Sustainability has become an increasingly prominent theme in many industries, and the same is true of agriculture. Agriculture and agrifood system sustainability has drawn attention from both sector participants as well as policymakers and other stakeholders. As a notable and recent example, a full day of 2023’s UN Climate Change Conference COP28 conference in Dubai was dedicated specifically to food and agriculture, representing a landmark first for any COP.(1)

When we consider where and how the world’s food will be grown for future generations, there is a clear impetus to ensure a sustainable global food system that will provide continuity of supply for a growing global population, while preserving – and improving – the land resources that are required to produce food. Initially coined in the early 1980s by U.S.-based organic research center the RodaleI nstitute, the term “regenerative agriculture” has been in the spotlight in the media, politics, academia, and the global business community in recent years.(2)

This might bring a few questions to our readers’ minds:

How is “regenerative agriculture” defined?

Why is it relevant?

What are the associated challenges and opportunities?

Where does Canada stand compared to its global peers?

Defining Regenerative Agriculture

Despite recent widespread use of the phrase, there is no singular, universally accepted legal or regulatory definition for “regenerative agriculture”.(3) This sets the idea of regenerative agriculture apart from a conceptually similar, but distinct phrase “organic”, and the related descriptive prefixes “bio-” and “eco-”, which are legally defined and protected in Europe, amongst other jurisdictions.(4)

Instead, the term “regenerative” is used to refer to various practices (e.g., the use of cover crops, or reducing or eliminating soil tillage), desired outcomes (e.g., better soil quality, or more biodiversity), or some combination of the two.(3) Despite the lack of consensus as to what exactly regenerative agriculture entails, there is some agreement that the main principles and objectives of regenerative agriculture are to promote a holistic view of the global food system to improve soil health, the broader environment, human health, and economic prosperity.(4)

Similarly, McCain Foods – a Canadian leader in the global food industry that produces one in every four French fries consumed across the world(5) – concisely defines regenerative agriculture as:

“… an ecosystem-based approach to farming that aims to improve farmer resilience, yield, and quality by improving soil health, enhancing biodiversity, and reducing the impact of synthetic inputs.”(6)

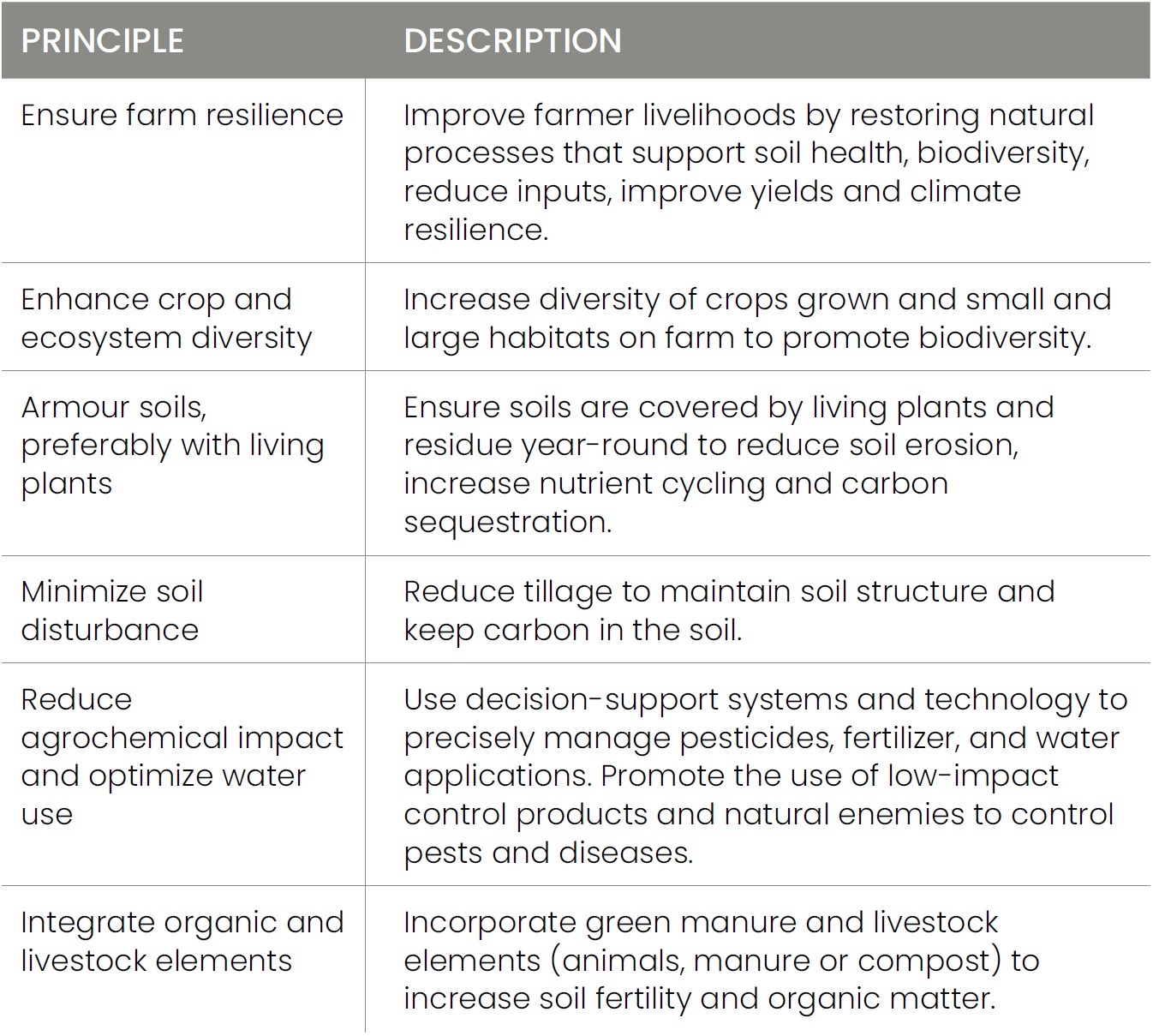

Outlined in McCain Foods’ Regenerative Agriculture Framework is a set of six principles that can be applied to growing potatoes. Many of those principles can also be applied in the context of growing crops such as wheat, corn, soy, peas, or higher-value fruits and vegetables:

At a glance, some of these principles may seem different than what many would think are incorporated into conventional farming practices. However, based on Bonnefield’s decade-plus experience managing portfolios of high-quality Canadian farmland properties, we have observed that many Canadian crop farmers have employed practices that align with these concepts for years, and often seek opportunities to further improve. Anecdotally, Canadian farm operators acknowledge that sustainable practices can enhance yields and crop quality, while also enhancing and supporting farmland values and long-term production.

Why is Regenerative Agriculture Important?

Global food production has had to scale significantly to support rapid population growth. In the second half of the 20th century, crop yields increased at an unprecedented pace; cereal yields increased by 207% over the five decades between 1961 and 2021 while the total land area used for cereal production increased by just 14%.(8)

This agricultural intensification – or increased crop production on a relatively similar amount of land – has largely been achieved through the strategic use of chemicals (e.g., fertilizer, pesticides, fungicides, and herbicides), crop irrigation, mechanization and technology (e.g., improved and more-efficient farm machinery, precision agriculture technology), and improved seed genetics that have improved seed genetics that has strengthened plant resilience plants’ resilience to disease, drought, and other material risks.(8)

The global population is expected to reach 8.5 billion by 2030 and grow even further to 9.7 billion 2050(9), meaning that the world’s demand for food will continue to increase. However, this growth also means that land that is currently uninhabited or used for other purposes – like farming – will face additional pressure (and, likely, decline) as cities expand to accommodate more people.

A delicate balance must be struck between the need for sufficient, nutritious food and the need for housing, both at home in Canada and across the world. From an agricultural perspective, this underscores the need to employ practices to increase production, while also supporting the sustainability of this finite resource will be critical over the coming decades.

Opportunities &Challenges

As we consider future demand for crop production in a world with declining arable land, the idea that agricultural practices should shift to incorporate increasingly sustainable practices may seem daunting but necessary. On one hand, it may take several years for farmers that currently rely on less-sustainable farming practices such as sustained mono-cropping (i.e., planting the same crop type for multiple consecutive years) to successfully transition to more regeneratively-minded practices. This transitionary period requires an investment of capital, inputs, and time that will impact crop production for at least one to two growing seasons.(10) However, those with a multi-generational view of farming acknowledge that without sustainable practices, the long-term feasibility of the farm operations will be negatively impacted.

In addition to the costs of transition, some question whether regenerative agricultural practices will allow farmers to maintain current production levels. A three-decade field study conducted by the Rodale Institute found that, following the initial transition period, there is typically little if any difference in crop yields on conventional farms vs. regenerative farms.(10) In addition, the study found that the regenerative fields studied outperformed their conventionally farmed counterparts during stressful conditions, particularly droughts, as the regenerative fields were better able to retain water.(10) Beyond the lack of long-term impact to crop yields and fact that regenerative practices also contribute positively to global climate change initiatives, the potential benefits include:

Reduced costs over time resulting from decreased need for raw inputs

Enhanced soil quality, moisture retention, and nutrient balance which can support strong yields and high-quality crops

Increased on-farm water availability for non-irrigation usage, or an overall reduced need for water

Potential access to financial assistance through grants or other non-governmental programs

How is Canada Positioned?

As consumers and other stakeholders have begun to demand increased sustainability and accountability across the entire agrifood value chain, value-added processors have demonstrated a meaningful desire to work with farmers who are sustainability-minded.

Large processors are already positioning themselves to meet growing demands for sustainably-sourced agrifood products. As one recent example, McCain has made an ambitious commitment to source 100% of its potatoes from regenerative farms by the end of 2030.(7) While definitions of regenerative farming may differ between enterprises, we believe that this approach is broadly reflective of the industry’s overall tone and direction looking ahead. This means that for Canadian farmers to remain competitive, they will likely need to incorporate (or continue to utilize) regenerative farming practices in their operations.

The importance of innovation and the role of regenerative farming practices in ensuring the sustainability of Canada’s agriculture industry is not new to farmers. The most recent Census of Agriculture found that while the area of farms across the country declined by approximately 3% between 2016 and 2021, many Canadian farmers implemented precision technologies designed specifically to enhance efficiency and yields, and nearly 65% of operators reported that they engaged in sustainable farming practices.(11) This data points to farmers’ understanding that leveraging these advancements is crucial and, while the field of regenerative agriculture will keep evolving, we believe that Canadian farm operators will continue to demonstrate the adaptability and resilience for which they have become known.

A Supportive Partner for a Sustainable Future

Recognition of Canadian agriculture’s role in the context of global food security, water scarcity, and climate change has underpinned Bonnefield’s business model since the firm’s founding over a decade ago. This includes playing a role as a supportive, non-controlling, partner to progressive Canadian farmers and agribusiness operators as they consider how best to grow for the future.

As one example of our inherent support for agricultural sustainability practices, Bonnefield’s Standards of Care – a set of agronomic best practices developed in conjunction with industry experts to preserve and enhance farmland through sound land management principles – are an integral part of each of Bonnefield’s farmland lease contracts. This hallmark component of our farmland sale-leaseback model includes parameters that are designed to protect and enhance soil health, ensure responsible resource usage, and to generally promote good land stewardship. At a high level, the Standards of Care align to some of the core principles of regenerative agriculture, with a view to both ensuring the long-term productivity of the farms owned by our funds and their long-term value.

Beyond the Standards of Care, Bonnefield actively contributes to the enhancement of Canada’s agricultural industry and long-term sustainability. We have been active participants in the ongoing development of Canada’s National Index on Agri-Food Performance and in August 2023, Bonnefield joined Farm Credit Canada, Manulife Investment Management, and McCain Foods to launch the Canadian pilot of Leading Harvest – a third-party audited Farmland Management Standard designed to promote sustainable agricultural practices.

It is clear that weaving sustainable principles into the fabric of the industry will be an essential part of Canadian agriculture’s growth story, particularly as it becomes more essential than ever in a global context. As a trusted partner to farmers and agribusiness operators, Bonnefield will continue to support progressive farmers and value chain participants as we build a brighter, and sustainable, future for Canadian agriculture.

About Bonnefield Financial

Bonnefield is a leading Canadian farmland and agriculture investment manager, providing financing to progressive farmers and agricultural operators through land-lease and non-controlling equity solutions. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented operators to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long-term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.

Understanding the Impact of Wildfires on Canadian Agriculture

2023 has so far proved to be Canada’s most intense wildfire season in history. At the time of writing, approximately 135,000 square kilometres of forest and other land has been burned by wildfires and forest fires (collectively referred to as “wildland fires”) since the beginning of the year(1). This amount surpasses the previous record for area burned in a single year, which was set in 1989 when 75,596 square kilometres of land across Canada was affected by fires(2). The total amount of land burned to date in 2023 is more than seven times the average area burned per year over the past decade(3).

While there have been numerous evacuation orders across Canada in recent months due to fires, we are relieved and thankful to report there has been no direct impact to any of Bonnefield’s farms as of the time writing. It is important to note that Canadians living and working in rural areas – including farmers and agribusiness operators, as well as the communities of which they are a part – are most directly impacted by these events.

As Canada is home to expansive forests and grasslands, fires are not an unusual occurrence in summer months. Wildfires and forest fires typically occur beginning in May and through to September, with most fires occurring in remote areas(4). However, the intensity of wildfires in 2023 begs the question “why did this year’s wildfire season eclipse prior years so significantly, and what is the potential impact to Canada’s agricultural sector?”

An Unusually Intense Fire Season

For context, the Canadian Interagency Forest Fire Centre reported that there were approximately 900 active wildfires as of mid-July, most of which were considered uncontrolled burns(5). Through May and June, wildfires persisted in Northern Alberta and Northern British Columbia, and forest fires in Northern Quebec led to unprecedented levels of wildfire smoke and poor air quality across Quebec and Ontario as well as parts of the Northeast United States(4). By late June the total amount of Canadian land burned by wildfires in 2023 surpassed the total area burned in 2016, 2019, 2020, and 2022 combined(6) and, in mid-July the federal government mobilized the Canadian Armed Forces and the Canadian Coast Guard to assist with firefighting efforts in British Columbia(7).

There are three key factors that lead to wildfires and forest fires: 1) ignition (either lightning or due to human activity), 2) hot and dry weather, and 3) vegetation (trees, shrubs, and brush) which is made drier and more flammable by arid weather conditions(8). It is believed potential cumulative effects of climate change, along with woodland management practices, have increased the risk of fires starting and rapidly spreading(9). More specifically, drought conditions, high temperatures, and increased frequency of lightning strikes – which start roughly half of Canada’s fires – are thought to be the main climate change-related effects that are contributing to heightened wildfire risk(9).

This summer has been exceptionally hot with record-breaking high temperatures observed globally. In fact, the U.S. National Oceanic and Atmospheric Administration recently reported that June 2023 was the warmest June since global temperature record-keeping commenced in 1850, and the European Union’s Copernicus Climate Change Service indicated that the first two weeks of July 2023 likely represented the warmest two weeks in the planet’s history(10).

In a recent briefing, Northern Forestry Centre at the Canadian Forest Service director general Michael Norton discussed the impact that continued unusually warm and arid conditions across Canada through the summer months will likely have through the rest of the season, stating that “expected warm and dry conditions will increase wildfire risk from British Columbia and the Yukon across the country right to Western Labrador”, and that “it is anticipated that many parts of Canada will continue to see above normal fire activity”(9).

Where do Fires Occur, and How Are They Managed?

Canada is home to the third-largest forest area in the world with over 3.6 million square kilometers of forests, representing approximately 40% of the country’s total land base(11). Only 6% of Canada’s forests are privately owned by non-governmental entities such as forest companies and private owners (e.g., family-owned forests and woodlots), with provincial and territorial governments owning 90% and the federal government owning the remaining 4%(12). The primary areas that experience “normal course” wildland fire activity are southern British Columbia, and across the boreal forest that extends from Alaska across the northern parts of British Columbia, the Prairies, Ontario, Quebec, and the Maritimes(13).

Much of the country’s forested land is remote and sparsely inhabited; however, approximately 17% of that land is considered part of Canada’s wildland-urban interface (WUI)(14), where homes and community structures, commercial and industrial activity, and infrastructure such as roads and railways meet or intermingle with forested areas(15). Wildfires pose a significant risk to WUI areas due to their proximity to the natural vegetation that serves as fuel for wildfires. Researchers have also noted that in these areas, there is also an increased risk of fires being started due to human ignition(16). Moreover, the threat posed to WUI areas by wildfires is growing both in Canada and elsewhere as urban areas continue to expand into wildlands and existing rural areas experience population growth.

The 2016 Horse River Wildfire in Northern Alberta serves as a particularly significant example of wildfire risk in Canada’s WUI. Though firefighters attempted to suppress the blaze that began southwest of the town of Fort McMurray, Alberta, the fire grew extremely quickly as result of hot and dry weather; ultimately, 80,000 people were evacuated from the area and more than 2,400 man-made structures were lost as result of fire(17). The estimated total economic impact of the Horse River Wildfire was nearly $9 billion, and the event represents the most expensive insured natural disaster in Canadian history(18). While it is an extreme example, the Horse River Wildfire illustrates just how quickly wildfires can evolve into large-scale disasters with significant detrimental impacts.

Given the toll that Canadian wildland fires can take in a given year, it is important to consider where responsibility lies for fire management and how fires are managed. As noted, the majority of Canada’s forests are owned by provincial and territorial governments, which also have responsibility for wildland fire management in their respective jurisdictions(19). Federal government agencies are responsible for wildland fire management in select areas including national parks and military bases(19), and Canada has also entered into agreements with other countries, such as the United States, to share firefighting resources and expertise(20).

It is worth noting that Canada’s approach to wildfire management has shifted over time. Fire suppression (fully putting out fires) was historically the primary goal of wildfire management strategies until the 1970s when recognition of fire’s ecological benefits to forests began to grow(19). The current approach to wildfire management across the country involves various levels of fire suppression ranging from complete extinguishment to limited (or no) intervention, and the decision as to whether to fight a fire or let it burn out naturally is made by the government agency responsible for fire management in the area where the fire is occurring, based on that agency’s hierarchy of fire management priorities(19). While many fires are left to burn out naturally, active fire suppression generally takes place within the southern parts of the boreal forest where human activities such as forest harvesting, mining, urban developments, and agriculture are more concentrated(14).

Fire’s Impacts on Canadian Agriculture

Wildfires present numerous risks to people, property and economic activity, though some may be less immediately apparent than others. In addition to the direct risk to human life and property, poor air quality as result of lingering fire smoke can have serious adverse health effects, such as respiratory illnesses and psychological distress(21).

From an agricultural perspective, crop yields may also be impacted by fire smoke due to reduced sunlight levels that can impact the photosynthesis process necessary for plant maturation, as well as increased ground-level ozone that can be damaging to plant tissue(22). As it is impractical for scientists to conduct controlled experiments involving wildfire smoke and thus difficult to specifically isolate the effects of smoke from other factors that ultimately determine crop yields, the direct impact that wildfire smoke has on crop production is unknown; however, this remains an active area of research, and scientists often focus on measuring the effects of smoke events as they occur(22).

Additionally, it has been reported that prolonged exposure to smoke can affect the taste of fruits and vegetables(23). As one example, following the wildfires that affected British Columbia’s Okanagan Valley in 2021, winemakers in the region conducted lab tests on their grapes and found that high levels of airborne smoke molecules had been absorbed by the fruit(24). Ultimately, this led to wines that were bottled in the region that year being affected by “smoke taint”, or an ashy flavour profile that many winemakers view as a negative impact to the quality of the wine that can reduce the end product’s appeal and affect the marketability of a wine vintage(24). Smoke taint may be less of a concern for farm operators who primarily grow row crops that are more commodity-like in nature and are often processed into higher value products such as seed oils. However, the economic impacts of smoke on higher-value crops including fruits and vegetables may become a greater concern for some Canadian farmers over time as wildfires become more frequent and more intense.

Understanding & Managing Investment Risks

As a leading Canadian farmland and agriculture investment manager, we believe that it is necessary to understand the risks associated with investing in Canadian farmland to the fullest extent possible. Since inception, Bonnefield’s investment process has considered regional risk factors that can impact farming including regional soil types, typical area weather patterns, water availability, as well as investment-specific characteristics such as topography, drainage, and other similar attributes.

Though some risks (such as large-scale wildfires, or intense droughts or floods) are difficult to predict and quantify, Bonnefield has contemplated environmental risks as part of our investment process since the firm’s inception and our team has continued to enhance our analysis of these risks over time. A few examples of how our team has integrated major environmental risks into the investment process include:

Collaboration with our extensive network of farmer partners and industry participants, such as agrologists, appraisers, and brokers, to understand and determine specific nuances of environmental risks (e.g., flooding, hail) that affect a particular region;

Leveraging satellite imagery and historical environmental data to better understand both long-term and recent climatic trends and conditions; and

Using underwriting models that include multiple scenarios (e.g., different levels of crop yields) and risk premiums appropriate for a farmland property in a specific region.

As we look ahead to the remaining summer months and beyond, it seems clear that wildfires, along with other major climate and weather events, will continue to be a major theme. However, we are heartened knowing that Bonnefield properties have not to date been directly impacted by this year’s fire activity. We also recognize that a single year of increased wildland fire activity, while notable, is not enough to draw meaningful conclusions from, or change our current practices. Indeed, a year like 2023 provides valuable insight and data to refine our understanding of climate and other risks facing the agricultural industry in Canada. Bonnefield will continue to monitor developments and use this information to support both our farm partners and our investors.

About Bonnefield Financial

Bonnefield is a leading Canadian farmland and agriculture investment manager, providing financing to progressive farmers and agricultural operators through land-lease and non-controlling equity solutions. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented operators to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long-term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.

How do We Strike the Balance Between Farmland and Housing?

Farming and agribusiness are essential parts of Canada’s economy. Canada’s agricultural and agri-food sector is a major economic driver for the country that generates over $100 billion of gross domestic product (GDP) and employs over 2 million people(1). However, while Canada is one of the largest countries in the world with a total land mass of approximately 2.5 billion acres(2), in 2021 only 154 million acres (or 6%) of the country’s land was used for farming(3).

As the global population continues to grow there is a natural stress created in balancing the need for agricultural land to support sustainable food production, and increased urbanization to support housing and industry growth. Over recent months, events in the province of Ontario have offered a glimpse into the competing demands on land and highlighted the importance of well developed, long-term and sustainably minded policies and practices with respect to land use.

Ontario – Home to Many and Continuing to Grow

Though only the fifth largest of Canada’s provinces and territories by land area (representing approximately 10% of the country’s land mass), Ontario is the nation’s most populous province and is home to nearly 40% of the country’s total population(4). As such, the province is a major contributor to Canada’s economy, including Canada’s agricultural sector. In 2021, Ontario had the largest number of farms and farm operators of any province, was the second-largest contributor to Canada’s farm revenues and led other provinces in farming key crops such as soybeans and corn(5). The Ontario Federation of Agriculture (OFA) estimates that agriculture contributes $47 billion annually to the province’s GDP while generating nearly 750,000 jobs(6). Additionally, more than half of the highest-quality farmland in Canada is located within Ontario(7).

Despite already being the nation’s most populous province, Ontario continues to grow. The province’s population grew by 24% from 11.4 million in 2001 to 14.2 million in 2021(8). Current projections indicate that Ontario’s population will grow by more than 35% to surpass 20 million within the next 25 years, with the Greater Toronto Area expected to grow the fastest at a rate of over 40% over that same period(9).

However, Ontario’s population growth in recent years has not been met by a commensurate increase in the supply of housing that is both suitable and affordable; it has been reported that home prices and rents in many Ontario cities are now among the highest in the country, and rental vacancy rates have fallen to near pre-pandemic levels(10). Further, the average price of a house in Ontario reportedly increased by 180% over the course of a decade, whereas incomes grew at just 38%(11).

In December 2021, the Ontario government appointed a new Housing Affordability Task Force to help develop a set of recommendations on measures to address housing supply and affordability(12) and, in February 2022, the Task Force released its summary report detailing more than 50 recommendations to the province(12). The measures outlined in the report centered on creating more housing supply and proposed that Ontario adopt a goal of building 1.5 million new homes over the next decade(12).

Policymakers have been presented with the challenge of balancing the needs of a growing population and protecting valuable natural resources – including some of the richest, most productive farmland in the country. It is clear that more homes, particularly affordable housing options, will be needed to house Ontarians, but it is also true that more food will be needed in order to feed a growing population.

Farmland: A Valuable, but Finite, Resource

Though advancements in technology and practices have improved the efficiency of Canadian farms, thus reducing the total acres required to generate strong crop yields, the continued decline of farmland acreage across the country raises the question of where crops will be grown in the future. According to Statistics Canada’s Census of Agriculture data, the total area of Canadian farms declined by over 13 million acres between 2001 and 2021(13), which is roughly equivalent to losing an average of seven small farms per day over the past two decades(14).

Despite the major role that agriculture plays locally within Ontario, farmland loss has been a notable long-term trend in the province. Total agricultural acreage in Ontario has fallen by nearly 20% over the past 35 years(15), and the OFA estimates that the province’s farmland acreage shrank at a rate of 319 acres per day in 2021 – which is a sharp increase of 80% compared to the 175 acres lost per day just five years prior to that in 2016(16). Even more striking, if the current pace of farmland loss continues, 25% of the farmland that exists today in Ontario could disappear within the next 25 years(17).

Beyond its economic impact, Ontario’s agriculture industry has demonstrated significant progress and leadership in terms of sustainably minded farming practices. The number of Ontario farms reporting renewable energy production (such as through the use of solar panels or wind turbines) increased by more than 60% between 2016 and 2021, and the province had the highest proportion of farms planting winter cover crops – which are beneficial for long-term soil health – as compared to other provinces across Canada(5). Put simply: agriculture is essential to Canada, and Ontario is essential to Canadian agriculture.

Policy Responses Continue to Shift

Starting in 2005, the Ontario government established a series of policies, including the Provincial Policy Statement, the Greenbelt Plan, and the Growth Plan, designed to regulate urban sprawl and protect the province’s sensitive environmental and ecological features, such as wetlands and farmland(18). Though these measures may have slowed the rate of residential and commercial land development that would otherwise have occurred were they not in place, it is still clear that Ontario’s farmland base has diminished significantly in recent decades.

Following the Housing Affordability Task Force’s Summary Report in 2022, Ontario’s provincial government has tabled several bills with the aim of seeing 1.5 million new homes built by 2031. Among these pieces of legislation have been Bill 109: More Homes for Everyone Act, 2022 which was passed in April 2022[xix]; Bill 23: More Homes Built Faster Act, passed in November 2022(20); and, most recently, Bill 97: Helping Homebuyers, Protecting Tenants Act, 2023 was passed in June 2023(21).

These pieces of legislation collectively introduced major changes to the policy framework that governs where, how, when, and how quickly land can be re-developed for residential use, and have been met with mixed feedback from municipalities, environmental groups, and other stakeholders, including several of Ontario’s farming industry organizations.

Bill 97 & Demand for Ontario Farmland

The most recent example of housing-focused provincial legislation in Ontario is Bill 97. The policy changes encompassed under Bill 97 are wide-ranging and will make it easier for developers to build on agricultural land. Once such policy change will enable municipalities to expand their boundaries outwards and rezone agricultural land for development, without requiring evidence of need, or further environmental studies(22). Bill 97 would also strengthen the use of “Minister’s Zoning Orders” (MZOs), which allow the provincial government to override local municipalities’ existing land zoning rules and planning processes to directly change how specific pieces of land can be used – for example, turning land that is zoned for agriculture into residential or commercial developments(22).

Though Minister’s Zoning Orders have historically been issued by the provincial government in limited, extraordinary circumstances, they have been used more frequently in recent years to expedite residential and industrial development projects across Ontario(23). MZOs are seen by some local governments as a valuable tool when used responsibly and consistently to help support communities’ needs (e.g., to accelerate housing projects that include affordable units), however, it is also worth noting that MZOs do not require public consultation and cannot be appealed(23) In 2021, the Ontario Auditor General found that no formal process exists for interested parties to request MZOs, nor are there established criteria for approval(24). The Auditor General’s 2021 report on Ontario’s land-use planning tools and practices noted that “lack of transparency in issuing MZOs opens the process to criticisms of conflict of interest and unfairness”, and that MZOs are disruptive to land-use planning processes that would otherwise normally require years of consultation and preparation(24).

Bill 97 also initially included a clause that would allow municipalities to divide large farms into smaller land lots, with a view to making it easier to build homes(25). More than a dozen farming organizations including the Ontario Federation of Agriculture issued a joint letter to the Ontario government objecting to the proposed changes relating to farm severances, noting that granting municipalities the ability to split farms could hamper the growth of agricultural businesses such as livestock farming, fragment the agricultural land base, and risk inflating farmland prices due to new demand for land in traditionally farming-centric regions(26). Ultimately, the Ontario government decided not to proceed with the proposed lot severance regulation change but left the rest of Bill 97, including the MZO and municipal expansion proposals, intact.

Balancing Growth and Conservation – a Global Issue

Recent events in Ontario serve as an example of the delicate balance that must be achieved when considering both the protection of valuable natural resources and how municipalities will accommodate growth. However, this is not an issue unique to Ontario.

In June 2023, the State of Arizona implemented restrictions on home-building in the Phoenix area, currently one of the fastest-expanding municipal areas in the United States, in light of concerns over water supply based on groundwater projections over the next 100 years(27). The new restrictions will not affect projects that received permits prior to announcement of the policy but will prevent the construction of new homes that rely on groundwater supply, particularly in suburban areas(28). In a news conference, Arizona Governor Katie Hobbs stated that “this pause will not affect growth within any of our major cities”(29).

Maricopa County, which includes Phoenix and surrounding suburbs, draws more than half of its water supply from groundwater; given it can take thousands of years to replenish groundwater it is effectively a finite resource(28). On the subject of the role that water availability plays in future development, Director of the University of Arizona’s Water Resources Research Center Sharon Megdal noted that “we need to have water supplies in order to grow”(27).

Though it is not clear how Ontario’s growth story will ultimately evolve, increased housing supply and a stable food supply chain – including locally-produced food – will both play critical roles in supporting population growth for the long term. It is also true that, as a major contributor to Canada’s agricultural exports, Ontario’s farming sector will likely become increasingly important in the context of global food supply as the world’s population grows and climatic factors shift where crops can be growth around the globe. As a partner to Canadian farmers and agri-business operators for over a decade, Bonnefield has observed that Ontario’s farmers, along with their counterparts across the country, are resilient, adaptable, and growth minded. Ontario’s agriculture industry will play a major role in supporting the province’s growth, and access to farmland will remain an essential part of ensuring the sector’s success for years to come.

Bonnefield’s Perspective

Bonnefield is a proud, longstanding and supportive partner to Canadian farmers and agri-business operators. We prioritize “farmland for farming” and would like to see future generations of Canadian farmers have access to high quality, productive farmland. Farmland, and premium farmland in particular, is a valuable resource on which our future food production depends. For over a decade, Bonnefield’s farmland sale-leaseback offering has provided farm operators across the country with an alternative source of capital that ensures long-term access to the high-quality farmland that is essential for their operations, while also maintaining and enhancing the land that we invest in through agronomic best practices and strategic property improvements.

We also recognize that farmland represents the largest financial asset for many farm families and that selling land – whether to other farmers, long-term investors, or developers – allows operators to realize some of the long-term value appreciation of their land assets. This in turn provides farm operators with capital to help achieve important goals, such as transitioning toward retirement, or investing in other aspects of their businesses (e.g., equipment, technology, alternative parcels of land that improve operational efficiency).

It is our view that farmers should be able to manage and operate their businesses in a way that allows them to achieve their objectives, and that includes retaining the optionality to maximize the value of their lands by selling to the highest and best users of that land. With that in mind, the recent policy changes related to land-use planning in Ontario may make such decisions more complex for farmers by potentially expanding the competitive universe of parties looking to acquire prime farmland for a variety of uses, which will result in greater competition for farmland. Though this may be a positive for those already considering exiting the farming industry, it will also make it more difficult for young farmers to enter into the industry and for existing farmers to expand, and thus potentially increase the profitability of their businesses.

It is clear that Canada will require a significant increase in housing stock to meet current and future demands for housing. However, a balance must ultimately be achieved between the need for new housing and the need to preserve farmland – a scarce and valuable resource – for future generations. We acknowledge that this will be a significant challenge for policymakers over the years to come but believe that consideration should be given to:

Pursuing new housing through densification in existing urban areas across the country, and

Protecting our most valuable and productive farmland through rigorous and effective long-term zoning regulations.

The Ontario Housing Affordability Task Force’s 2022 report highlighted a need to make better use of land, noting that undeveloped land should be part of the solution “but isn’t nearly enough on its own”, and that “most of the solution must come from densification”(11). Additionally, the Task Force’s report stated that “environmentally sensitive areas must be protected, and farms provide food and food security. Relying too heavily on undeveloped land would whittle away too much of the already small share of land devoted to agriculture”(11). As a leading partner in Canadian agriculture, Bonnefield is aligned with this sentiment; it is our sincere hope that effective collaboration between policymakers and industry stakeholders will help to preserve as much as possible of one of Canada’s most valuable resources – the land that feeds us.

About Bonnefield Financial

Bonnefield is a leading Canadian farmland and agriculture investment manager, providing financing to progressive farmers and agricultural operators through land-lease and non-controlling equity solutions. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented operators to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long-term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.

Investors are increasingly realizing the value of private market and alternative assets in their portfolios for their diversification benefits and low correlation to traditional public market equity and fixed income products. The case for alternative investments was clearly highlighted throughout 2022 as public market asset valuations experienced volatile and, in many cases, negative performance.

Institutional and non-institutional investors alike saw their private market and alternative asset allocations account for a greater overall portion of their portfolios through 2022, both as a result of the relative decline in value from public markets (the “denominator effect”) as well as strong performance in select private market asset classes (“the numerator effect”).

However, recent market dynamics have brought two questions to the forefront for private market investors:

“How are my private market assets being valued?”, and

“Can I realize on these values by redeeming my existing positions?”

These topics are important considerations when evaluating the extraordinary variety of investable assets available to investors and are also topics that Bonnefield, one of Canada’s leading farmland and agriculture investment managers, regularly discusses with investors. Our team is keen on ensuring that all investors, irrespective of scale, fully understand and consider the importance of different valuation practices and liquidity features when selecting investments to meet their own investment requirements

Investing in Canadian Farmland – How can you Mark-to-Market?

Across private markets, fund managers use different valuation methodologies and practices to apply to their investment portfolios. Some use their own internal valuations while others rely on third parties. Some strike new values quarterly while others, every 12 months. It is important for potential investors to evaluate these methods and determine their comfort with, and suitability of, the approach with the asset and investment model.

Over its 14+ year history, Bonnefield has developed and refined our farmland valuation practices in a way to provide confidence to investors. We engage third-party, independent, accredited property appraisers to conduct thorough appraisals on our farmland properties, and those appraisals ultimately form the basis of the quarterly Net Asset Values (“NAVs”) of the funds.

Key Considerations

Arm’s-Length, Independent Appraisers

The use of third-party appraisers lends itself very naturally to farmland and we are fortunate in Canada to have a strong roster of qualified, independent professionals able to effectively value Bonnefield’s farmland properties across the country. The Appraisal Institute of Canada (“AIC”) is Canada’s leading real property valuation association and is a self-regulating organization that grants the Accredited Appraiser Canadian Institute (“AACI”) designation to qualified professionals who meet certain educational and experience requirements. These professionals must complete a series of examinations and continuing education requirements(1). As appraisers are held to a professional code of conduct by the AIC and are formally educated in the appropriate methodologies to derive property values, we are confident that the appraisal reports produced by AACI-accredited appraisers reflect the appraisers’ independent views of fair market value based on defined, objective analysis.

Fact-Based Analysis & Results

Professional appraisers rely primarily on quantifiable, observable data points to support their views of property values. Appraisal reports typically include a detailed analysis of relevant comparable property sale transactions that have occurred in the market, and that set of comparable sales transactions is refined based on geographic proximity, inherent land characteristics (e.g., soil types, crop types, topography, water access, drainage), and recency. Determining market values based on actual, tangible data ensures that appraisal values reflect current market conditions and do not consider speculative views as to where values may trend in the future.

Transparency

In private markets, information asymmetries can act as both a benefit and a risk. Bonnefield maintains a robust, proprietary internal database of farmland sale transaction activity across the country. This data set includes transaction dates, prices, and high-level property information that ensures our team is well-informed regarding historical observable farmland transactions. The database is updated on an ongoing basis. Having access to this information also helps to guide the initial stages of our investment process by enabling our team to quickly assess whether the proposed sale price for a potential farmland acquisition is reasonable in the context of the broader market. This database is also valuable when reviewing third-party valuation reports to ensure that no relevant transactions have been overlooked, which can occur in practice.

Timeliness of Data

Bonnefield strikes quarterly NAVs across its open-ended farmland funds and these values are informed by staggered appraisals across its properties. Bonnefield ensures each property is appraised at least once annually and can test its core regions and sub-strategies quarterly with this approach. This cadence matches the realities of the industry whereby a single growing season is unlikely to result in meaningful valuation changes within 12 months. However, to ensure timeliness of data, we continuously monitor comparable sales across the country to identify whether recent activity warrants additional appraisals throughout the year. It is our view that this level of rigour is appropriate for ensuring the most accurate reflection of value and ongoing pricing as possible, given the realities of a private, relatively illiquid market for farmland.

Liquidity Considerations for Investors in Private Markets

The discussion above outlines the approach that Bonnefield takes to valuing our Canadian farmland investment portfolios. The valuation approach is one of the key considerations when evaluating a private markets / real asset manager but, just as important is the question of how an investor can realize on value gains over time.

This question has been a particularly ‘hot topic’ given 2022 conditions, which saw private markets meaningfully outperform their public counterparts. Such a differential in performance can lead investors to request redemptions from their private markets fund holdings – a dynamic that was brought to light by reports of funds such as Blackstone’s REIT restricting redemptions in response to a surge in redemption requests. Closer to home, Canadian private mortgage lender Romspen also announced that it was freezing redemptions.

What actually drives these surges in redemption activity?

There is likely no single driver of increased redemption requests but in times of private market outperformance it is possible that investors are looking to realize value in anticipation of a value decline or rebalancing needs in other parts of their portfolio.

They may believe that values have not been adjusted on a timely basis and therefore want to redeem before the “correction” occurs. Or they could mistrust the value and want to realize on gains when possible. Both cases speak to the earlier points discussed with respect to the importance of appropriate valuation timing, transparency, and supporting data. Similarly, more institutional managers often manage their portfolio to pre-defined portfolio allocations and outperformance (or underperformance) in any one allocation can result in a shift away from their optimal mix.

Across Bonnefield’s open-ended farmland funds, we did not see heightened redemption requests through the end of 2022 despite strong performance of the assets. However, this is not unexpected given:

Canadian farmland is expected to outperform in times of high inflation; our investor base was not surprised to see the funds outpace other asset classes in the 2022 inflationary environment.

Farmland is a long-term, low volatility asset, and our investors have a long-term time horizon for their investments.

Our quarterly NAVs are based on third-party independent appraisals that use a comparable sales approach, thus drawing on actual comparable asset performance.

Our funds realize gains on an ongoing basis through regular portfolio management, most often in the form of sales of acreage back to our tenants or local farmers. This can serve as a market-test and enhance investor confidence in the ongoing valuation of the properties.

As Canada’s leading agriculture-focused investment manager, Bonnefield strives to be a strong steward of both the farmland properties that we manage, as well as capital invested by our limited partners. We are proud to be a source of long-term capital for farmers and agricultural operators, backed by investors who are committed to the long-term success of Canadian agriculture.

About Bonnefield Financial

Bonnefield is a leading Canadian farmland and agriculture investment manager, providing financing to progressive farmers and agricultural operators through land-lease and non-controlling equity solutions. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented operators to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long-term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.

Bonnefield has always been a strong supporter of Canadian agriculture. For over a decade we have worked with farmers across the country to grow their operations, transition to the next generation, or stabilize and strengthen their balance sheets through a flexible land-based capital solution. Over this time, we have heard from many others interested to understand how Bonnefield could also support their businesses beyond farmland. Not only does this represent a natural extension of our existing farmland investment activities, but it is also in keeping with our commitment to the future of Canadian agriculture to find a way to support these operators. For this reason, we are launching a new investment vehicle, the Bonnefield Integrated Agriculture Fund, with a mandate to invest in agri-businesses and on-farm infrastructure via non-controlling capital for leading operators.

When we think of food production in Canada, the focus is often on primary production, particularly crop and livestock farming, or on the manufacturing and sale of finished products such as baked goods, shelf-stable products, bottled beverages, packaged fresh and frozen produce, and other readily consumable items that are available at most food retailers. However, there are a number of integral steps between primary production and the sale of finished products to consumers. The journey that our food takes from field to plate is complex and, while each part of the agri-business value chain faces unique challenges, we believe that there is significant opportunity and need for investment and growth in this sector.

A Primer on Canada’s Agri-Business Value Chain

Food production begins with primary agriculture, which encompasses the core activities that are performed within the boundaries of farms, nurseries, or greenhouses(1). Primary agriculture can include growing and harvesting crops (e.g., grains, fruits, vegetables), dairy farming, raising livestock and poultry, and aquaculture.

After food leaves the farm, processors transform raw food inputs into products and by-products that are either finished and ready to consume (e.g., milk, meat, packaged fruit and vegetables) or are then used in further value-added processing to create other goods (e.g., oils, flours, extracted proteins). Most of the food that we eat must be processed in some way prior to consumption. To take a simple example: wheat must be grown, harvested, graded (inspected and assessed for quality), cleaned, dried, ground, packaged, and shipped before it can be used to make food products such as bread.

Storage and logistics also play a fundamental role through the entire process, ensuring that food products are held safely, available for use, and able to move efficiently on to the next buyer or consumer. Grain storage and elevators, terminals, warehouses, cold storage and transloading facilities, and third-party transport providers (including trucks and railways) are a few notable examples of additional services and infrastructure that are necessary for food products to ultimately reach end consumers. These functions are essential in ensuring that Canadian food products are able to reliably reach domestic and international end markets. Notably, Canada is a major exporter of food to countries around the world and is expected to play an increasingly major role as climate change continues to affect where food is produced around the world in the coming decades.

Toward the far end of the value chain lies food distribution and retailing, and the foodservice industry. Wholesalers, grocery stores, diversified retailers, convenience stores, specialty retailers, and restaurants represent the most frequent and consistent touchpoints that many Canadians have with the agri-business value chain.

Overview of the Canadian Agri-Business Value Chain

Food Production: A Canadian Economic Powerhouse

Canada’s agriculture and agri-food processing sector is a major driver of our country’s economy in terms of production value, job creation, and international trade. Canada’s most recent Census of Agriculture reported that there were nearly 190,000 farms across the country as of 2021 which collectively employed 241,500 individuals(2). Primary agriculture also generated approximately C$32 billion, or 1.6%, of Canada’s gross domestic product (GDP) for the year(2). The Census also reported that total farm cash receipts reached an astounding C$83.2 billion for the year, of which 57% (C$47.3 billion) was attributed to crops and 36% (C$30.0 billion) was attributed to livestock and livestock products, with the remaining portion comprised of direct payments(3).

Food and beverage processing was also a major source of production value and Canadian jobs in 2021, having generated C$33 billion, or 1.7%, of Canada’s GDP for the year and employing over 300,000 individuals(2). Food and beverage processing also represented the single largest manufacturing industry in Canada in 2021, accounting for nearly 18% of all manufacturing-related GDP for the year(2). Interestingly, approximately 70% of all processed food and beverage products sold in Canada were manufactured by domestic producers in 2021, with half of the imported products having been manufactured in the U.S. and the remaining imported goods sourced from other countries around the world.

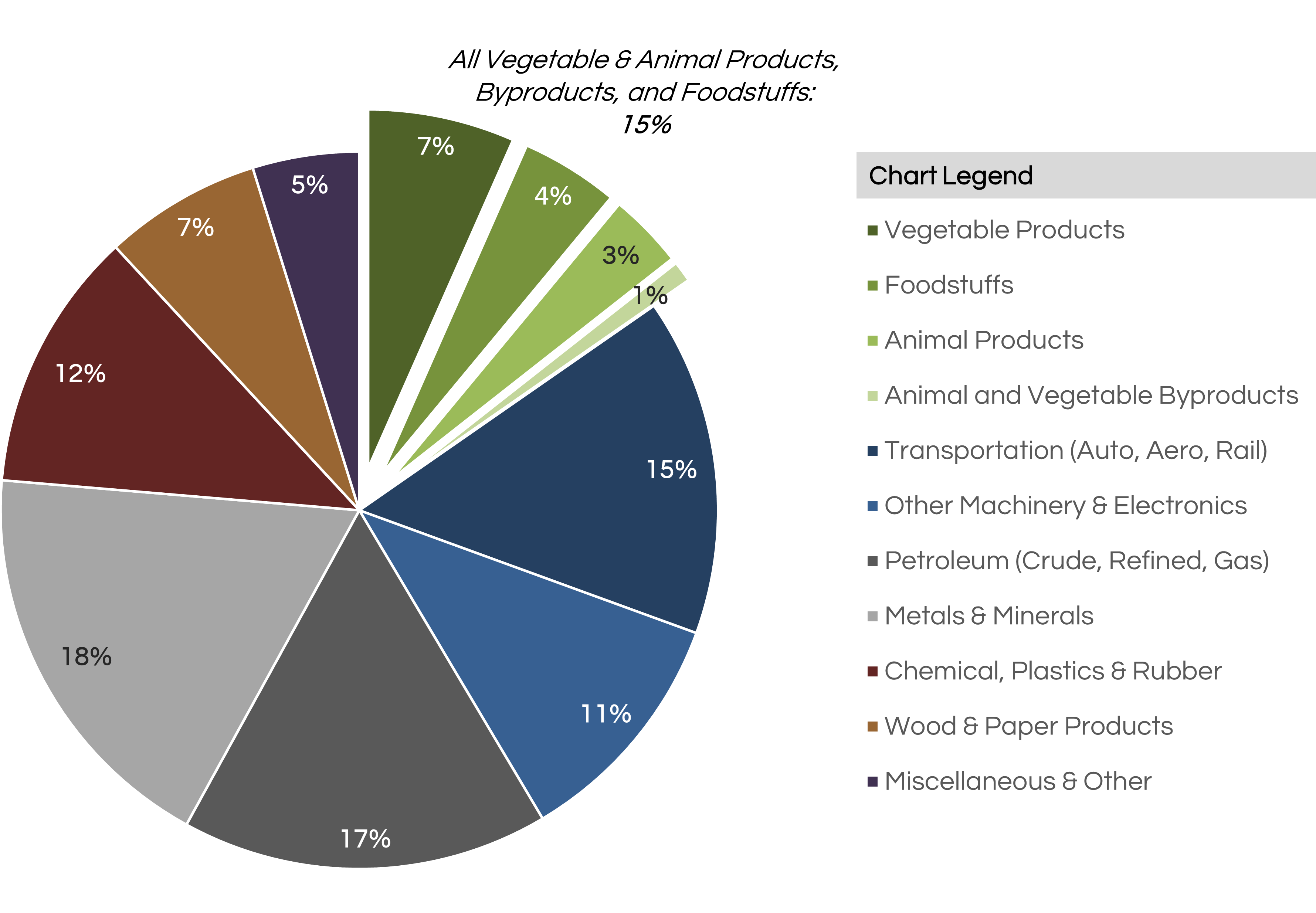

The economic importance of Canadian farming and food processing is further underscored when we look more closely at international trade. In 2020, the total trade value of all of Canada’s exports reached C$370.8 billion dollars, of which C$56.9 billion or 15.3% was attributed to collectively to vegetable products (C$24.5 billion / 6.6%), foodstuffs (16.3 billion / 4.4%), animal products including meat, cheese, eggs, and milk (C$12.5 billion / 3.4%), and animal and vegetable by-products including oils (C$3.5 billon / 0.9%).

As seen above, the aggregate trade value of Canadian food exports rivalled the value of exports from several other natural resource sectors including oil & gas and the extraction of minerals and metals, as well as the export of automobiles, airplanes, and locomotive equipment.

The strength of Canada’s agri-business sector relies on a functional, efficient value chain that extends from primary food production through to distribution, whether to domestic or international end markets. As discussed in Bonnefield’s most recent White Paper exploring the effects of climate change on global agriculture, we believe that Canadian food production will prove to be increasingly important over the near- to mid-term as the effects of climate change begin to affect food production elsewhere in the world.

As Canadian production of certain food products, such as crops, fruit, and vegetables stands to increase due to favourable shifts in climactic conditions over the coming decades, we believe that major investment in increasing processing capacity and technology, along with storage and transportation infrastructure, will also be necessary as we look to the future.

A Need for Capital…

According to a 2018 study conducted by Canada’s Economic Strategy Tables discussing the state and goals of the country’s agri-food sector, Canada had 11,499 food and beverage processing establishments in 2017 of which 94.4% were small operations with fewer than 99 employees(5). Additionally, capital investment in the food processing industry, particularly machinery and equipment, as a percentage of sales dwindled from 2.3% in 1998 to just 1.2% in 2016, and R&D expenditures in the Canadian agri-food sector as a percentage of sales fell by 24% between 2008 and 2016(5). This suggests that there has been a sustained under-investment in Canada’s food and beverage processing industry that needs to be addressed.

Finally, the report indicates that the investments that have been made in food processing innovation were fragmented across educational institutions, food technology centres, research centres and locally focused incubators(5). While these organizations play an essential role in terms of research, their scope in being able to achieve scaled commercialization is intentionally limited(5).

Just as we saw a need for alternative sources of financing in the farming industry over a decade ago, Bonnefield recognizes that Canadian agri-businesses more broadly are also limited in their access to sources of capital. These companies are often operating in manufacturing-related sectors that are capital-intensive. They require machinery, facilities, and technology – any or all of which require significant funds to acquire and implement – to compete successfully and achieve growth. Traditional debt-lending provides meaningful support to these operators but complementary, industry-specific, alternative forms of financing are lacking in the Canadian market.

… and an Attractive Investment Thesis

For those looking to gain exposure to the attractive investment attributes of agriculture, investment in Canadian agri-businesses offers an appealing option. Not only is there demand for increased investment into the sector, but Canada specifically offers unique and attractive dynamics.

Diversification: In terms of crop farming, Canada benefits from a geographic landscape, soil types, and climactic conditions across the country that result in growing conditions that are hospitable for different crop types on a regional and localized basis. For example, farmers in New Brunswick have access to land that can successfully produce potatoes, whereas farmers in the Prairies have farmland and weather conditions that better suited to row crop farming. The same is true of other agricultural products, such as dairy, wild-caught and farmed seafood, and livestock. Given the diversity of agricultural production across the country, there are many unique opportunities for businesses further along the value chain to add value through processing, packaging, storage, and transportation of Canadian farmed products. We believe that this inherent diversification gives rise to a myriad of opportunities for investors looking to deploy capital in the space.

Demand for Canadian Products: Canada’s reputation for outstanding food product safety and quality is world-renowned(5). An increasing consumer focus on food nutrition and safety, combined with a growing global population and a changing climate-driven shift in where the world’s food will be produced in the future provides a strong rationale to support the thesis that demand for Canadian-made food products will likely continue to grow over the coming decades. To meet this demand, the entire value chain – from primary producers to processors and distributors – will need to grow. Naturally, we anticipate that this will create compelling opportunities to invest in Canada’s agri-business sector, particularly around achieving scale and innovating for the future.

Supportive Regulatory Environment: The Canadian agri-business sector also benefits from a regulatory environment that seeks not only to support existing industry participants, but to grow the industry over the long-term. One example of this is the Canadian Agricultural Partnership (“CAP”) – a five-year joint investment program through which Canadian federal, provincial, and territorial governments will invest C$3 billion between 2018 and 2023 to strengthen and growth the agriculture and agri-food sector(6). The CAP encompasses initiatives, program, and funding geared toward growing trade and expanding markets, innovation and sustainable growth, and supporting diversity(6). Though this is one of many examples of Canada’s long-term practice of providing governmental support for the agriculture and agri-business industry, it still stands that the sector has seen a lack of investment in recent decades.

Bonnefield’s Role

As Canada’s leading provider of supportive, flexible sale-leaseback financing solutions for Canadian farmers, Bonnefield has heard time and again from our farmers and network of business partners that there is a distinct need for investment in the Canadian agri-business value chain beyond the farm gate. The launch of the Bonnefield Integrated Agriculture Fund is a major milestone for our firm that represents an opportunity to further expand our presence as a partner in agriculture by supporting leading Canadian agri-business operators. We are excited about this evolution and look forward to contributing to the ongoing strengthening and growth of Canada’s agricultural industry.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.