Farmland continues to gain recognition as a stable and diversifying asset class that has historically provided inflation protection, low correlation to public markets, and long-term value preservation. Within it, investors often compare two distinct categories: row crops such as grains, oilseeds, and pulses, and permanent crops such as fruit orchards and berry fields. Each has unique characteristics and, at Bonnefield, we believe the right balance of both offers investors attractive risk-adjusted returns.

Download our Q2 2026 newsletter for an overview of the different characteristics and considerations that go with row and permanent crops.

Despite a challenging macroeconomic backdrop and persistent geopolitical uncertainty, Canadian farmland remained resilient in 2025, holding its value and posting modest gains across much of the country. This performance reinforced farmland’s role as a defensive asset class amid soft commodity prices, elevated input costs, and trade‑related disruption.

Is it better to lease to farmers or directly operate farms in uncertain economic times?

Canadian investors today are navigating a complex macroeconomic backdrop marked by persistent inflation, slower growth, and rising unemployment (often signs of a “stagflationary” environment). These factors have contributed to increasing investment interest in farmland, which stands out as a compelling inflation-hedging, defensive asset. Its appeal lies in its scarcity, potential for productivity growth and therefore long-term capital appreciation, and its potential to generate consistent, uncorrelated, riskadjusted returns.

In this quarter’s newsletter, we take a closer look at how economic conditions are evolving, why they matter for farmland investors, and how different investment/ownership structures perform under pressure. Specifically, we compare direct invest-andoperate models with invest-and-lease strategies to help investors better understand how each approach behaves in a stagflationary environment, assessing which approach can deliver stronger downside protection and better risk-adjusted performance.are committed to the long-term sustainable future of Canadian agriculture.

At the heart of Bonnefield’s farmland investment model are the relationships we cultivate – not only with our investors, but with the farmers we support through our leasing solutions and who are stewards of the land. Our Property Management team plays a critical role in maintaining these relationships, conducting site visits, and evaluating opportunities to enhance the properties through additional investment.

The summer months are busy for our Property Managers as they travel across the country to visit every Bonnefield property and meet with our tenants. Over the course of three months, the team collectively visits over 133,000 acres of Bonnefield-managed farmland across seven provinces, collecting their fair share of Tim Hortons rewards points and picking up great stories and insight from the road. In this quarter’s newsletter we wanted to share a flavour of what they are hearing and seeing this season.

Meet the Team

Alayna – Calgary, Alberta

Region: Western Canada

Alayna brings a deep-rooted understanding of Canadian agriculture to her role as Property Manager, overseeing Bonnefield’s farmland properties across Western Canada. Raised on a grain farm in the Prairies, she combines firsthand farming experience with formal agronomic training and business expertise.

Before joining Bonnefield, Alayna spent eight years with BASF, one of the world’s leading crop input companies, where she worked closely with growers to provide tailored agronomic solutions. She holds a diploma in Crop Technology and a degree in Business, equipping her with both technical and strategic insight into the evolving agricultural landscape.

Alayna’s approachable, charismatic nature allows her to build strong, trusted relationships with farm partners – an essential quality in managing Bonnefield’s long-term farmland partnerships. Her on-the-ground knowledge of Prairie farming practices and products helps ensure our properties are managed sustainably and in alignment with the unique needs of local operators.

Alayna’s Summer So Far

“We’re increasingly having conversations with farmers who are exploring regenerative practices to improve soil health and long-term productivity of the land”, says Alayna. A recent example was in Northern Alberta, where Alayna and Investment Management team member, Mitch, met with a multigenerational row crop farmer growing canola, peas, wheat, barley, and oats. This tenant is actively working to rebuild soil structure on select parcels which had been degraded by previous operators. Bonnefield’s land makes up a meaningful portion of their operations, and together we’ve been working to address agronomic challenges over several years.

A key practice they’re trialing is the use of multi-species cropping, specifically underseeding canola with peas. This approach increases organic matter in the soil while reducing the need for synthetic nitrogen, as peas naturally address nitrogen levels in the soil. The goal is to lower input costs and gradually restore soil health. To support this transition, Bonnefield reduced the rental rate on these parcels, creating flexibility for the tenant to invest in these soil-enhancing practices. Over time, as the land increases in productivity, our rental rate will adjust to reflect the economics of these enhanced parcels. These types of collaborations, focused on soil remediation, input reduction, and long-term sustainability, are becoming an increasingly common theme of our tenant relationships.

Local Alberta Farmer

Patrick – Hamilton, Ontario

Region: Ontario

Patrick brings a unique blend of farming and agri-business experience to his role as Property Manager, where he supports the performance of most of Bonnefield’s farmland properties across Ontario. Raised on a multigenerational family farm, Patrick grew up working in his family’s direct-to-consumer apple orchard and played a key role in its transition to cash crop production. He remains actively involved in the current farm operations.

Patrick’s background, spanning both orchard and broadacre farming, makes him especially well-suited to work with Ontario’s highly diversified base of growers, who produce everything from apples, to ginseng, to wheat. He holds a degree in Economics and Finance from the University of Guelph and brings additional industry experience from his time as a Junior Trader with London Agricultural Commodities, and as a Business Development Representative with HD Mutual Insurance.

With firsthand farm knowledge and a strong foundation in agri-business and risk management, Patrick is equipped to build trusted relationships with farm partners and support Bonnefield’s long-term farmland stewardship in this dynamic region.

Patrick’s Summer So Far

A recurring theme that Patrick has been hearing from the field is that farmers are increasingly focused on expanding and diversifying their operations, particularly in today’s environment of heightened market volatility. Margins remain under pressure due to softer commodity prices, persistently high input costs, and elevated interest rates, while geopolitical uncertainty adds another layer of complexity. This kind of volatility isn’t new to farmers. They typically manage it by developing multiple income streams to strengthen and stabilize their businesses. Many established producers continue to pursue these strategies actively, aiming to build greater resilience and consistency across cycles.

A good example is a sixth-generation family farm in Southwestern Ontario that operates both cash crop and swine enterprises. On the cropping side, they grow corn, wheat, and soybeans, and are committed to soil health through practices such as reduced tillage and the use of cover crops where possible. Since partnering with Bonnefield last year through a leasing relationship on their cropland, they’ve been exploring opportunities to expand their hog operation as a strategic complement to their cropping business. With feed costs currently low and crop margins tight, this diversified income approach helps smooth earnings and reduce overall business risk.

This type of farmer: entrepreneurial, and focused on risk management, is a common operator profile with whom we like to work. They understand how to adapt to shifting market dynamics and take a proactive approach to long-term business sustainability. Their ability to scale thoughtfully and build resilience across operations makes them an ideal partner for Bonnefield. Most importantly, Bonnefield offers value to these types of operators as they think about the best uses for capital and investment to support their growth and diversification.

Winter Wheat, Ontario

Sean – Fredericton, New Brunswick

Region: Eastern Ontario & Maritimes

Sean manages Bonnefield’s farmland properties across Eastern Canada, working closely with farm partners to support the productivity and long-term sustainability of each property under management.

Raised on a small farm outside Stanley, New Brunswick, Sean developed a deep appreciation for farming early on. He holds a Bachelor of Science in Biology from the University of New Brunswick, and began his career in an agricultural microbiology lab where he supported seed potato certification and contributed to research on the transmission of Potato Virus Y (PVY).

Prior to joining Bonnefield, Sean was Agronomy Operations Manager at Resson Aerospace, an agriculture technology start-up focused on crop health and disease detection. In that role, he led projects across Canada, the U.S., and India, collaborating with farmers from a range of growing regions and crop types.

Sean’s background in farm operations, research, and agronomy allows him to build strong relationships with Bonnefield’s tenants and offer practical, informed support on the ground. In this way, Sean is able to work collaboratively with our farm partners to ensure they are successful while sustainably maintaining Bonnefield’s farm properties.

Sean’s Summer So Far

During Sean’s short hike up to our New Brunswick properties, a consistent theme he heard among potato producers is their openness to innovation and a strong focus on practices that boost crop yields and expand production capacity. This is largely driven by increasing demand from the region’s primary buyers, McCain and Cavendish, for whom most farmers grow under contract.

Enhancing yields remains a top priority, and local farmers are taking proactive steps to meet this goal. Many are trialling new potato varieties on select acres, targeting higher yields and more uniform tuber sizes. These trials help determine which varieties and techniques perform best in the region’s unique growing conditions. At the same time, farmers are adopting regenerative practices to improve soil health and long-term productivity. This includes using multi-species cover crops to build organic matter and enhance soil structure, as well as applying manure during off-potato years to further enrich the soil and support future crop performance. They are also working closely with local agrologists to refine spray regimens annually, helping to prevent disease resistance and ensure healthy crops.

In addition to optimizing production on existing acres, many farmers are also actively pursuing land expansion to meet future demand. Notably, the Grand Falls area is seeing infrastructure development that supports this growth, most significantly, the planned construction of a new train terminal near McCain’s potato processing plant. This facility will improve logistical efficiency, streamlining the movement of inputs and harvested crops in and out of the region.

Sean in Dufferin, ON

What About Tariffs?

Given the current geopolitical situation, our Property Managers have certainly engaged in interesting discussions about politics, economics, and market conditions. However, uncertainty and political and economic volatility are part of the normal realities for multi-generational farmers. While everyone has an opinion on the current situation, our Property Management visits this year have highlighted that despite short term uncertainty and volatility, a few common themes have emerged that highlight our farm partners’ focus on long-term success:

A willingness to innovate,

A focus on building operational resilience, and

An unwavering commitment to the land.

Despite the headwinds facing today’s farmers, from economic and political uncertainty to increasingly volatile weather, we continue to see examples of adaptability and forward-thinking approaches by tenants across our portfolio.

Our Property Management team remains committed to supporting this progress. By staying close to the ground, both literally and figuratively, they gain firsthand insight into what’s working and where support can make a difference.

As the growing season moves into harvest, the team will be keeping a close eye on yields, exploring opportunities for property enhancements, and beginning to plan for 2026 lease renewals. We look forward to sharing more from the field in the months ahead.

About Bonnefield Financial

Bonnefield is a leading Canadian farmland and agribusiness investment manager. We provide capital to progressive farmers and agribusiness operators through land-lease financing and non-controlling equity solutions. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers and agribusiness operators to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long-term sustainable future of Canadian agriculture.

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment. This communication is for informational purposes only and should not be relied upon for completeness. Any investment performance data outlined in this document should not be used to predict future returns. Any market prices, data, and third-party information are not warranted as to completeness or accuracy and are subject to change without notice. Prospective investors should take appropriate professional advice before making any investment decision. In all cases where historical performance is presented, note that past performance is not indicative of future results, and should not be relied upon as the basis for making an investment decision. There can be no assurance that any unrealized investments will ultimately be realized at the valuations taken into account in calculating the Funds performance presented herein, where applicable. The performance of such investments when ultimately realized may be materially different. This document may not be transmitted, reproduced, or used in whole or in part for any other purpose, nor may it be disclosed or made available, directly or indirectly, in whole or in part, to any other person without Bonnefield’s prior written consent.

Copying, distributing or sharing this document or its contents is expressly prohibited without the express, written consent of Bonnefield.

Canadian Agriculture: Assessing our Exposure to Potential U.S. Tariffs

In recent months, U.S. trade policy has taken center stage, with heightened rhetoric around tariffs and the potential for retaliatory actions from global trading partners. While no new U.S. tariffs have been implemented on Canadian agriculture, for investors in the space, the question still naturally arises: How vulnerable is the sector to these developments, and what are the implications for farmland investment?

At Bonnefield, we have been analyzing these questions closely. While there is no simple answer, understanding potential exposure, and the structural factors that can help mitigate it, is essential. Amid broader near-term macroeconomic and geopolitical uncertainty, we remain confident that Canadian farmland will once again prove to be a resilient, long-term store of value. In fact, tariff uncertainty further reinforces the case for investing in tangible, productive, and uncorrelated assets like high-quality Canadian farmland.

Key Factors That Will Determine The Impact of U.S. Tariffs

Although the full effects of potential future U.S. tariffs on Canadian agriculture are difficult to forecast, we generally expect some short-term downward pressures on commodity prices, and the actual impact will vary depending on the commodity and its reliance on the U.S. market. (We provide a more detailed analysis of key crops and export destinations later in this newsletter).

Several variables will influence the outcome:

The ability of U.S. importers to absorb or pass on tariff-related costs

Consumer response in the U.S. and the substitutability of Canadian products

The extent to which Canadian consumers respond to U.S. tariffs with additional demand for Canadian products

The scope and duration of the tariffs

Canada’s potential retaliatory measures

Broader global supply chain shifts prompted by U.S. protectionism

Ultimately, the global nature of agricultural commodity markets provides a natural buffer from potential tariff impacts as demand displaced by one market often finds a home in another. We saw this pattern emerge when India placed barriers on Canadian lentils in 2017, and when China restricted purchases of Canadian canola in 2019. In both these cases, Canadian production went elsewhere (largely to the EU) to supply crop shortages created by China and India’s changing trade patterns.

Mitigating Forces Supporting The Sector

Several macroeconomic and sector-specific dynamics are poised to help offset the potential downside:

1. Lower Interest Rates

In a recessionary environment, interest rates are likely to remain low or even decline, helping to alleviate some of the financial pressures faced by Canadian farmers.

2. Favourable Currency Dynamics

A weaker Canadian dollar provides a natural hedge for producers, as most agricultural commodities are priced in U.S. dollars. This supports Canadian export competitiveness and farmer profitability, even amidst tariff disruptions.

3. Government Support

Historically, the Canadian government has acted to support the agriculture sector during times of stress. For example, during the 2018–2019 trade dispute with China, the Canadian government provided $150 million in insurance support to canola exporters and expanded the Advance Payments Program, offering up to $1 million in loans – half of which was interest-free for canola producers.(1),(2)We would expect policy intervention if tariffs were to cause sustained disruption.

4. Export Market Diversification

The global nature of agriculture means that if one region imposes trade restrictions, others often increase their purchasing to fill the gap. Canada’s growing network of trade agreements supports this flexibility.

5. Low Agricultural Stockpile

Demand from a growing worldwide population, combined with years of geopolitical and climate change induced production challenges, have resulted in declining global stocks-to-use ratios for most agricultural commodities, e.g., corn stock-to-use ratio is currently at a 10-year low.(3)Consumers around the world will need Canadian crops, regardless of US tariffs and trade disruptions.

U.S. and Canadian Agricultural Trade Flows Have Changed in Recent Years

Most Canadians are surprised to learn that in the last decade, Canada has gone from being a net importer of food from the U.S. to a net exporter.(4) This is true of bulk agricultural commodities (like grains) as well as for intermediate goods (like livestock and feed) and even for branded consumer food products. On the face of it, being a net exporter to the U.S. would suggest that Canada is more vulnerable to U.S. agricultural tariffs than when we were a net importer. However, it is also true that U.S. food manufacturers and end consumers are much more reliant on Canadian crops than they were even a decade ago. A February 2025 policy note from Agrifood Economic Systems concluded:

“…on a net basis, Canada is feeding the U.S.. Tariffs that increase the price of agri-food products imported by the U.S. from Canada will cost U.S. consumers. If tariffs are sufficient to effectively halt Canada-U.S. trade in some products, the U.S. will be shorted in these products to some degree, for some period of time, and prices could increase sharply.” (5)

On balance, U.S. reliance on Canadian farmers suggests that agricultural tariffs are likely to have a big impact on U.S. producers and consumers and are, therefore, likely to be short lived if implemented.

The China Factor

While the focus of much attention is on U.S. tariff policy, Chinese tariffs (both on the U.S. and on Canada) are also important to consider. China’s recent imposition of a 100% tariff on Canadian canola oil and meal, along with a 25% tariff on seafood and pork, marks a significant escalation in the ongoing trade tensions between the two nations. These measures, effective from March 20, 2025, were introduced in direct response to Canada’s earlier decision to levy a 100% tariff on Chinese electric vehicles and a 25% tariff on steel and aluminum imports – actions that Canada justified as necessary to counteract unfair subsidies and market distortions by China.

As noted earlier in this newsletter, China has taken similar steps in the past, most notably in 2019, when it suspended import permits for major Canadian canola exporters. Although this move initially disrupted Canadian canola exports, the industry demonstrated resilience by diversifying its markets and finding alternative buyers. That episode, like the current one, initially disrupted trade and put downward pressure on farm margins and cash receipts. But Canadian producers quickly adapted: displaced volumes found new homes, largely in the EU, where supply gaps created by shifting global trade patterns provided new market opportunities. The current situation is likely to follow a similar trajectory. We also note that China’s current tariffs target canola oil and meal, which are considered processed forms of canola. Most of China’s canola imports from Canada consist of unprocessed canola, such as seeds, (e.g. in 2024, ~80% of canola exported to China was unprocessed) and therefore, the overall impact of these tariffs is relatively limited.(6)

These recurring patterns speak to the resilience of Canadian agriculture and the buffering effect of globally integrated commodity markets. While near-term volatility in prices and cash flows is expected, past experience suggests that Canada’s export-oriented producers are well positioned to weather this period of uncertainty. Diversification of markets and continued investment in trade infrastructure will remain key to mitigating future shocks and maintaining long-term sector stability.

These dynamics are not unique to Canada. Recent Chinese tariffs on U.S. agricultural products, including soybeans and corn, have similarly demonstrated that in a globally undersupplied market, protectionist measures often result in a rerouting of trade rather than a net reduction in supply. As China reduces its reliance on U.S. commodities, countries like Brazil and Argentina have stepped in to meet demand. China’s share of soybean imports from the U.S. fell from 40% in 2016 to 18% in 2024, while Brazil’s share rose from 46% to 74% during the same period. Brazil has also surpassed the U.S. as China’s top corn supplier since gaining market access in 2022.(7)These shifts underscore the adaptability of global supply chains and the limitations of tariffs as a tool for influencing long-term trade dynamics. For Canadian producers, this reinforces the importance of maintaining access to diversified markets and investing in the agility needed to respond to changing global conditions.

Diversification of Canada’s Export Markets is Well Underway

Canada has actively expanded its agricultural trade relationships beyond the U.S. through landmark agreements such as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and the Comprehensive Economic and Trade Agreement (CETA) with the EU. These agreements have unlocked access to new, high-growth markets for Canadian crops, strengthening the sector’s global competitiveness and reducing risks related to overreliance on any single jurisdiction.

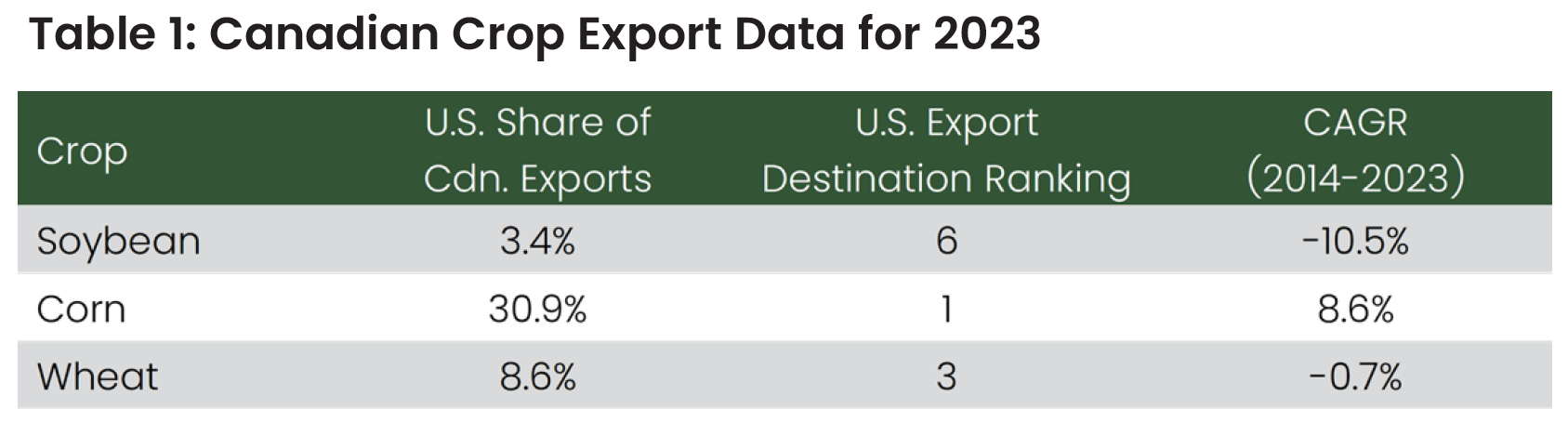

Bonnefield recently undertook a review of its farmland portfolios to evaluate likely exposure to the U.S. market. Three of the largest exposures in our portfolios are soybeans, corn, and wheat, which are also the major crops exported by Canada. The table below outlines the U.S.’ share of Canadian exports for each key crop in 2023, its ranking as a key export destination, and the associated compound annual growth rate (CAGR) from 2014-2023, based on total dollar value exported in CAD for each of these crops.(8)

The takeaway from this data should give Canadian farmland investors comfort.

Soybeans: The U.S. share of Canadian soybean exports has steadily declined, with growing demand from Asia and the Middle East driving future growth.

Wheat: Similarly, wheat exports have shifted away from the U.S., also favouring Asian and Middle Eastern markets.

Corn: While the U.S. saw a spike in corn imports from Canada in 2023, European markets, particularly Ireland, Spain, and the U.K., have been rapidly gaining ground, with impressive CAGRs of 19.2%, 8.7%, and 27.2%, respectively. In fact, these three countries represented over 60% of Canadian corn exports in 2023.(9)

This diversification highlights the growing resilience of Canada’s export ecosystem and its ability to adapt to evolving global trade dynamics, specifically in times of trade embargoes and tariffs from certain jurisdictions. Internally, Bonnefield continues to prioritize business development in regions with diverse crop capabilities and export access.

Long-Term Outlook: Still a Strong Case for Investment

Despite near-term trade uncertainty, we believe Canadian agriculture remains fundamentally strong. Canadian farmland continues to offer a compelling investment thesis grounded in:

Stable, uncorrelated returns

Limited volatility relative to other asset classes

Long-term supply/demand imbalances in global food and energy markets

Tariffs may bring temporary volatility, but they do not alter the long-term drivers of farmland value: population growth, dietary shifts, and the transition toward renewable energy sources.

Importantly, periods of market disruption often create attractive entry points. In a sector that has historically suffered from underinvestment, the current environment presents an opportunity to deploy capital in ways that enhance productivity, support farmers, and drive long-term value creation.

In Summary

Canadian agriculture remains fundamentally sound and increasingly diversified. Bonnefield’s portfolio strategy, rooted in high-quality farmland with broad market access, is well positioned to navigate volatility and capitalize on opportunity even in the face of potential U.S. tariffs.

About Bonnefield Financial

Bonnefield is a leading Canadian farmland and agribusiness investment manager. We provide capital to progressive farmers and agribusiness operators through land-lease financing and non-controlling equity solutions. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers and agribusiness operators to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long-term sustainable future of Canadian agriculture.

Sources

1. Government of Canada, “Canada backs Canadian canola farmers and exporters with $150 million in insurance support,” June 13, 2019.

2. Government of Canada, “Government of Canada implements new regulations to enhance Advance Payments Program,” June 3, 2019.

3. MacroMicro, “World – Corn Stocks-to-Use Ratio” as of April 2025.

4. Government of Canada, “The United States’ trade with Canada and Canada’s trade with the United States,” February, 2024.

5. Al Mussell, Douglas Hedley, and Ted Bilyea, Canadian Agri-Food is Highly Vulnerable to US Tariffs. The US Should Worry Too, Agri-Food Economic Systems, February 2025.

6. Canola Council of Canada: Profiles of Canada’s leading canola markets. August 2024.

7. Reuters, “Chinese buyers switch to cheaper Brazilian soybeans ahead of Trump return,” January 17, 2025.

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment. This communication is for informational purposes only and should not be relied upon for completeness. Any investment performance data outlined in this document should not be used to predict future returns. Any market prices, data, and third-party information are not warranted as to completeness or accuracy and are subject to change without notice. Prospective investors should take appropriate professional advice before making any investment decision. In all cases where historical performance is presented, note that past performance is not indicative of future results, and should not be relied upon as the basis for making an investment decision. There can be no assurance that any unrealized investments will ultimately be realized at the valuations taken into account in calculating the Funds performance presented herein, where applicable. The performance of such investments when ultimately realized may be materially different. This document may not be transmitted, reproduced, or used in whole or in part for any other purpose, nor may it be disclosed or made available, directly or indirectly, in whole or in part, to any other person without Bonnefield’s prior written consent.

Copying, distributing or sharing this document or its contents is expressly prohibited without the express, written consent of Bonnefield.