Those who follow the agricultural industry will be aware of the increasing attention that agriculture technology (AgTech) firms are receiving, and with it, significant investment dollars. In fact, one of Canada’s largest institutional investors, the Ontario Teachers’ Pension Plan (OTPP) recently made its first AgTech investment through its venture capital arm, Teachers’ Innovation Platform. With the spotlight on the AgTech industry, we wanted to review the role that technology has played in agriculture and explore how ongoing innovation can drive industry performance through the lens of a farmland owner / investor.

Technology in Agriculture: A Driver of Productivity & Farmland Values

Innovation and technological advancements in agriculture have been around for as long as farming itself. The search for increased efficiency to meet growing consumer demands is not going away and significant technological advancements have been made in the agriculture industry over the past several decades. Today, technologies such as GPS Guidance for farming equipment and Site-Specific Crop Management practices allow farmers to be more precise and efficient in crop production. As a farmland owner, this raises a key question: how do technological advancements affect producer income and subsequently, farmland values?

For a conventional crop producer, farm income is a function of underlying commodity prices, expected crop yields, and the cost of crop production. Commodity prices are determined by the global market and, while producers can use certain marketing strategies to help reduce risk, individual producers cannot ultimately influence commodity prices. As such, farm operators looking to improve productivity, and thus profitability, can be better served by finding ways to boost crop yields and lower production costs to increase income.

Since farm incomes are a key driver of farmland value, the result of sustainable increases in overall farm profitability can be seen through appreciation of farmland values, making new advancement in AgTech interesting for not only the farm operator but the farmland investor as well.

Examples of AgTech Areas of Focus

Plant Breeding

While longer growing seasons resulting from climate change certainly play a role in increasing crop yields in certain geographies, advances in agricultural technology are also widely acknowledged as being a major driver of improved yields. Notably, there have been significant advancements in plant science and breeding over the past 30 years. Varieties of certain key crops, such as corn, soybeans, and canola can be engineered to mature over a specific number of growing days to accommodate local growing conditions and allow farmers to plan for crop maturity at desired times, or to be more resilient against certain diseases. This allows farmers to select and seed optimal plant varieties that are best suited to their location and the characteristics of their land.

Precision Agriculture

Precision agriculture (also referred to as Site Specific Crop Management) uses aerial and satellite imagery, weather data, and crop health indicators to enable farmers to be more exact in the planting of seeds and the application of fertilizer. For example, variable-rate fertilizer application allows producers to apply the ideal amount of fertilizer to different regions of a single field to maximize crop health and avoid unnecessary overuse of fertilizer. Beyond increasing crop yields, this technology also has considerable benefits from an environmental perspective as it reduces the overall amount of fertilizer required thus preserving supply and limiting unnecessary run-off. Other technologies, such as GPS guidance, have allowed for more accurate planting of crops and fewer wasted acres.

Larger, More Efficient Machinery

Technological advancements have also created significant cost savings in agriculture, and farming operations are larger and more efficient than ever. This is made possible by new technologies such as the large machines that allow producers to plant, fertilize, and harvest greater acreage in less time. Today, large tractors with planting implements spanning over 60 feet in width can cover over 300 acres in a single day, whereas the smaller 15-foot no-till drills of the past would have taken more than four days to cover the same amount of land.

What This Means for Farmland Values

Technological advancements have helped producers to increase yields, reduce costs and have ultimately had a positive impact on farm income and farmland values. As noted in our Q1 newsletter, there has been much excitement in the Canadian farmland market in the first half of 2021, attributable to commodity prices rising to multi-year highs, low transactional activity in 2020, and the prolonged low interest rate environment. However, these factors are cyclical and can shift in a relatively short period of time. In contrast, activities by farm operators and the agriculture sector as a whole, to develop and implement new technologies, increase yields, manage costs, and reduce their environmental footprints are something we believe will support the ongoing capital appreciation of Canadian farmland.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

We are often asked what sets Bonnefield apart as a leading Canadian farmland manager. While there are many qualities that come to mind (our strong 10+ year track record, institutional quality reporting and administration, and our sale-leaseback model that attracts leading farm partners, just to name a few), diversification is one of the most obvious.

Geographic diversification has been a central theme in Bonnefield’s investment thesis since the firm’s inception over a decade ago. As Canada’s leading farmland investment manager, we invest in more Canadian provinces than any other Canadian agriculture-focused asset manager. We apply a granular approach to diversification, investing in over 30 unique growing regions across the country, and ensuring portfolio diversification across multiple climatic regions, crop types and tenant relationships.

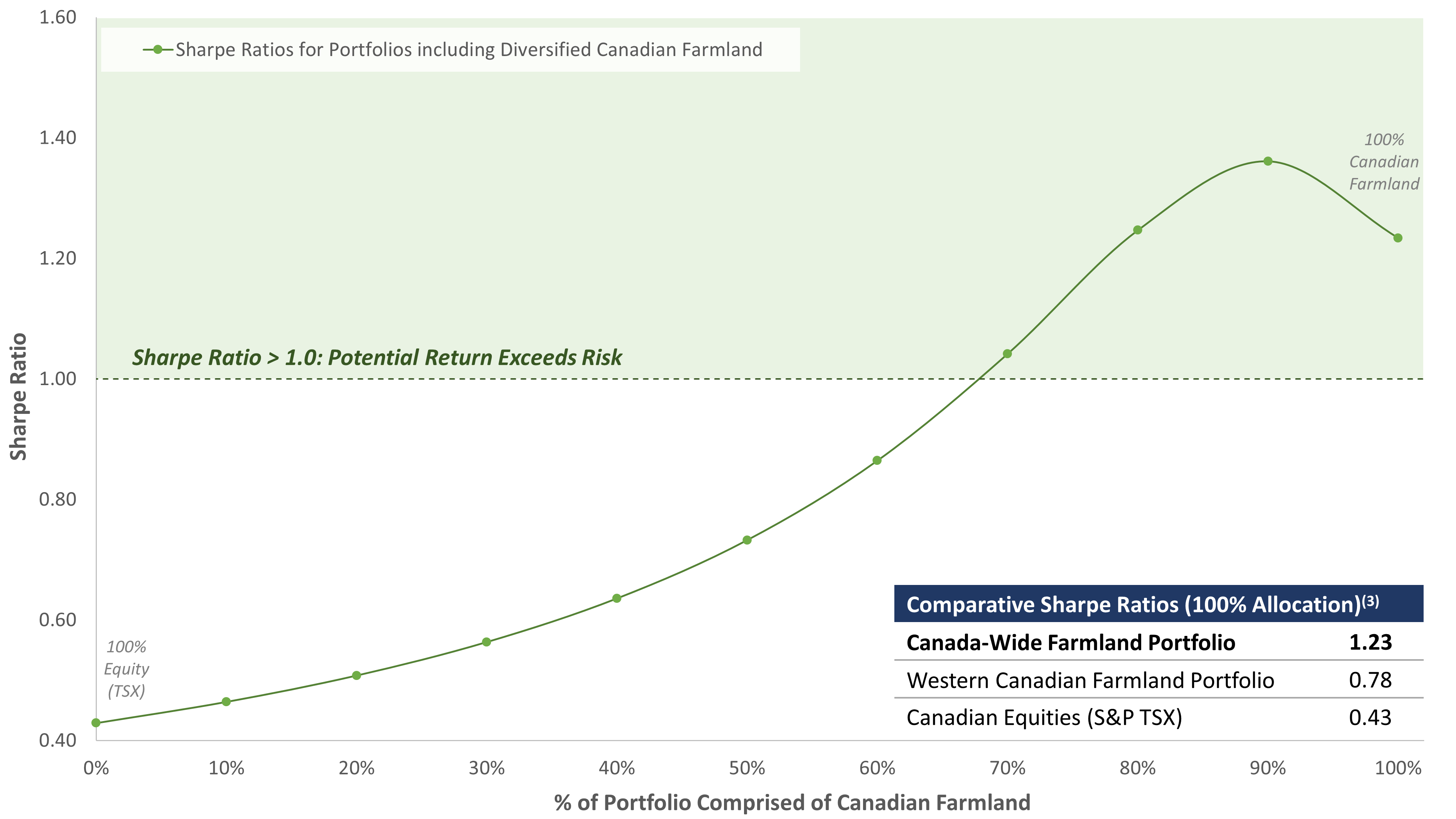

Assessing Risk & Return: Sharpe Ratio Analysis

To illustrate the value of diversification in an investment portfolio, we conducted a Sharpe ratio analysis(1) using historical Canadian farmland values between 1985-2019. This type of analysis is a staple of portfolio management theory and a relative measure of the trade-off between risk and return. A higher Sharpe ratio typically suggests a higher potential return per unit of risk taken on and therefore, many investors focus on improving / maximizing the Sharpe ratio of their portfolios.

Risk-Return Profile: Diversified Canadian Farmland in a Portfolio (Sharpe Ratio Analysis)(2)

The first takeaway from this analysis is the positive impact on the Sharpe Ratio as a result of increasing the allocation to Canadian farmland (regardless of its diversification) as opposed to holding only publicly traded equity. With its historically stable return profile, Canadian farmland reduces the volatility of returns and, therefore, improves the Sharpe ratio.

The second takeaway is the relative benefit of holding a portfolio with greater diversification amongst its farmland holdings. As seen in the chart above, portfolios consisting of farmland diversified across most provinces in Canada (Bonnefield currently invests in BC, AB, SK, MB, ON, NB, and NS) demonstrate higher Sharpe ratios, indicative of a favourable risk‐return trade-off, compared to those with farmland limited to only the prairie provinces. This illustrates the relative benefits of maximizing potential diversification within the farmland portfolio.

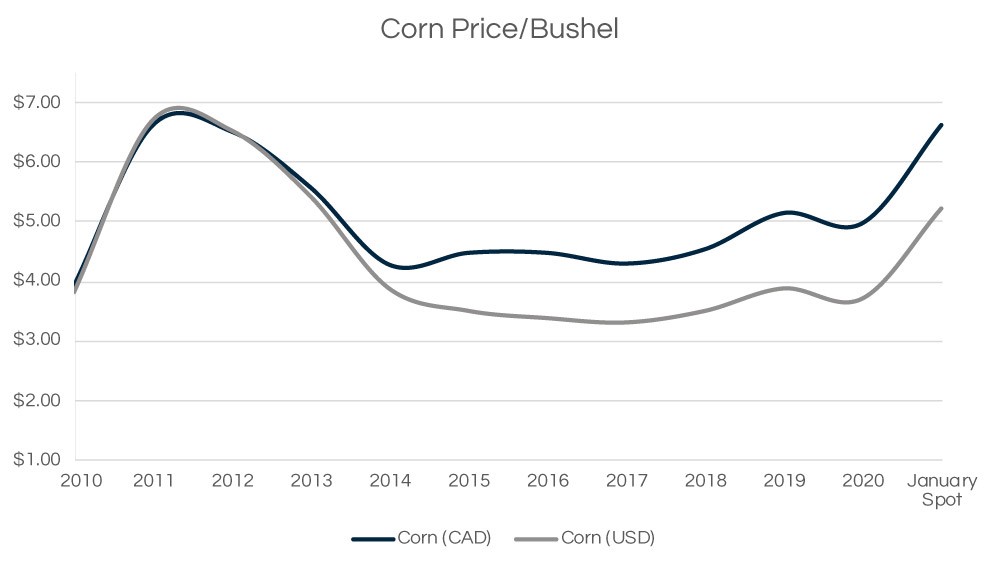

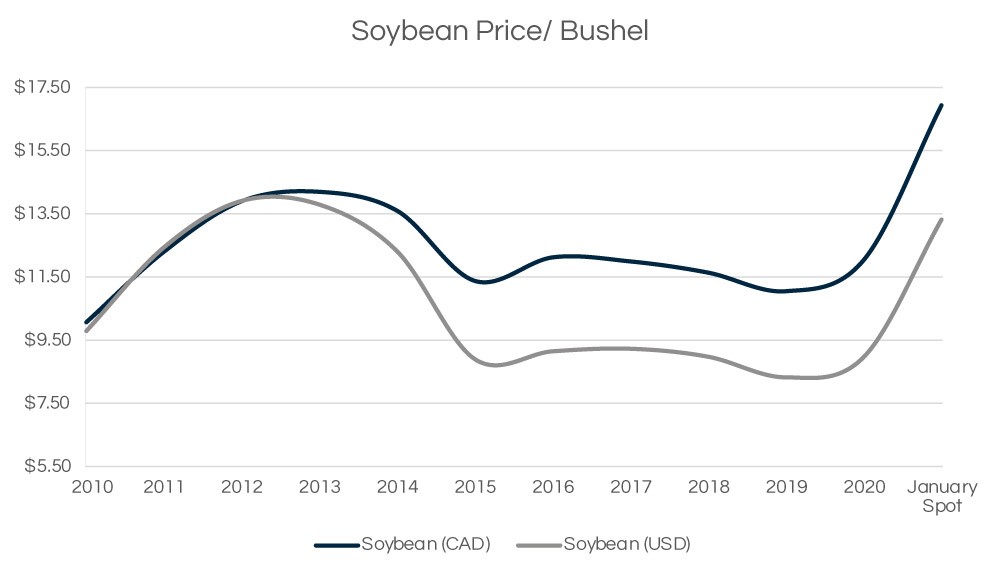

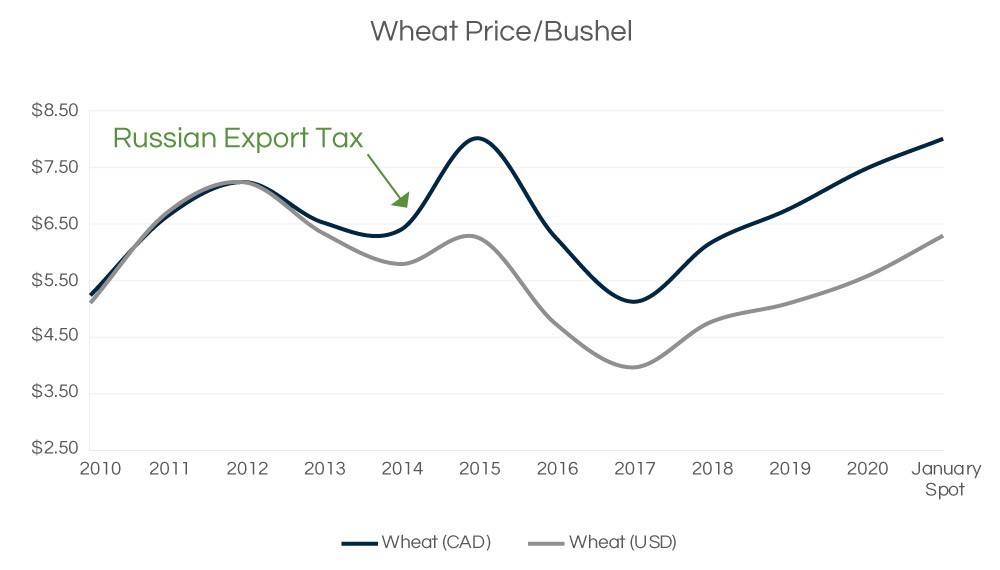

As noted in our Q1 2020 Newsletter, the Canadian agricultural community has been optimistic since the beginning of 2021 given:

The backdrop of increased feed demand from China;

The reduced crop supply from Brazil and Argentina; and

The Russian export tax on wheat.

Combined with a prolonged period of low interest rates, relatively low transactional activity for Canadian farmland in 2020, and the current multi-year high commodity prices for key crops, we continue to believe that Canadian farmland values are poised for an exciting period of strong growth.

As investors explore the benefits of Canadian farmland within their investment portfolios, we encourage them to consider the relative value of exposure to a well-diversified farmland portfolio to minimize volatility and maximize your potential risk-adjusted returns.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

(1) Sharpe ratios represent a relative measure potential returns compared to potential risk of an investment, and are calculated by dividing i) the excess return above a selected risk-free rate (i.e., average historical rate of return for an asset/investment less a risk-free rate such as the prevailing rate for a Government or Treasury-issued instrument) by ii) the standard deviation of those historical returns.

(2) Analysis contemplates hypothetical portfolios balanced between i) Canadian equities (S&P TSX index) and ii) Statistics Canada farmland values (weighted equally between selected provinces; Bonnefield’s investment provinces include BC, AB, SK, MB, ON, NS, and NB), between 1985 and 2019.

(3) Noted Sharpe ratios assume 100% allocation of a hypothetical portfolio to each of i) Canadian farmland in Bonnefield’s investment provinces, ii) Canadian farmland in AB/SK/MB only, and iii) Canadian equities (S&P TSX index).

Over the past decade, we have seen increased interest among the investment community in agriculture and farmland as an asset class. Not only are large, sophisticated, institutional investors across the globe evaluating (or already invest in) farmland and agricultural investments, so too, are increasing numbers of non-institutional investors.

Click here to read an article by Bonnefield’s Andrea Gruza that explores how farmland investments provide investors with a diversifying asset with strong ESG characteristics, climate change hedging capabilities and potential to support a move towards a net zero investment portfolio.

(Original article published in the spring 2021 edition of Radius European Investment Journal.)

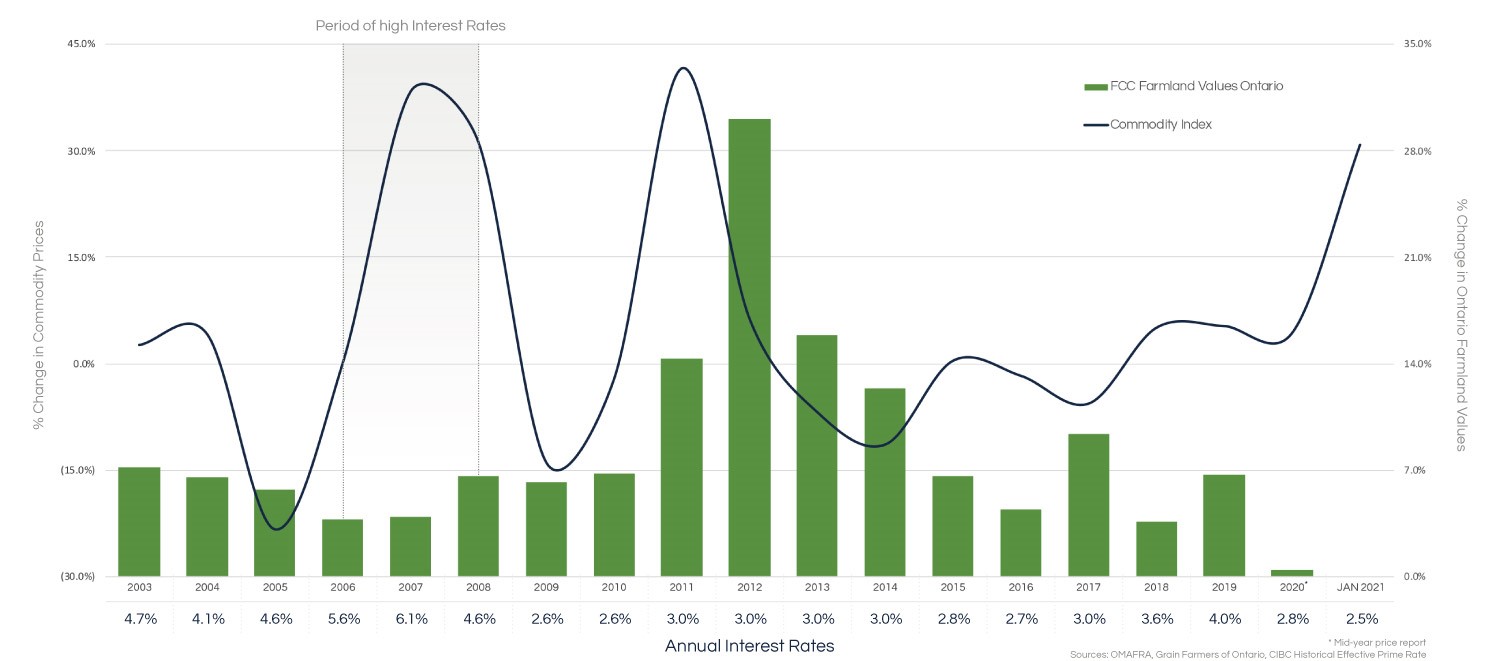

The mood in much of the Canadian agricultural community has been positive lately. Following several years of depressed agricultural commodity prices, there is a significant rebound in prices across multiple commodities. The last time we saw similar commodity price growth, combined with low interest rates was in 2011 which marked the beginning of several years of double digit increases in farmland values. While there is no guarantee that we will have the same outcome, the signs are very encouraging.

1. Increased Demand from China

The catalyst for this rebound has been a massive increase from China for feed, as it rebuilds its hog herds following the devastating impacts of the 2018 swine flu that resulted in a ~60% reduction of the country’s breeding sows by the second half of 2019 (1). We expect that the increase in demand from China should be longer lasting as it will likely take two to three years to rebuild the pig herds back to pre swine flu levels.

2. Severe Drought in South America

A severe drought in South America since last October drastically reduced supply from Brazil and Argentina – two major corn and soybean producers. While this offers short-term support to pricing, recent rains in the region should provide positive conditions for the current harvest.

3. Russian Export Tax on Wheat

Finally, prices are also seeing an impact from a recently announced export tax that Russia placed on its wheat producers in an attempt to reign in recent domestic food price inflation resulting from COVID-19. In 2015, this had a major impact on global wheat supply. We expect a similar impact this year with wheat prices increasing materially.

Sources: OMAFRA, Grain Farmers of Ontario

Commodity Price Impact on Farmland Values

Given the magnitude of recent commodity price increases we took a look back to see what effect commodity prices have had on farmland values historically. Two notable characteristics emerge from this analysis.

1. Significant upside potential for farmland values resulting from a combination of high commodity prices and low borrowing costs.

This creates a favourable environment whereby farm profitability increases, leaving farm operators with more cash in their pockets. The combination of greater cash on hand and low borrowing costs facilitates an increase in farmland acquisitions. Having this combination of factors is important because, as we saw in 2007, an increase in commodity prices against the backdrop of high borrowing costs, did not see meaningful farmland value increases.

2. Farmland values have had historical downside protection through several years of significant commodity price decreases.

Not only have farmland values failed to track the declines in commodity pricing, they have actually continued to increase in value (albeit at a slower rate in years of significant commodity price declines.) This trend can be attributed to the favourable supply and demand dynamics that exist due to a limited supply of global arable farmland with an increasing demand for food. From 1961 to 2016 there was a 48% decline in hectares of arable land per person (2). This is attributable both to a growing population as well as a decline in total arable land from desertification and urbanization.

It is evident, based on historical analysis, that commodity prices can influence farmland values through enhanced farm profitability. Based on our experience of the last two decades, that influence is far more significant on the upside than it is on the downside.

What This Means For Farmland Values

While there is always potential for unforeseen events to arise, a review of current market conditions provides support for a positive outlook on farm prices. The combination of increasing commodity prices and low borrowing costs shows the potential for a return to farmland valuations reminiscent of the early 2010’s.

A Note on the Analysis

We focused our analysis on Ontario using the three main cash crops grown in the province: wheat, soybeans, and corn. According to data from the Ontario Ministry of Agriculture, Food and Rural Affairs (“OMAFRA”), these three crops represent roughly 71% of the total cropland in Ontario based on seeded acres which makes this a meaningful, albeit simplifying, analysis for evaluating general trends in the province. In addition to commodity prices, we have also included the prime rate as a proxy for farmers’ borrowing costs, as this also has a significant influence on land values. The graph above illustrates the annual percentage change in commodity prices and Ontario farmland values against the prime rate. To capture historical commodity prices, we used a hypothetical commodity price index comprised of 40% soybeans, 40% corn and 20% wheat. This is representative of a typical five-year rotation for an Ontario farmer of two years planted to corn, two years planted to soybeans and one year to wheat.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

Bonnefield’s Vice President of Capital Markets Andrea Gruza joined host Robert Arnason on the Between the Rows podcast recently to discuss ESG Investing and its relevance for Canada’s agricultural sector.

“ESG investing isn’t necessarily a widely agreed-upon term and the definitions and parameters around ESG in the investing community really are evolving. It stands for environmental, social and governance factors. The term certainly has become pretty widely recognized and adopted across multiple industries over the last few years, not just within finance, and you’re hearing [it] from the majority of large sophisticated investors across the globe.

“I think everybody’s situation is unique and I can’t speak [for] all farmers across the country, but I don’t think ESG is [just] a trend. I can imagine the terminology around ESG evolving and the set of considerations for each industry changing over time as it better reflects what’s happening in the world around us. I think that as we learn more, we’re more aware of what things we should be thinking about when we evaluate how a business is performing.

Listen to the podcast and full interview below, or by clicking here.

Note: This is the final article in an eight-part series published by GAI News that examines eight existing trends set to alter the structure of our global food system. Be sure to read the first seven articles here: Part I , Part II, Part III , Part IV , Part V , Part VI and Part VII.

“Economic growth won’t feed a growing population living on this finite planet.”– Phil Harding

Concerns about population growth have circulated through discourse since ancient times. Philosophers, such as Plato and Aristotle, questioned the sizes of their respective communities and their capacity to nourish additional people when the world had a population of about 162 million [i]. Writers from ancient Carthage had dwelled on population growth when global numbers had reached 200 million people, who were noted as “burdensome to the world which can hardly support us”. As we approach a global population that is fifty times larger than in Plato’s time, the same concerns come to light, albeit with different information.

Productivity improvements have typically remained one step ahead of food demand, allowing the world’s population to grow geometrically over the past two hundred years. Although the population continues to grow, crop yield productivity improvements have slowed considerably in the past several decades[ii].

While the preceding seven articles of our ‘Agriculture in a Changing Climate and Society’ series focus on secular trends affecting the supply side of the global agri-food system, this final piece delves into the demand side. A multitude of evidence points to a singular fact: nutritional demand is increasing rapidly on a global basis[iii]. Some experts question the world’s collective ability to nourish this demand in the long term[iv], while others speculate that new technologies will need to be developed and implemented in order to address the supply/demand imbalance. The World Resource Institute (WRI) indicates that while fulfilling nutrient requirements for an additional 2.4 billion people in the next thirty years is achievable, the global agri-food system will have to undergo significant changes in order to adapt[v].

As external factors, such as urbanization, water scarcity and pollinator loss, are set to reduce global food supply[vi], the earth’s population is projected to continue increasing for the next century[vii]. Sub-Saharan Africa is set to foster most of the world’s population growth, an area that is likely to become less suitable for crop production over the next century. In addition to increasing populations, a growing middle class will naturally continue to increase the global appetite for meat, dairy, and high-value fruit crops. These products are characterized by high production and overhead costs compared to other commodities of similar nutrient profiles. While this consumption shift is positive from the perspective of social mobility and will likely foster a period of robust demand growth for farmers in the short-medium term, the increased demand will come at cost to the environment.

Some estimate that we will have to increase arable land by 593 million hectares (more than twenty-four times the size of the United Kingdom) between 2010 and 2050 in order to bridge the gap needed to meet increasing food demands[viii]. The greatest concern lies in our collective food security in conjunction with global environmental sustainability. The socio-ecological trade-offs that arise from developing forested land lends itself to notions that our arable capacity is reaching its peak.

Food Spending and Disposable Income

Spending on food in the United States, as a percentage of disposable personal income, has been sitting near its historic low since 2004. This does not come as a surprise, but as a paradox, as calories consumed per capita in the U.S. reached the all-time high of 3,828 per day in 2005[ix].

Figure 1: Normalized food expenditures by final purchasers and users[x].

Source: USDA, 2019

Food cost compared to relative wealth is historically low throughout the world, largely due to commercialization of value-chains, historical productivity growth, and national subsidies. While consumers in developed countries are currently offered nourishment at relatively affordable prices compared to their historical income levels, these prices generally do not address the ecological externalities involved in producing the food[xi]. As such, a trend reversal is forecasted to begin in the next twenty years for net food expenditure, predicated on a declining basis of scarce resources, transitioning food demand patterns and a need to account for the environmental effects of food production.

The Malthusian Theory: Cropland Per Capita

Most significant, agricultural producers are losing cropland per capita[xii]. A typical Western diet requires about 1.2 acres of cropland per year to supply the types of calories to which we are accustomed. Emerging economies are now consuming similar diets to those of the West with more meat and dairy. This is creating a critical point of increased demand for energy intensive food products. Many areas of the world, namely Asia and Africa, will not have the arable land to produce nearly enough food to nourish its population. Figure 2 depicts each region’s cropland per capita.

Figure 2: Acres of Cropland Per Person, 2016

Source: History Database of the Global Environment (HYDE)

If every person had the appetite of an average individual in the United States at the current level of production, we would need to convert every acre of forest into farmland and would still be short of calories by about 38 percent[xiii]. With current Western food consumption, a diet that is becoming normalized by the world’s middle class, only a select few countries have the capacity to domestically produce more calories than they consume. The burden of production will be left to a handful of agricultural exporters with enough productive cropland to contribute to the global food stores, such as Canada and Australia. Admittedly, the Malthusian model of food supply versus cultivated land does not offer full explanatory power for the planet’s carrying capacity. It does, however, paint a general picture of the planet’s capacity to nourish different appetites at current technological levels.

Calories versus Nutrients

In assessing the issues surrounding global food demand, a distinction should be made between calories and nutrient-requirements. While about 800 million people globally are suffering from a means-based caloric deficit[xiv], over 2 billion do not have regular access to safe, nutritious, sufficient food[xv]. The developing world will continue to struggle with food accessibility as its population grows. Further, crop nutrient capacity in equatorial regions especially, is incredibly sensitive to rainfall variability and spells of extreme heat.

The developed-world’s farming system, which will likely provide the nourishment for most of the world’s growing population, is largely based on maximizing caloric production rather than nutrient density and diversity. This model has perpetuated throughout agricultural economies, as farmers are incentivized to maximize their yields in response to historic consumer and government interests in driving down food costs. Farmers act as rational participants, naturally responding to the markets they supply.

The developed world’s agricultural system is still incentivized with the same family of subsidies that were legislated at the dawn of the third agricultural revolution. In North America and Europe these subsidies typically offer support for a handful of crops with high caloric density such as feed-grains and oilseeds.

While global needs, production methods, and resource constraints continue to change, the policies surrounding the food system have remained largely unchanged since their inception. National subsidy programs are frequently reciprocated by similar or equivalent programs in neighbouring countries, leading to antiquated and sticky legislative movement across international value chains. Re-orienting farmer incentives from caloric density to nutrient diversity could be a fundamental step towards solving this issue by producing foods which meet the needs of a growing consumer base.

Solutions, Steps, and Goals

While the difficulties in feeding a growing population are considerable, there remains optimism that it can be achieved. There are 10 steps that would help us to address the challenges related to nourishing the food demands of a growing population. Each topic is complex, worthy of its own article, and many have been listed by the World Resource Institute as keys to “feeding the 10 billion”.

Food Waste Mitigation: Evidence indicates that the most effective mechanisms for supplying accessible and nutritious foods exists in reducing food waste rather than growing greater volumes of crops per acre. In the developing world, most food waste occurs at the production and storage levels, while in the developed world a staggering amount of food is lost at the consumption and market levels.

Investment in Aquaculture & Developing Sustainable Fisheries: Improved fish farming technologies including new genetics, infrastructure, and algae-based feeds have increased the competitiveness and investment merits of the aquaculture industry. Preservation of current fishery stock, alongside sustainable farming methods, will be the foundation from which we can offer omega-3 fatty acids in the future.

Climate-Controlled Agriculture: With so much emphasis placed in farmland per capita and the notion of declining scarce land assets, climate-controlled agriculture is consistently climbing towards profitability, and therefore viability, on a large, commercial scale. Investing in low-cost options such as warehouse conversion may prove to be the next frontier of effectively nourishing urban populations. With this being said, 95 percent of our food, even in the developed world, comes from farmland.

Improved Technology & Genetics: While crop-yield productivity growth has been slow compared to green revolution levels, new advances in crop genetics and molecular biology are remarkably promising. Further public and private investment in crop breeding, biologicals, and AI technology could make all the difference in feeding the next 2 billion people.

Enhanced Water Management: Water depletion in groundwater systems continues to be one of the most alarming aspects of modern agriculture. We will eventually have to shift to a process where crops are irrigated only through sustainable water sources, such as rain-fed reservoirs, rivers, and/or snowmelts. That shift should begin before aquifers are fully depleted.

Soil Health Preservation: Some scientists estimate that we are losing up to 1 percent of topsoil each year, with nutrient availability degrading as well. Nearly two-thirds of this degradation is derived from deforestation and overgrazing. Incorporating techniques such as no-till agriculture, rotational grazing, drill seeding, and certain organic production methods could significantly reduce the rate of soil loss.

Sequester Carbon in Soils: What benefits soil health may also create the opportunity to sequester additional carbon. Maximizing soil organic matter levels offers a multitude of effects, such as enhancing yields, sequestering more carbon, diminishing the required nutrients amendments, and enhancing ecosystem diversity. This can be achieved through the use of cover crops and healthier rotations, as well as no-till and conservational tillage methods.

Shift Diets Globally: While a sensitive argument in agricultural circles, the fact remains that reducing ruminant (beef and lamb) consumption would reduce the number of calories and land needed to produce that food-type by over ten times. If global diets slowly shifted towards plant-based proteins and nutrient-dense fruit/vegetable products, total stress on the environment would reduce. In addition, many farmers have the opportunity to improve pasture productivity with enhanced fertilizers and regenerative grazing techniques, which could increase the output of meat and reduce emissions.

Reforest Inefficient Lands: The second greatest contributor to carbon emissions is land deforestation, particularly in equatorial regions. Investing in direct efforts to bring these fallowed lands back to productive capacity or re-foresting the lands would promote carbon sequestration and a multitude of ecosystem services. Large food companies may also commit to plant trees and sourcing products from tropical deforestation-free value chains.

Re-orient Legislation: It may be time for consumers to take the burden of paying the ‘total price’ for food and water resources, which includes the cost of depletion and the externalities involved in using the resource. Further, subsidies and farm support should slowly start to shift towards food types that dovetail with the nutritional needs of our growing population.

Ultimately, addressing challenges pertaining to population growth and its nourishment will require active collaboration between businesses, policy makers, and consumers. Resources must be used more efficiently, and innovation will need to be spurred by public and private support. The above 10 points are topics that will exist throughout this century and likely beyond it. Many solutions to the nourishment issue are also investable opportunities, underpinned by global demographic trends. Those who have the opportunity to allocate capital also bear the responsibility to deploy their resources towards environmentally resilient strategies and regions. With investors in all asset classes assessing how they can limit their exposure to the effects of global warming, there are few industries more intertwined with climate change than agriculture. The effects of climate change are relevant to every aspect of the global food system. The long-term issues that affect the world’s agricultural output become opportunities to invest, thereby creating value for investors and society.

Note: this article first appeared in Global AgInvesting on November 15, 2019 globalaginvesting.com. This is the seventh article of an eight-part series published by GAI News that will examine how the global food system is set to be altered by eight existing trends. Each month a new installment will be released. Click the following links to read the first six installments: Part I , Part II, Part III , Part IV , Part V and Part VI.

Written by: Jeremy Stroud, Bonnefield, Agricultural Investment Analyst

Institutional investors are allocating capital with greater longevity in mind than ever.(1) With US$84 trillion of institutional assets under management in the 34 Organization for Economic Co-operation and Development (OECD) countries and a lengthening timescale of liabilities, investors are increasingly considering factors that were previously overlooked.(2) As the Canada Pension Plan Investment Board (CPPIB) stated in its last annual report, its current strategy involves “investing in quarter centuries, not quarters” by addressing factors that are projected to pose a threat to return generation and capital preservation several decades in the future.(3) While crop pollination and insect extinction may not be issues that rise to the top of an investor’s mind, they are fundamental to many economic activities in the long term.(4) One-third of the world’s food supply is reliant on external pollinators such as ants, honeybees, and bumble bees. The quality and frequency of their activity is intrinsically tied to the success of the agri-food sector and all adjacent industries. The matter is therefore worthy of rigorous consideration when investing in agriculture.

Commercial fruit and vegetable producers – a group with the most economic dependence on the ecosystem services offered by pollinators – are seeing consistently declining pollinator populations.(5) Ecosystem biodiversity is at a lower level than needed to sustain healthy colony numbers, and investors may have a part to play in solving the issue.(6) Investors with access to local expertise, an understanding of biological sciences, and flexibility in capital deployment may benefit from investing in the preservation of native pollinators as part of their asset management activities. This may also be a key factor in underwriting new investments in fruit and vegetable land, as crop yield and quality fluctuates in proportion to the amount of pollination it receives.(7) Native wild pollinators have been shown to increase the shelf life and commercial value of fruit crops versus their domestically managed counterparts.(8) From the farmer’s standpoint, permanent crops such as orchards, vineyards and bushland as well as row crops like canola, beets, and strawberries are all dependent on external pollination.

Neonicotinoids

There exists a contentious issue in modern agricultural communities where pesticides such as neonicotinoids, which account for about 25 percent of global agro-chemical sales, are perceived to cause destructive effects to bee colonies. As there exists a correlation between higher pesticide use and regional colony collapse disorder frequency, countries who use the most pesticides are projected to have more rapidly declining bee populations. With this being said, a statistically significant study of causation has yet to be found, and the issue continues to be debated in agricultural circles. Exhibit 1 shows the extent of pesticide use by country.

Exhibit 1: Pesticide Use per Hectare of Cropland (kg/ha), 2014

Source: United Nations Food and Agriculture Organization, 2014

As seen in the above chart, farmers in countries such as China and the Netherlands use three times more pesticides on their crops than farmers in the U.S., UK and Canada. The latter countries may attribute part of their moderation in chemical use to the cold winters which naturally regulate pest and disease risk. Countries with year-round growing seasons and extended periods of wetness are more susceptible to the growth of undesirable organisms. In contrast, pollinators such as bees are more likely to thrive in Canada due to its lower population density, greater extent of forested regions and reduced use of pesticides compared to other agricultural producers.

Honeybees

A recent comprehensive study indicates that the U.S. agricultural landscape is 48 times more toxic for bees than just 25 years ago.(9) Honeybees, which are used by the US Environmental Protection Agency (EPA) as a proxy for other insect populations, are consistently declining in numbers throughout North America. As insect populations drop, bird populations that rely on insect nutrition also decline.

Despite the abundance of rhetoric surrounding honeybee colonies in the United States, the insect is not native to North America. Their genetic predecessors were first seen in Asia over 300,000 years ago and the species we see today was brought to the Americas by early colonists.(10) Honeybees may be thought of as a domesticated species, similar to livestock, that are bred, managed, and shipped from farm to farm for their pollination capacity of crops such as blueberries. While they do provide additional economic value through their productive capacity for honey, honeybees are generally less efficient than native pollinators and are prone to spreading diseases to other insects.(11) Global pollinated crops are valued at over US$212 billion per year, a value that is expected to accelerate at a pace faster than typical grain crops due to a growing global appetite for fruits, nuts and vegetables.(12) Exhibit 2 demonstrates where pollinator services provide the greatest benefits on a per hectare basis.

Exhibit 2: Pollination service contribution to the crop market output ($USD/ha)

Source: Potts et al., 2016(13)

The map above shows areas such as southern Europe and Asia as key regions where investment in pollination service could make the greatest improvement to crop market outputs. The total value of pollinator services may be attributed to thousands of species; however, and as some academics have stated, honeybees have a tendency to “hog the limelight”(14).

Alternative Pollinators

While honeybees are in vogue as a topic of discussion, non-bee pollinators such as flies, beetles, ants, wasps, butterflies, bats, and birds are all important contributors to global crop production.(15) Some studies estimate that these alternatives offer up to 50 percent of total pollinating services for all fruit, nut and vegetable crops.(16) With this being said, secondary pollinators are less efficient per visit, and cannot be relied upon to replace bee populations for specific crop types and climatic zones.

Considering that ecosystem fragility is a national or even continental issue, opportunities to work with governments in the form of Public-Private Partnerships may offer interregional solutions. Initiatives such as the Integrated Crop Pollination Project may be pointed to as a progressive example of the intersection between profitable farm management and environmental enhancement. An analysis from the Journal of Economic Entomology estimates that profit per acre can increase by over US $2,000 per acre of tree fruit land by incorporating alternative pollinators such as the native blue orchard bee on farms in North America.(17) This requires maintenance, expertise, and the deliberate allocation of patient capital, forgoing short-term profits for long-term gains.

Pesticides are necessary for generating the long-term crop yields that are needed to nourish the growing global appetite, but the management with which they are applied is crucial to preserving a diverse ecosystem – both above and beneath the soil. Strong evidence suggests that large-scale fruit and vegetable farmers could benefit from investing in the establishment and stewardship of wild pollinator colonies. Governments and enterprises are adopting a broader recognition for the roles that biodiversity and ecosystem services play throughout the value chain.(18) This is underpinned by a consumer base with preferences for supporting transparency and sustainability – a trend that is unlikely to disappear. Companies and investors who act early on this issue may benefit from an early mover’s advantage, industry recognition, and the development of proprietary processes.

Note: this article first appeared in Global AgInvesting on October 1, 2019 globalaginvesting.com. This is the sixth article of an eight-part series published by GAI News that will examine how the global food system is set to be altered by eight existing trends. Each month a new installment will be released. Click the following links to read the first five installments: Part I , Part II, Part III , Part IV and Part V.

Written by: Jeremy Stroud, Bonnefield, Agricultural Investment Analyst

“Phosphorus has no substitute in sustaining all life and food production on our planet.” – Ashley, Cordell & Mavinic

There are few nutrients more essential to the progress of industrialized society than phosphorus. The mineral is necessary for plant growth, it is finite in its accessible form and it cannot currently be replaced by synthetic means. The implementation of phosphate rock in soils has allowed our society to flourish and scale just as much as any other agricultural innovation, and as leaders, it is time to take a closer look at the implications of its use.

Incorporating mineral fertilizers, such as phosphate and ammonium nitrate, into modern cropping systems is responsible for at least 40 percent of crop yield growth since the mid-nineteenth century. [1] That amounts to more food than humans had produced in the previous twelve thousand years combined. Phosphorus is used by farmers to promote the storage and transfer of energy and enable processes such as photosynthesis, respiration and nutrient transportation. While manure was originally used for its phosphorus content, industrialists in central Florida found that phosphate-rich rocks could be mined and applied to our soils for the same purpose. [2] While nitrogen, the other major element for plant growth, may be formed through naturally occurring cycles, phosphorus typically cannot. Here lies the crux of the matter: the agricultural sector is currently mining and using phosphate at an unsustainable pace and it will be farmers, particularly in developing countries, who will feel the effects most profoundly.

Growing Demand and Shrinking Supply

Last year 270 million tonnes of phosphate were mined throughout the world – a 20 percent increase from 2014 levels and a 38 percent increase since 2011.[3] For context, there are about 70 billion tonnes of known phosphate reserves, 80 percent of which is not feasible to access with current extraction technology. Modern row crop species such as corn, wheat, soy, and rice have been bred with ravenous appetites for phosphorus, and consumption has risen in a non-linear fashion since the 1960s as farms have depleted their soil’s naturally occurring nutrient stores. Some estimates suggest we will reach peak phosphorus production by 2040, others by 2070, and others in the 2100s.[4] Regardless of the estimated timeframe, the peak may very well come, and it will likely trigger a surge in fertilizer prices for agricultural producers. The chart below demonstrates the source of phosphorus use per acre in farmland globally.

Figure 1: Historical Global Sources of Phosphorus Fertilizer, 1800 – 2010 [5]

Source: Cordell et al., 2009

In addition to the issue of its scarcity, phosphate reserves are not evenly distributed. Over 75 percent of the world’s phosphate stores are in Morocco and Western Sahara which is effectively controlled by Morocco. Massachusetts Institute of Technology estimates that we have less than 80 years of readily available deposits left at our current rate of consumption. [6] The image below shows the largest phosphate mine in Africa, Bou Craa in the Western Sahara, which holds about 3 percent of the world’s phosphate rock.[7] It is the size of 3,000 football fields and utilizes a 100 km conveyor belt, the largest in the world, to move the crushed product to its coast for export.

The phosphorus dilemma has become a balancing act between applying phosphorus to increase crop yields and feed the population, while also responsibly extracting and applying the resource. Our historical practices have been heavily slanted towards the former.

Bones of Contention: Necessity Versus Excess

With only 15 percent of phosphate absorbed for plant use, surplus minerals added to the soil are generally lost due to runoff, leaching or accumulating in its non-accessible form. As dissolved phosphates reach local waterways, they activate phytoplankton growth which begins the process of eutrophication, thereby spurring mass algal blooms, fish mortality and riverbed sedimentation. Dissolved phosphates also have a tendency of entering groundwater and aquifer sources, leading to the deterioration of water health and, in some cases, contamination of drinking water. So how can we reduce reliance on phosphorus while also maintaining strong yields? How can we prevent eutrophication and ensure the plant retains more of the phosphate applied? The answers lie in responsible investing, management and oversight of farming practices. In short, reducing our phosphate use and implementing sustainable techniques could rebalance the natural phosphorus cycle.

1. Invest where phosphorus is not a constraint

Quite simply, some farming regions use far more phosphate rock per hectare than others. The European Union, Canada, and the US combined will use less than half the phosphate per hectare than China. As seen in Figure 2, Canada applies some of the least phosphate fertilizers per hectare of any major grain producer.

Figure 2: Phosphate Use per Hectare of Cropland, 2002-2014

Source: United Nations – Institute for Environment and Human Security (UN-EHS), 2015

Canadian, US and European grain farms generally require less phosphorus and potassium, yet more nitrogen fertilizer than other comparable farms in Brazil, Australia and Europe. This is due to their history of less-intensive farming practises, their colder winters, their common crop rotations, and their typical soil nutrient profiles. This allows Canadian farmers to be in a sustainable position over the next century as phosphate reserves continue to be depleted, while nitrogen requirements may be achieved through manure application and crop rotation techniques.

2. Conservation practices and biologicals

To become available for plant production, organic phosphorus may be mineralized by micro-organisms in the soil. One specific organism, a fungus known as mycorrhizae, works in a symbiotic way with over 80% of vascular crops such as wheat, corn, potatoes, and rice. It has adapted to help plants for this very purpose, with the potential to be used to increase phosphorus uptake efficiency by 50%. This is an active biotechnology that has been around for 450 million years, and its further incorporation into our crop mix could provide meaningful effects for agricultural sustainability. The use of common bush crops, such as the Mexican Sunflower, may be used as a green manure which adds organic phosphorus to the soil as well.[8]

3. Innovation and Technology

Some researchers, governments, and startups believe that the effects of the phosphorus issue may be reduced by applying fertilizers with more precision and through recycling our existing products. Startups such as NuReSys aim to recover phosphorus nutrients from human urine.[9] Geneticists are also working towards phosphorus efficient rice crops with larger root systems which would be able to extract more available phosphorus in the soil.[10] In addition, targeted fertilizer applications can reduce the amount of phosphate used by farmers, thereby cutting their costs and mitigating potential nutrient leaching.[11] As farmers and businesses incorporate more technology with environmentally beneficial characteristics, the challenge of phosphorus overuse may begin to turn into an opportunity.

Throughout this series, the same point has been made; those who have the opportunity to allocate capital also bear the responsibility to deploy their resources towards environmentally resilient strategies and regions. A Greek Proverb may articulate this notion more eloquently:

“A society grows great when old men plant trees whose shade they know they shall never sit in.”

Note: this article first appeared in Global AgInvesting on September 4, 2019 globalaginvesting.com. This is the fifth article of an eight-part series published by GAI News that will examine how the global food system is set to be altered by eight existing trends. Each month a new installment will be released. Click the following links to read the first four installments: Part I , Part II, Part III and Part IV.

Written by: Jeremy Stroud, Bonnefield, Agricultural Investment Analyst, and Michael DeSa, AGD Consulting Founder

With the advent of sprawling wildfires throughout Brazil’s Amazon rainforest, politicians, businesses, and investors in timber and agriculture within the region are prompted to sincerely consider the ramifications of their asset management practices and investment decisions. While many forest fires occur as a natural and beneficial reaction of the local ecological cycle, this is not the case for the Amazon. Despite the fact that these fires have taken place in Brazil’s dry season, INPE, the Brazilian national space agency, has documented an 83 percent increase in fires since the previous year,[1] while deforestation has increased by 67 percent since January 2019.[2] The El Niño dry period likely contributed to the severity, although INPE has directly connected these fires with the recent onslaught of deforestation and greenfield agricultural development.[3]

The Amazon basin supports over half the world’s tropical rainforests and currently acts to offset approximately one quarter of human-caused greenhouse gas emissions.[4] Events taking place in Brazil serve as a vivid reminder of weather volatility and its intersection with global agriculture. This issue explores severe weather events, natural disaster risk in farming regions and the implications for investors. The findings reaffirm similar themes in past installments: those who have the opportunity to invest in land and water resources also bear the responsibility to allocate their capital towards environmentally resilient regions and strategies.

While we previously wrote about global warming, carbon emissions, and the long-term growth of global surface temperatures, this article reflects the opposite side of the climate change coin. It pertains to the immediate consequences of severe weather events and natural disasters. As temperatures increase, additional moisture is retained in the air which leads to heavier downpours and a higher frequency of extreme precipitation events.[5] On the other hand, warmer weather also accelerates the pace of evaporation, leading to circumstances where droughts and wildfires may prevail. Agriculture has always succumbed to the forces of unsettled weather behavior, although trends project increased volatility in each of the next several decades. Extreme events are accelerating at a tremendous pace, and Figure 1 exhibits just how fast it is happening.

Figure 1: Occurrence of Global Natural Disasters[6]

Source: International Disasters Database (EM-DAT), GMO Investments, 2018

According to the UN’s Food and Agriculture Organization (FAO), over 20 percent of economic losses due to natural disasters are absorbed by agricultural businesses worldwide with natural disasters accounting for approximately one quarter of annual crop losses.[7] Beyond losses to farm yields, severe storms and droughts also constrain logistical systems that service the agri-food industry. River traffic throughout the Mississippi River, for example, was reduced significantly after a drought in 2012 narrowed the route. We also witnessed substantial flooding this spring in the U.S. Midwest where farmers experienced delayed planting, destroyed facilities, and increased spoilage for crops in storage.

Although natural disasters are indiscriminate in their movements, each geography faces a different level of risk. Figure 2 depicts each country’s susceptibility to natural disaster risk from the 2018 World Risk Report by the United Nations Institute for Environment and Human Security. It offers insight on a country’s exposure and vulnerability to potential natural disasters by analyzing historical data. The study ranks 173 countries by measuring an average citizen’s probability of being exposed to natural hazards such as floods, storms, droughts, sea level events, and earthquakes.

Figure 2: World Risk Report – Risk of an Extreme Natural Event Leading to Disaster[8]

Source: United Nations – Institute for Environment and Human Security (UN-EHS), 2018

The multi-year United Nations analysis identifies Central America, West and Central Africa, Southeast Asia, and Oceania as the areas with the highest global disaster risk. It indicates that while many countries are improving their disaster preparedness, extremes in weather systems are expected to occur more frequently with heightened potential for negative consequences.[9] Although the concern is growing throughout the world, Canada and Europe’s diversified geography and cooler climate position them as some of the lowest risk regions in the world. Countries with robust national emergency management systems have also helped to partially mitigate the devastating effects of severe weather and geological systems.

The Modern Investor’s Response to Catastrophe

The Cambridge Centre for Risk Studies uses a series of scenario analyses to assess the impact of hypothetically likely natural disasters on financial markets and investment portfolios.[10] The study forecasts significant economic consequences for equity markets if any of these events were to occur. For example if Mount Rainier, an active volcano in the state of Washington, were to erupt, the S&P 500 and Dow Jones Industrial Average are expected to suffer a 20 percent loss.[11] Other scenarios that were studied include floods, hurricanes, and earthquakes, and although each have a low probability of occurrence, they collectively exemplify the potential for a large destructive event.

There are few winners in the wake of catastrophe, as production capacity, investor confidence, and local infrastructure all suffer. As such, traditional portfolios consisting of public equity and fixed income assets are particularly vulnerable to natural disaster events due to their global interconnectedness. In the event of an extreme disaster with over US$1 trillion in damages, returns are expected to suffer in a non-linear manner with their risk-tolerance as global markets are perturbed. Investing in a diversified portfolio of real assets such as infrastructure and farmland in low-risk geographies may act to offset economic losses brought forth by severe environmental events and fluctuations.

Investors may also consider allocating capital towards regenerative agricultural practices and land portfolios with disaster prevention infrastructure in place. Regenerative agriculture, which works to increase soil organic matter content, will increase the resilience of soil structures, thereby increasing moisture retention during times of drought and reducing topsoil erosion in heavy downpours.

Recent events have provided all agricultural investors, no matter their exposure to specific geographies, commodities, or strategies, with the opportunity to consider the long-term ecological consequences of their actions. Preservation of capital with positive environmental and economic returns may be achieved with careful due diligence and investment discipline. Critically acclaimed investor, Jeremy Grantham, may have best articulated the matter in his most recent report:

“We’re racing to protect not just our portfolios, not just our grandchildren, but our species. So get to it.”

Note: this article first appeared in Global AgInvesting on July 24, 2019 globalaginvesting.com. This is the fourth article of an eight-part series published by GAI News that will examine how the global food system is set to be altered by eight existing trends. Each month a new installment will be released. Click the following links to read the first two installments: Part I , Part II and Part III.

Written by: Jeremy Stroud, Bonnefield, Agricultural Investment Analyst

“The global average temperature for June 2019 was declared the hottest ever recorded for the month.” [1]

Headlines such as these occur with such regularity that we tend to become desensitized to the magnitude of the statement. News of record-high temperatures, melting glaciers and unprecedented carbon dioxide (CO2) levels have become so commonplace that they are now a focal point of political discourse and investment decision-making. Investors in all asset classes are assessing how they can limit their exposure to the effects of global warming, and there are few industries more intertwined with climate change than agriculture. Capital deployed in the agri-food industry, and more specifically in farmland, is set to face structural challenges in the long-term. Structural challenges such as these naturally lead to opportunities for investors with the foresight and patience to execute on long-term investment theses. This article explores how rising temperatures and CO2 levels are projected to affect global land suitability over the course of this century, and present the select few regions which may benefit from these new climatic conditions.

Carbon Dioxide and Heightened Temperatures

Temperatures are set to accelerate at a pace greater than we have seen since the glacial retreat of the last ice age as atmospheric CO2 has reached its highest level in the past three million years[2]. Warming occurs when certain greenhouse gases, such as CO2, restrict heat from escaping the atmosphere[3]. In the short term, higher CO2 levels may benefit crops such as soybeans and wheat due to increased photosynthesis capacity and water retention; however, the greater picture appears quite different[4]. Figure 1 portrays the earth’s average CO2 levels over the past 800,000 years.

Figure 1: Historical CO2 Levels in Parts Per Million

While global surface temperatures have already increased by about 1ºC since 1950, global temperature is projected to increase by another 2.5ºC in the next 40 years[5] and up to 4.5ºC by the end of the century, at the current pace of emissions[6]. This is poised to cause depletion of water resources, rising sea levels and severe pressure on our collective environmental system. Figure 2 demonstrates the historic global surface temperature compared to the 1951-1980 average since 1900.

Figure 2: Global Surface Temperature Compared to 1951-1980 Average

Source: NASA Goddard Institute for Space Studies, GMO Investments, 2016

Dropping Yields and Changing Fields

As each plant variety has a designated temperature range within which it can grow and reproduce, additional heat stress caused by global warming will stunt various crops’ ability to pollinate, retain moisture, and develop roots. Increasing temperatures, therefore, are expected to decrease the land area conducive to the production of high-calorie crops such as wheat, soy, and corn. A National Academy of Sciences study estimates a 5 to 15 percent decrease in grain crop production for each degree Celsius over current levels[7]. With temperatures currently rising, a rebalance of the agrarian equilibrium and a loss of biodiversity in oceans and forests is already taking place.

Overall crop yields are expected to begin their decline by 2030, and certain northern regions will be relied on to meet global nutritional needs[8]. Diseases, weeds, and insects, which thrive in warmer conditions, are expected to multiply and further restrain yield growth, while food nutrition is set to drop. Total yield decline is attributed in part to water scarcity and greater rainfall variability, the proliferation of pests, extreme heat events, and the reduction of multi-cropping in equatorial regions[9]. The International Food Policy Research Institute also recently published a study which found that plant nutrient availability is forecasted to significantly decline as a result of growing atmospheric CO2 levels[10]. Protein, iron, and zinc could each decline by between 15 and 20 percent in global availability over the next 30 years according to their model. In short, the world’s growing demographic will require more food to supply consumers with the same nutritional profile that we currently enjoy. Our collective ability to achieve this depends on an increase in crop yield per unit of farmland, in addition to an increase in global farmable land base.

Figure 3 depicts the forecasted change in farmland suitability to grow the 16 most common crops from averages in 1981–2010 to 2071–2100. Green areas exhibit an increase in suitability, while yellow and brown colored regions reveal where a decrease in land suitability occurs.

Figure 3: Change in agricultural suitability between 1981–2010 and 2071–2100.

Source: Zabel, Putzenlechner & Mauser, 2014

The researchers who produced this map use an internationally recognized climate scenario model to determine the climatic and topographic changes that are expected by the late 21st century[11]. The findings from this study are clearly stated: higher latitude areas such as Canada, Norway, China, Russia, Mongolia, and parts of the United States are expected to grow in suitable land area by 2100. On the other hand, many warm-climate regions, which are accelerating in population growth and therefore nutritional needs, will face reduced land suitability.

Investing Where It’s Cool: The High Latitude Thesis

A longer growing season and additional heat units for crops such as wheat and corn will increase the area in northern regions that are conducive to temperate cereal cultivation. Figure 4 shows the boreal forest in green, along with the estimated movement of agricultural suitability boundaries in the northern hemisphere.

Figure 4: Northward shift of the agricultural climate zone under 21st-century global climate change King et al., 2018

By 2099, about 76 percent of the area shown in green above is expected to reach crop feasible growing conditions compared to the current 32 percent[12]. For long-term investors with investment horizons of over 20 years, boreal regions such as the Clay Belt in Ontario and the Northern Prairies of Alberta are forecasted to become viable for large-scale grain and pulse production as temperatures increase. In these regions, the sparse populations and significant levels of capital needed to prepare the land for production have kept asset prices reasonably low. With the correct local knowledge and capital flows, tens of million acres in Canada and Russia that were previously untouched could emerge as the final frontier of scalable farmland use.

The high latitude investment thesis is not only underpinned by an increase in suitable land, but also an expected increase in crop yields. Figure 5 demonstrates the projected change in yields by sub-region between 2010 and 2050 considering a 3ºC increase in temperature from pre-industrial levels.

Figure 5: Projected Impacts on Crop Yields in a 3°C Warmer World

Source: World Resource Institute, The World Bank, 2010

The high-latitude investment thesis calls to immediate question the fact that many forested areas, which act as carbon sinks, would need to be converted to scalable crop production. It is then crucial for investors and policymakers to consider alternatives for preserving global ecosystem services, perhaps by investing in carbon offset programs or tree re-planting projects. With the knowledge and technology now available, investors are also urged to promote and implement production techniques that preserve and enhance affected ecosystem services. Evidence indicates that investment in regenerative agricultural practices, sustainable intensification, and maintaining soils with high levels of organic matter may mitigate some externalities of a warming planet[13]. Investment in foundational infrastructure strategies such as community development, transportation, green energy, and processing facilities could create opportunities for investors to diversify cash flows while integrating synergies with their farmland investments. A portfolio such as this would be a sustainable step forward to providing the world with the food it needs.