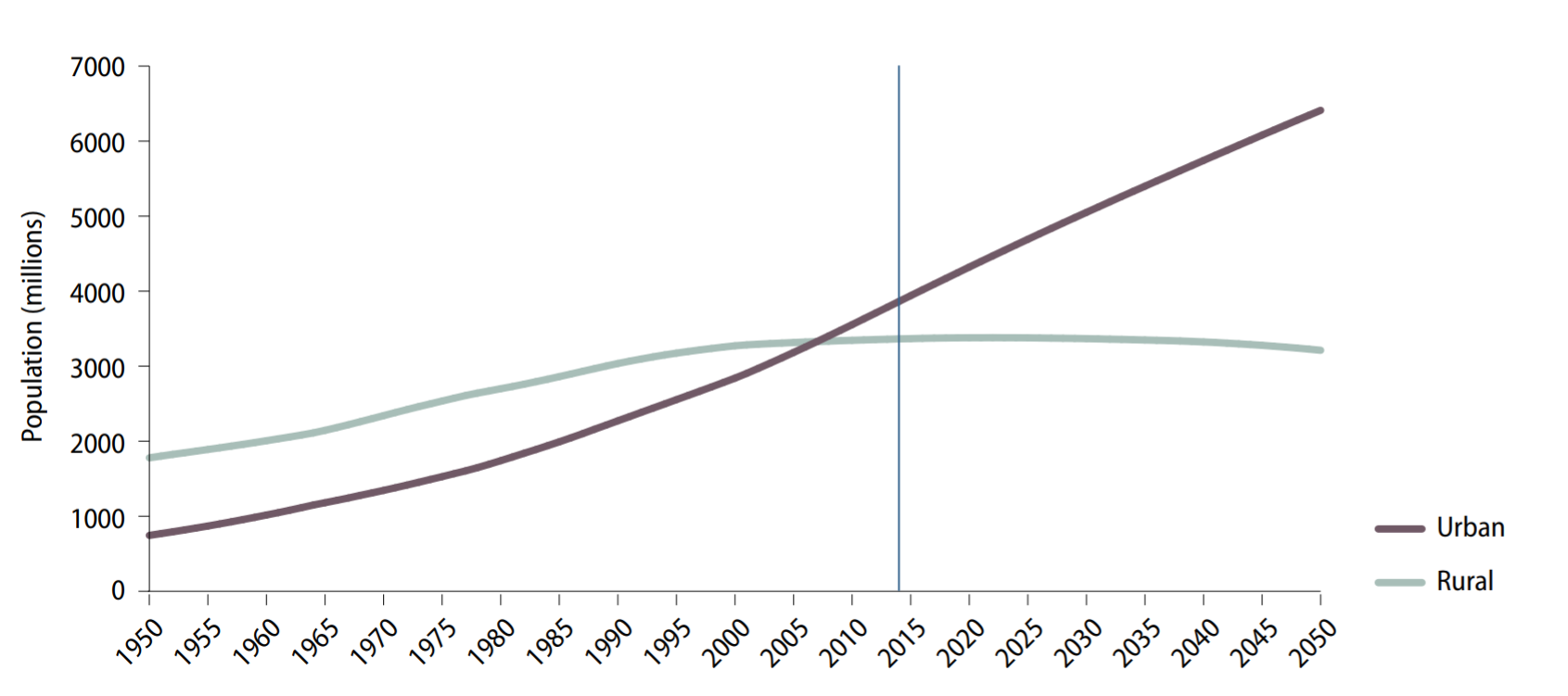

It is a modern reality that some of the world’s most fertile soil is now beneath several layers of concrete. Cities were originally established based on their proximity to agriculturally productive land and its strategic significance. As economies continue to shift from rural to urban residency, the world’s major cities naturally expand outwards. Unless geographic or regulatory restrictions exist, cities extend by developing into farmland areas that had historically been the source of their nourishment. Currently, populations in developing economies are urbanizing at a rapid pace with 40 percent of urbanization taking place in developing slums – a trend that is expected to heighten regional socio-economic disparities and sanitary-access concerns. The global urban population is set to increase by 2.5 billion people by 2050, with India, China, and Nigeria accounting for nearly 900 million additional people. Figure 1 highlights the global shift in urban vs. rural populations.

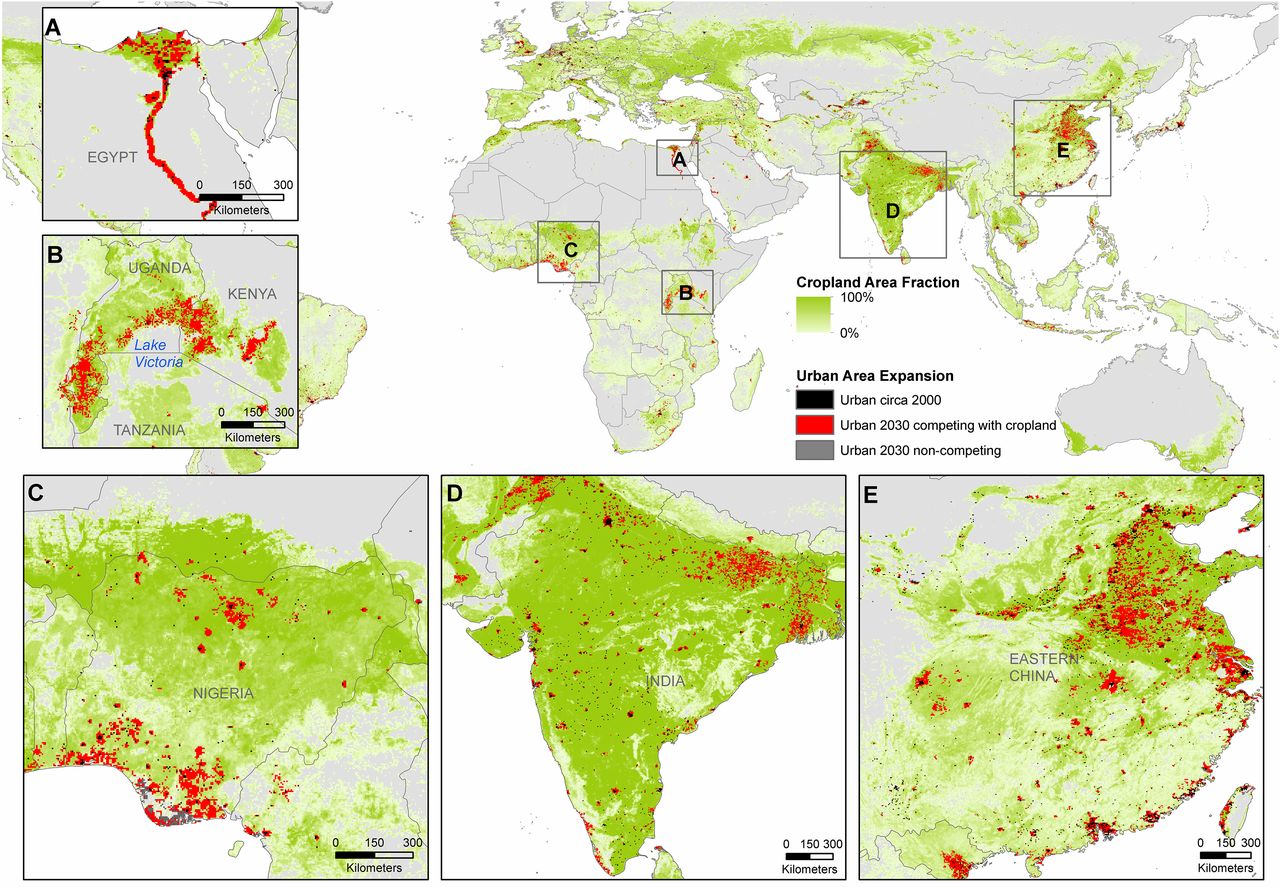

Urban expansion is projected to reduce our global cropland area by 47 million acres between 2015 – 2030, and it is taking place on cropland that is 77 percent more productive than average. This is an especially concerning issue in the developing world where population growth will expand at the highest rate throughout ‘mega-urban’ areas. Nearly 90 percent of the world’s cropland loss due to urban expansion will take place in Asia and Africa. Figure 2 exhibits the fertile areas which will be hit hardest by urban expansion.

Crop growing regions are affected by urbanization to a far lesser extent in countries with dispersed population centers, an abundance of land resources, and proactive land-use regulations, such as in Canada, the U.S., and Australia. In Canada, for example, the Golden Horseshoe Greenbelt and Agricultural Land Reserve Acts collectively protect more than 13 million acres of productive farmland. Although it may make immediate economic sense for cities to develop outwards instead of upwards, natural geographic barriers to urban expansion have contributed to some of the most prosperous and concentrated cities on the planet, such as New York and Singapore. Increased urban density (whether a consequence of necessity or planning) has also been correlated to increased productivity and wages due to the cost savings derived from urban agglomeration.

Urban Expansion and Agricultural Investing

With the emergence of concerns relating to urban expansion and its effects on agriculture, our minds naturally lean towards the merits of indoor farming as a solution to farmland loss. While urban and greenhouse farming projects have developed rapidly due to recent technological advancements and access to venture capital funding, the types of foods grown in enclosed settings are typically exclusive of the grains, oilseeds, pulses, field vegetables, and permanent crops grown on farms. The future of our food system will likely consist of a complementary combination of climate-controlled indoor and traditional outdoor farming methods rather than a slant towards just one. Investments on both sides of the agricultural production spectrum are expected to generate similar risk-adjusted returns over the long term, albeit with differing levels of volatility, asset capital appreciation, cash flows, operational risks, and sensitivity to commodity price fluctuations.

Within the context of global urbanization, farmland located on the perimeter of a growing city will typically command price premiums for development potential. This land is no longer valued for its productive agricultural capacity and would be considered a different investment class altogether. Some of the safest and most fundamentally-sound agricultural investments available are located in close enough proximity to supply growing cities with fresh food, yet far enough away not to have development premiums. These assets naturally lend themselves to the pursuit of sustainable development goals through farmland protection and their function in nourishing a demand-oriented market. Further, they retain logistical and shelf-life efficiency, particularly for direct-to-eat goods. An investment of this type also may be optimized and expanded in the long term to increase economies of scale and capacity for production of different crop types.

As productive crop growing land becomes increasingly scarce over the next century, the significance of fertile land assets have every reason to flourish.

D’Amour et al. (2016). Proceedings of the National Academy of Sciences. Future urban land expansion and implications for global croplands. https://www.pnas.org/content/114/34/8939