Bonnefield has always been a strong supporter of Canadian agriculture. For over a decade we have worked with farmers across the country to grow their operations, transition to the next generation, or stabilize and strengthen their balance sheets through a flexible land-based capital solution. Over this time, we have heard from many others interested to understand how Bonnefield could also support their businesses beyond farmland. Not only does this represent a natural extension of our existing farmland investment activities, but it is also in keeping with our commitment to the future of Canadian agriculture to find a way to support these operators. For this reason, we are launching a new investment vehicle, the Bonnefield Integrated Agriculture Fund, with a mandate to invest in agri-businesses and on-farm infrastructure via non-controlling capital for leading operators.

When we think of food production in Canada, the focus is often on primary production, particularly crop and livestock farming, or on the manufacturing and sale of finished products such as baked goods, shelf-stable products, bottled beverages, packaged fresh and frozen produce, and other readily consumable items that are available at most food retailers. However, there are a number of integral steps between primary production and the sale of finished products to consumers. The journey that our food takes from field to plate is complex and, while each part of the agri-business value chain faces unique challenges, we believe that there is significant opportunity and need for investment and growth in this sector.

A Primer on Canada’s Agri-Business Value Chain

Food production begins with primary agriculture, which encompasses the core activities that are performed within the boundaries of farms, nurseries, or greenhouses(1). Primary agriculture can include growing and harvesting crops (e.g., grains, fruits, vegetables), dairy farming, raising livestock and poultry, and aquaculture.

After food leaves the farm, processors transform raw food inputs into products and by-products that are either finished and ready to consume (e.g., milk, meat, packaged fruit and vegetables) or are then used in further value-added processing to create other goods (e.g., oils, flours, extracted proteins). Most of the food that we eat must be processed in some way prior to consumption. To take a simple example: wheat must be grown, harvested, graded (inspected and assessed for quality), cleaned, dried, ground, packaged, and shipped before it can be used to make food products such as bread.

Storage and logistics also play a fundamental role through the entire process, ensuring that food products are held safely, available for use, and able to move efficiently on to the next buyer or consumer. Grain storage and elevators, terminals, warehouses, cold storage and transloading facilities, and third-party transport providers (including trucks and railways) are a few notable examples of additional services and infrastructure that are necessary for food products to ultimately reach end consumers. These functions are essential in ensuring that Canadian food products are able to reliably reach domestic and international end markets. Notably, Canada is a major exporter of food to countries around the world and is expected to play an increasingly major role as climate change continues to affect where food is produced around the world in the coming decades.

Toward the far end of the value chain lies food distribution and retailing, and the foodservice industry. Wholesalers, grocery stores, diversified retailers, convenience stores, specialty retailers, and restaurants represent the most frequent and consistent touchpoints that many Canadians have with the agri-business value chain.

Overview of the Canadian Agri-Business Value Chain

Food Production: A Canadian Economic Powerhouse

Canada’s agriculture and agri-food processing sector is a major driver of our country’s economy in terms of production value, job creation, and international trade. Canada’s most recent Census of Agriculture reported that there were nearly 190,000 farms across the country as of 2021 which collectively employed 241,500 individuals(2). Primary agriculture also generated approximately C$32 billion, or 1.6%, of Canada’s gross domestic product (GDP) for the year(2). The Census also reported that total farm cash receipts reached an astounding C$83.2 billion for the year, of which 57% (C$47.3 billion) was attributed to crops and 36% (C$30.0 billion) was attributed to livestock and livestock products, with the remaining portion comprised of direct payments(3).

Food and beverage processing was also a major source of production value and Canadian jobs in 2021, having generated C$33 billion, or 1.7%, of Canada’s GDP for the year and employing over 300,000 individuals(2). Food and beverage processing also represented the single largest manufacturing industry in Canada in 2021, accounting for nearly 18% of all manufacturing-related GDP for the year(2). Interestingly, approximately 70% of all processed food and beverage products sold in Canada were manufactured by domestic producers in 2021, with half of the imported products having been manufactured in the U.S. and the remaining imported goods sourced from other countries around the world.

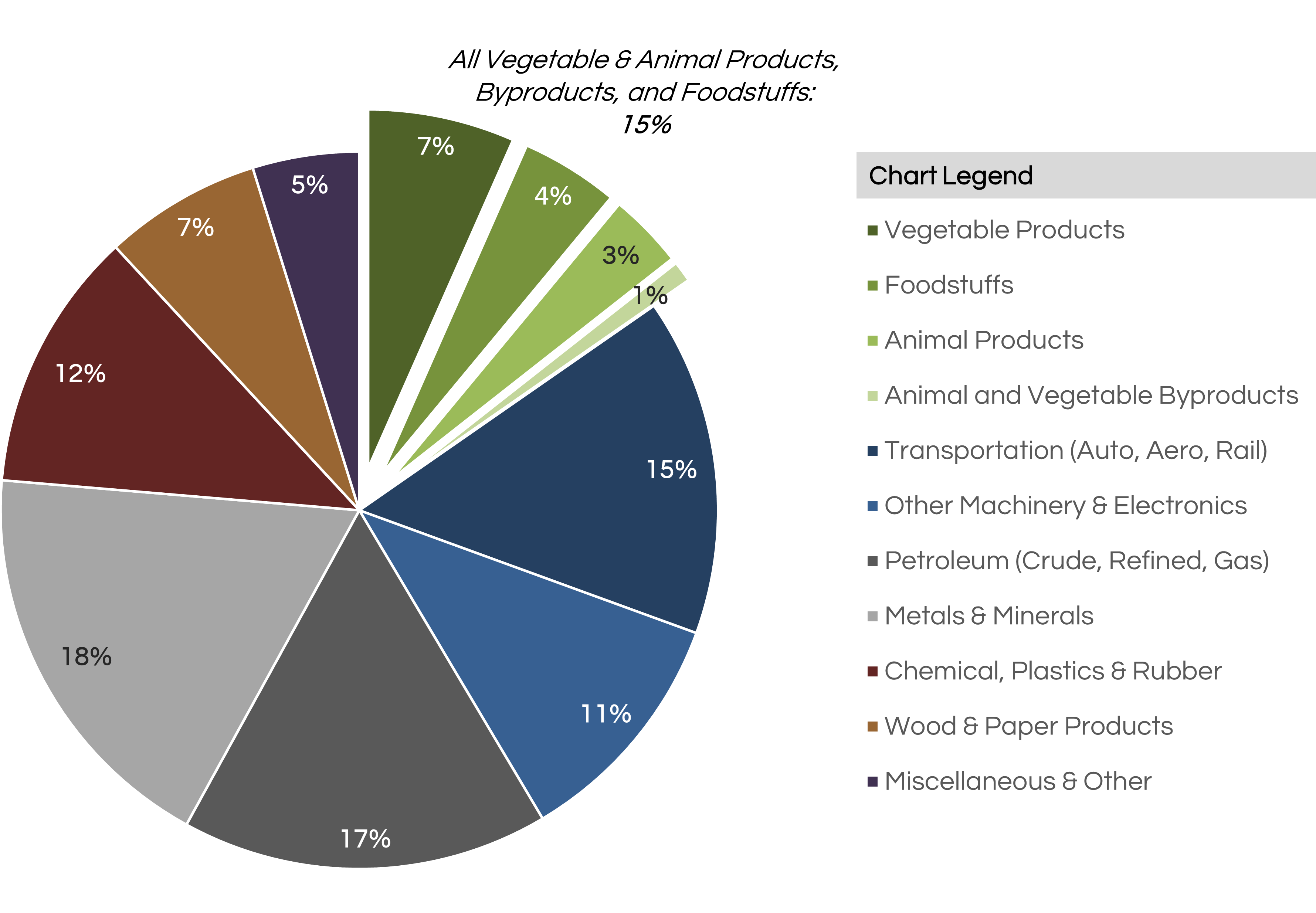

The economic importance of Canadian farming and food processing is further underscored when we look more closely at international trade. In 2020, the total trade value of all of Canada’s exports reached C$370.8 billion dollars, of which C$56.9 billion or 15.3% was attributed to collectively to vegetable products (C$24.5 billion / 6.6%), foodstuffs (16.3 billion / 4.4%), animal products including meat, cheese, eggs, and milk (C$12.5 billion / 3.4%), and animal and vegetable by-products including oils (C$3.5 billon / 0.9%).

As seen above, the aggregate trade value of Canadian food exports rivalled the value of exports from several other natural resource sectors including oil & gas and the extraction of minerals and metals, as well as the export of automobiles, airplanes, and locomotive equipment.

The strength of Canada’s agri-business sector relies on a functional, efficient value chain that extends from primary food production through to distribution, whether to domestic or international end markets. As discussed in Bonnefield’s most recent White Paper exploring the effects of climate change on global agriculture, we believe that Canadian food production will prove to be increasingly important over the near- to mid-term as the effects of climate change begin to affect food production elsewhere in the world.

As Canadian production of certain food products, such as crops, fruit, and vegetables stands to increase due to favourable shifts in climactic conditions over the coming decades, we believe that major investment in increasing processing capacity and technology, along with storage and transportation infrastructure, will also be necessary as we look to the future.

A Need for Capital…

According to a 2018 study conducted by Canada’s Economic Strategy Tables discussing the state and goals of the country’s agri-food sector, Canada had 11,499 food and beverage processing establishments in 2017 of which 94.4% were small operations with fewer than 99 employees(5). Additionally, capital investment in the food processing industry, particularly machinery and equipment, as a percentage of sales dwindled from 2.3% in 1998 to just 1.2% in 2016, and R&D expenditures in the Canadian agri-food sector as a percentage of sales fell by 24% between 2008 and 2016(5). This suggests that there has been a sustained under-investment in Canada’s food and beverage processing industry that needs to be addressed.

Finally, the report indicates that the investments that have been made in food processing innovation were fragmented across educational institutions, food technology centres, research centres and locally focused incubators(5). While these organizations play an essential role in terms of research, their scope in being able to achieve scaled commercialization is intentionally limited(5).

Just as we saw a need for alternative sources of financing in the farming industry over a decade ago, Bonnefield recognizes that Canadian agri-businesses more broadly are also limited in their access to sources of capital. These companies are often operating in manufacturing-related sectors that are capital-intensive. They require machinery, facilities, and technology – any or all of which require significant funds to acquire and implement – to compete successfully and achieve growth. Traditional debt-lending provides meaningful support to these operators but complementary, industry-specific, alternative forms of financing are lacking in the Canadian market.

… and an Attractive Investment Thesis

For those looking to gain exposure to the attractive investment attributes of agriculture, investment in Canadian agri-businesses offers an appealing option. Not only is there demand for increased investment into the sector, but Canada specifically offers unique and attractive dynamics.

Diversification: In terms of crop farming, Canada benefits from a geographic landscape, soil types, and climactic conditions across the country that result in growing conditions that are hospitable for different crop types on a regional and localized basis. For example, farmers in New Brunswick have access to land that can successfully produce potatoes, whereas farmers in the Prairies have farmland and weather conditions that better suited to row crop farming. The same is true of other agricultural products, such as dairy, wild-caught and farmed seafood, and livestock. Given the diversity of agricultural production across the country, there are many unique opportunities for businesses further along the value chain to add value through processing, packaging, storage, and transportation of Canadian farmed products. We believe that this inherent diversification gives rise to a myriad of opportunities for investors looking to deploy capital in the space.

Demand for Canadian Products: Canada’s reputation for outstanding food product safety and quality is world-renowned(5). An increasing consumer focus on food nutrition and safety, combined with a growing global population and a changing climate-driven shift in where the world’s food will be produced in the future provides a strong rationale to support the thesis that demand for Canadian-made food products will likely continue to grow over the coming decades. To meet this demand, the entire value chain – from primary producers to processors and distributors – will need to grow. Naturally, we anticipate that this will create compelling opportunities to invest in Canada’s agri-business sector, particularly around achieving scale and innovating for the future.

Supportive Regulatory Environment: The Canadian agri-business sector also benefits from a regulatory environment that seeks not only to support existing industry participants, but to grow the industry over the long-term. One example of this is the Canadian Agricultural Partnership (“CAP”) – a five-year joint investment program through which Canadian federal, provincial, and territorial governments will invest C$3 billion between 2018 and 2023 to strengthen and growth the agriculture and agri-food sector(6). The CAP encompasses initiatives, program, and funding geared toward growing trade and expanding markets, innovation and sustainable growth, and supporting diversity(6). Though this is one of many examples of Canada’s long-term practice of providing governmental support for the agriculture and agri-business industry, it still stands that the sector has seen a lack of investment in recent decades.

Bonnefield’s Role

As Canada’s leading provider of supportive, flexible sale-leaseback financing solutions for Canadian farmers, Bonnefield has heard time and again from our farmers and network of business partners that there is a distinct need for investment in the Canadian agri-business value chain beyond the farm gate. The launch of the Bonnefield Integrated Agriculture Fund is a major milestone for our firm that represents an opportunity to further expand our presence as a partner in agriculture by supporting leading Canadian agri-business operators. We are excited about this evolution and look forward to contributing to the ongoing strengthening and growth of Canada’s agricultural industry.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.

The topic of food security has gained prominence through 2022 and has highlighted the important role that Canada will play in meeting future demands for food production.

Clickhere to watch the team at Bonnefield discuss this important issue in a discussion moderated by Catherine Marshall of Real Alts.

Permanent Crops and Canada’s Evolving Agricultural Landscape

As a major agricultural producer and exporter, Canada is a leading supplier of traditional cold-weather crops such as wheat and canola across the globe. However, higher-value permanent crops such as apples, berries and stone fruits are increasingly being grown in Canada as growing conditions continue to become more accommodative as a result of climate and weather shifts.

Bonnefield has been working with blueberry farmers for many years and recently completed its first transaction with a leading British Columbia-based grower of raspberries, as we continue to ensure our farmland portfolios reflect the diversification of the Canadian agricultural landscape. Below we break down some of the key differences between row crops and permanent crops and how changing growing conditions may impact the future economics of agriculture in Canada.

Row Crops vs. Permanent Crops – What’s the Difference?

The terms “row crops” and “permanent crops” may be unfamiliar to some. An easy way to distinguish between the two is to think about a permanent crop as one that does not require annual replanting. Examples of permanent crops in Canada can include apples, blueberries and grapes. In each of these instances, fruit is produced for multiple years on the same plant (biological asset). Row crops, on the other hand, are seeded annually (i.e. wheat, canola, barley, corn, etc.).

The risk profile of permanent and row crops varies due to the fact that permanent crops rely on the biological asset’s survival through the winter months and potentially volatile weather conditions through the entire year, over the course of several years. Permanent crops also tend to be more labour-intensive than row crops, requiring greater inputs from a time and materials perspective.

The demand and end-market profile for row crops and permanent crops also tend to be different. Due to a shorter shelf life a larger percentage of permanent crops are sold into local markets. In addition, demand for permanent crops depends more on consumer preference than demand for row crops does. For example, certain varietals of berries and apples are more popular today than they were a decade ago as end consumers’ size and flavour preferences have changed. Conversely, demand for row crops is driven by a variety of macro-factors such as global production and supply levels for key crops such as wheat and soy, as well as continued global population growth. As row crops are more likely than permanent crops to be processed prior to human consumption – for example, the milling and refining of flour prior to its use in producing baked goods – consumer preferences generally have less of a direct impact on overall demand.

Permanent Crops in Canada

Canada has not historically been known as a major grower of permanent crops. While approximately 34% of all Canadian farms were reported as oilseed and grain farming operations, just 4% were fruit and tree nut farming operations per Statistics Canada’s 2021 Census of Agriculture(1).

However, we are seeing a wider range of cultivars now available as a result of favourable climate impacts on Canadian agriculture. Historically, harsh winters have limited permanent crop production in Canada as permanent crops, which are harvested from trees, shrubs or vines that do not need to be replanted each year, generally require milder conditions to protect the plant through the winter months.

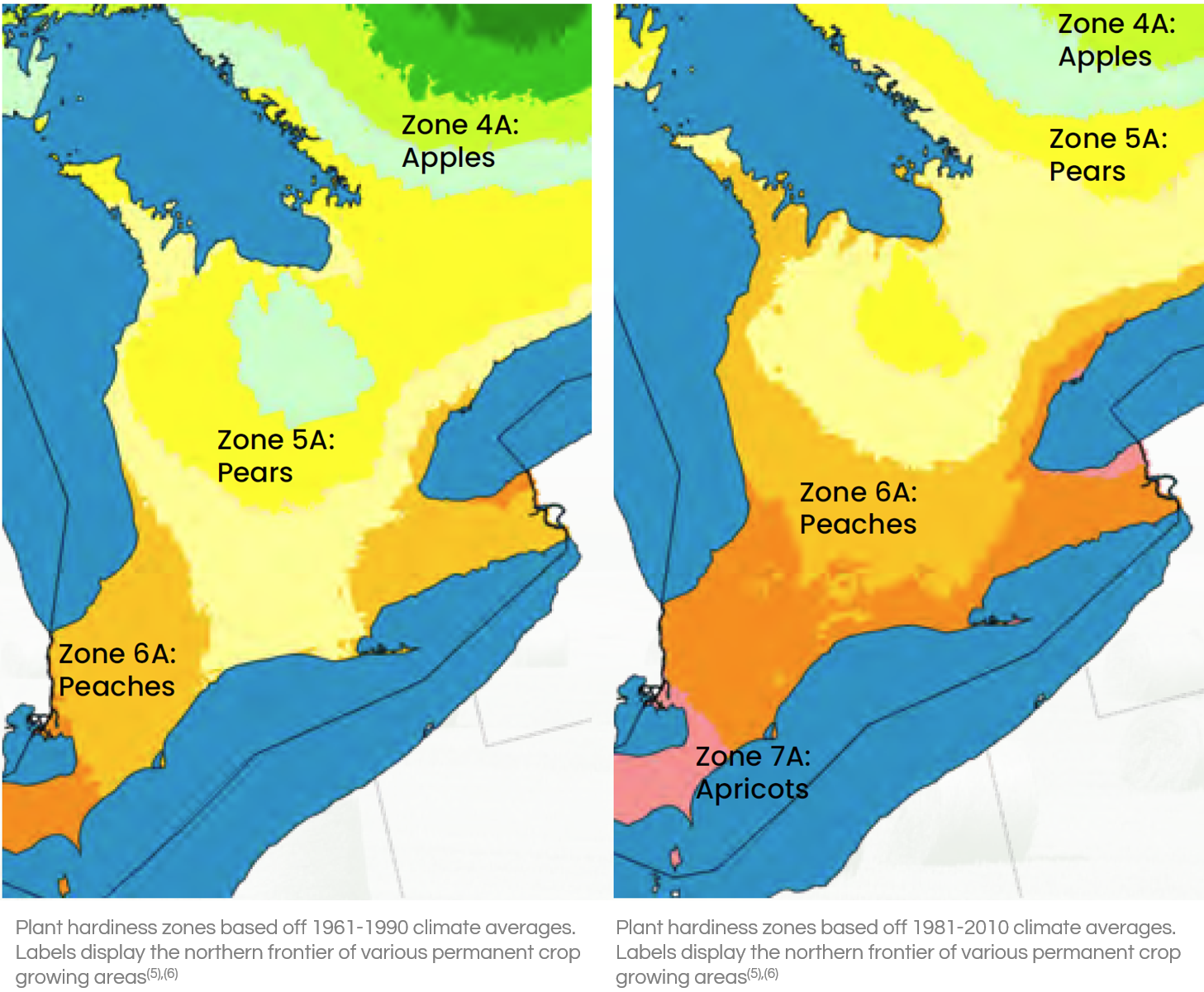

Producers use the Canadian Plant Hardiness Zone Mapping system to predict winter survival rates for their crops and, in 2010, these maps were re-drawn to reflect changing climatic conditions. The updated maps show a substantial northward migration of historical growing regions, and academic studies predict continued northward expansion of land suitable for growing warm weather permanent crops(2)(3). This change is exciting for Canadian farmers as permanent crops that have historically been grown in warmer, more southern parts of North America tend to command higher prices, which drive increased farm revenues and, ultimately, higher farmland values(4).

Bonnefield’s Experience

As previously mentioned, Bonnefield works with a number of leading permanent crop growers across Canada. We currently support apple, blueberry and raspberry producers through our alternative farmland financing solutions, and we continue to evaluate new varietals and growing regions in order to broaden our scope across the industry.

From our perspective, exposure to permanent crops offers valuable diversification that both de-risks our activities and provides us with exposure to farm operators with different and higher cash-flowing economic models than many traditional row croppers. While a single, standalone transaction in a permanent crop farm would likely demonstrate meaningful volatility and thus have a higher overall level of risk compared to a row crop operation, Bonnefield’s ability to complement exposure to permanent crops with a solid base of row crop investments creates an attractive risk/return profile for our holdings overall.

Additionally, our experience working with diversified permanent crop producers in Canada has further highlighted for us the benefit to being in Canada versus other parts of the globe. We all recognize that California has historically been a leading producer of high value permanent crops and a leading agricultural region. However, ongoing water shortages create significant strain on the industry and increasing heat units create risk for harsh growing conditions, and increased pest and disease prevalence. This increases the cost of operating in the region and enhances its volatility profile. Canada, on the other hand, has significant access to water resources and more moderate growing conditions. Our ability to grow varied permanent crop types is increasing which offers Canadian farm operators valuable optionality in their crop choices. Bonnefield is proud to be able to support these farmers throughout their business life cycle as we work towards the common goal of a strong and resilient Canadian agricultural industry.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.

Surging agriculture input costs, especially the prices of fertilizer and fuel, have been top of mind for many Canadian farmers as they kick off the 2022 seeding season. Fertilizer prices reached multi-year highs in Q4 2021, and the emergent conflict in Ukraine in early 2022 has only exacerbated the already-strong upward pressure on market prices.

According to Bloomberg’s Green Markets Fertilizer Price Index – which tracks North American fertilizer prices over time – fertilizer prices have more than tripled since early 2020.(1)

Green Markets Fertilizer Price Index (Nov. 2019-May 2022)

Source: Green Markets, a Bloomberg LP Company

The global supply chain has been massively disrupted since the onset of the global COVID-19 pandemic, as logistical bottlenecks built up at the world’s largest shipping ports while nations experienced labour shortages due to lockdowns, and dislocations affected shipping routes, air cargo, ground transport lines, and railways(2).

As countries around the world began to loosen pandemic-related restrictions through late 2021 and 2022, commodity prices have soared as result of pent-up demand and supply constraints, with fuel prices rising significantly. In addition, several recent events have further restricted the supply of fertilizer chemicals, such as ammonium phosphates, nitrogen, potash, and urea, resulting in continued upward pressure on prices:

Extreme Weather in the U.S.: Hurricane Ida hit the U.S. Gulf Coast in September 2021, effectively shutting down production and causing serious shipping delays and logistical challenges in New Orleans – the U.S.’s main trading hub for fertilizers(3);

Chinese Export Policy: China, one of the world’s key suppliers of urea, sulphate, and phosphate, imposed new customs regulations in October 2021 that included enhanced inspection requirements and new export certificates on a wide variety of export products, including urea and ammonium nitrate, that effectively curbed the export of fertilizers from the country. This move followed a September 2021 circular from China’s National Development and Reform Commission, the country’s economic planning body, calling for stability in fertilizer prices in the domestic market(4);

Russian Trade Restrictions: Russia temporarily halted the export of fertilizers from the country in March 2022, citing a lack of logistical connectivity and lack of transport ship arrivals in Russian ports after commencing an attack on Ukraine that continues to occur as at time of writing. Notably, Russia is also a major producer of potash, phosphate, and nitrogen-based fertilizers, and many countries have implemented sanctions against Russia as well as tariffs on Russian goods(5).

Fertilizer exports from the U.S., China, and Russia have historically reached differing end markets, with the main destinations for U.S. fertilizers being Canada, Brazil, and Mexico, whereas some of the key markets for Chinese and Russian fertilizers include Brazil, India, Australia, and Estonia(6). That said, the developments highlighted above collectively have led to an unprecedented strain on the global supply of fertilizer chemicals, thus impacting farmers and food prices across the world.

Global Fertilizer Trade

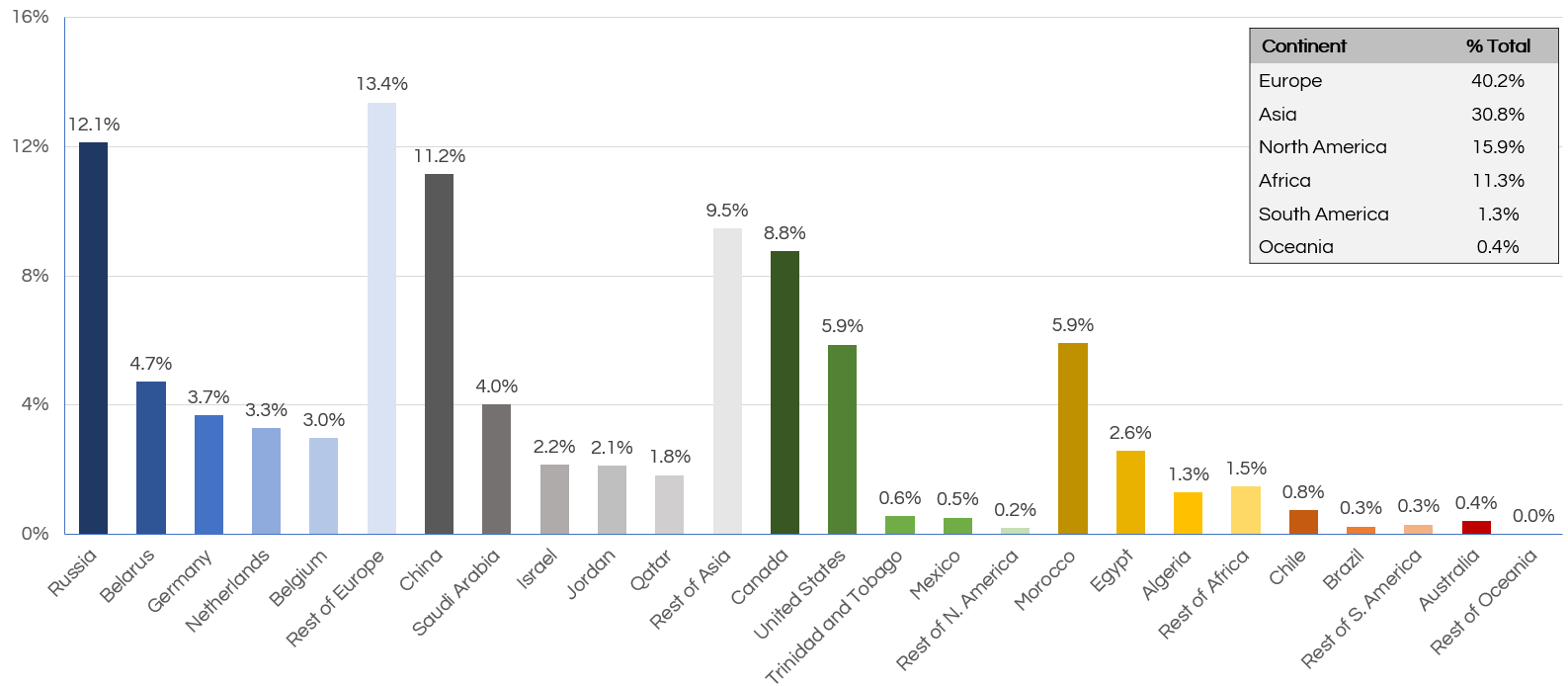

Fertilizers represent one of the world’s most heavily traded product types and, as shown below, the largest exporters in 2020 were Russia, China, and Canada

Largest Global Exporters of Fertilizers – Share of Global Export Trade Value by Country (2020)

Source: Observatory of Economic Complexity.

As noted, Russia and China have recently implemented increasingly isolationist-style export policies and, in 2020, the two countries accounted for ~23% of fertilizer exports globally(6). With these two major exporters limiting outbound trade of fertilizers, as well as the war in Ukraine and its trade implications (e.g., sanctions affecting the ability import of Russian goods), countries around the globe have directly felt the impact of supply limitations. Brazil and India stand to bear the brunt of the immediate supply shock, with Brazil and India having sourced ~26% and ~31% of their fertilizer imports from Russia and China collectively(6).

In Brazil’s case, there are concerns that the uncertainty and extremely elevated costs associated with sourcing fertilizer could hinder crop yields, resulting in a smaller harvest and even higher global food prices higher given the country’s importance in global crop markets. This is in addition to existing concerns around Brazil’s 2022 yields due to the possibility of extreme weather, like the severe drought experienced during the 2021 growing season(7). Brazilian farmers are considering various strategies of dealing with the shortage; SLC Agricola SA, one of the country’s largest producers of soybeans, corn, and cotton, is planning to reduce fertilizer usage by up to 25% in the coming year(8). On the supply side, major fertilizer producers are exploring ways to ramp up production, but doing so will take time and is thus not an immediate possibility. Canada’s largest potash producer, Nutrien, has committed to increasing its potash production by almost 1 million tonnes this year – the ramped-up production is expected in the second half of 2022(9), which is after the Northern Hemisphere’s seeding season. In summary, while major food and chemical producers alike are employing their best efforts to stabilize prices and ensure continuity of supply for both fertilizers and food, it could take months (or longer) before the impact of those efforts is seen.

A Canadian Perspective

Canada is the world’s third-largest exporter of fertilizers and has historically imported significantly less fertilizer in aggregate than it has exported(6). In 2020, the total trade value of fertilizers exported from Canada totalled approximately US$5.5 billion (C$7 billion(10)), whereas the total trade value of imported fertilizers was approximately US$1.4 billion (C$1.8 billion(10))(6). Notably, Canada is the largest global producer and exporter of potash, which refers to a group of chemicals and minerals that contain potassium (such as potassium chloride) that are most commonly used in fertilizers(11). Canada exported 22 million tonnes (“MT”) of potash in 2020, accounting for approximately 39% of the world’s total exports(11).

From this perspective, it may seem that Canadian farmers would be well-positioned to rely extensively on domestically produced fertilizer in operating their farms. However, it is important to note that successful crop growth requires a variety of different soil nutrients, some of which are not naturally occurring in soil and must be added through fertilizer application; as such, farmers cannot rely solely on Canadian-produced potash to grow their crops.

Canadian fertilizer production is very heavily concentrated toward potash, with 23 million MT having been produced between July 2020 and June 2021. In contrast, during the same period Canada produced approximately 4.8 million MT of ammonia, 4.5 million MT of urea (a form of nitrogen fertilizer), 1.5 million MT of urea ammonium nitrate (“UAN”), 1.3 million MT of ammonium sulphate, and less than 1 million MT each of ammonium nitrate and other fertilizer products(12).

We can also look to the Fertilizer Shipments Survey conducted by Statistics Canada on behalf of Agriculture and Agri-Food Canada for data on what types of fertilizer are shipped by manufacturers, wholesale distributors, and retailers to destinations within Canada to provide context on what types of fertilizers are used in Canadian farming(13). Between July 2020 and June 2021, the most-shipped fertilizer chemicals were urea (3.5 million MT of shipments within Canada reported), urea ammonium nitrate (1.4 million MT); and monoammonium phosphate (“MAP”; 1.5 million MT)(14). In addition to being a widely used fertilizer in Canada, MAP is water-soluble, contains the highest concentration of phosphorus of any common solid fertilizer, and has good storage and handling properties(15).

While Canada’s domestic production of both urea and UAN exceeded the total amount shipped to destinations within the country over that period, the same is not true for MAP(12)(13). In 2020, Brazil, Canada and Australia were the world’s largest importers of MAP, accounting for approximately 32%, 12%, and 7% of global trade value respectively, whereas the top exporters of MAP were Morocco (25% of global trade value), the U.S., (20%), China (19%), and Russia (16%)(6). The specific example of global MAP trade highlights that Canadian farmers do have to rely to some extent on importing certain fertilizer chemicals to generate strong crop yields while ensuring that the soil on their farmland remains in good health. Historically, the majority of Canada’s fertilizer imports have been sourced from the United States, with only a small fraction having been imported from Russia and China(6). With that said, Eastern Canada relies more heavily on Russian imported chemicals than does the rest of the country as there is essentially no local production of nitrogen, phosphorus, or potash in the region(16).

Fertilizer supply contracts are typically put in place by larger, more sophisticated Canadian farmers well in advance to ensure access to supply and allow for long lead times associated with production and shipping, with many of the contracts for 2022 having been established in 2021. That said, the 35% tariff on virtually all Russian imports implemented by the Canadian government in March 2022 went into effect as shipments were already en route to Canada from overseas destinations including Russia(10), which has resulted wholesalers and importers passing the tariff-related costs along to the end purchasers, including farmers(17).

As a result, Canadian farmers are currently in a position where they are reassessing whether they can apply smaller amounts of fertilizer and still achieve strong crop yields, or if alternatives (such as manure) present a viable option to minimize costs. Another unique aspect of Canadian farming is that many producers have some degree of optionality as to what crops they plant. For example, if the fertilizer specifically required to grow corn is not readily available, growers are able to switch to a crop that may need less fertilizer, or to a crop requiring fertilizer that their dealer can reliably source.

While input costs are on the rise, so too are the food commodity prices that drive farm incomes. Canadian farm cash receipts came in at an all-time high in 2021, marking a 9% increase over 2020, due primarily to record commodity prices(18). The strong growth in 2021 farm cash receipts was on the back of an already strong year in 2020, which had seen a 15% increase over the previous year(12). Higher revenue as result of food prices largely keeping pace with increasing input costs has provided some comfort for Canadian farmers with respect to their abilities to tolerate those cost increases over at least the near- to mid-term.

How Does This Affect Bonnefield’s Farmers?

Bonnefield’s farmers, who are progressive, well-established operators and have strong community ties, continue to be agile in their handling of the uncertainty around supply availability and costs. Many of our farmer tenants were very proactive ahead of the 2022 growing season, purchasing fertilizer well ahead of time. In addition, many of our farmers purchase seeds that already contain fertilizer which provides some flexibility as to the timing of fertilizer application should shipping delays occur. This are just some of the many examples of the resilience and business savvy that our farmers have demonstrated over the years.

Our team has heard in recent weeks that farmers’ main concerns aside from input costs remain primarily local for the time being and include domestic supply chain issues such as rail strikes, rising interest rates, and the possibility of unfavourable weather. The continued strength in food commodity prices has led to optimism that 2022 will be another year of strong farm incomes, which are a key driver of Canadian farmland values. Bonnefield offers our farmers long-term leases that are not immediately impacted by rising interest rates, and we act as a supportive partner to our farmers by investing in property improvements that might otherwise be delayed or forgone as result of other unforeseen expenses that strain farmers’ cash positions. As we have since our inception over a decade ago, Bonnefield remains committed to supporting our farmers through all conditions as a true partner in Canadian agriculture.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.

We are often asked about farmland lease rates across Canada as well as the relationship between lease rates and farmland value. This recent publication from Farm Credit Canada (FCC) provides an interesting overview of the topic.

We are seeing it at the grocery store and the gas pump – prices are rising. The topic of inflation is receiving a lot of attention as observers wait to see how governments will act to address those rising prices. With central banks around the world either considering or already increasing interest rates in 2022 to combat inflation, we are reminded that the prolonged low interest rate environment that has prevailed in Canada for more than a decade is atypical in the context of long-term monetary policy and is unlikely to persist indefinitely. In January 2022, Bank of Canada Governor Tiff Macklem noted in an interview during the same week that, “the message is pretty clear. We’re on a rising path.” (1).

More recently, on March 2nd 2022, Bank of Canada’s target for the overnight lending rate (a key benchmark for lending rates in Canada) was raised to 0.50% from 0.25% (2), marking the first time rates have changed since the COVID-19 pandemic in early 2020. In an accompanying statement, the Bank of Canada noted the emergence of conflict in Ukraine has led to increased uncertainty in global markets and has also caused prices for oil and other commodities to rise sharply in recent weeks, which will increase inflationary pressure above what was initially anticipated in January 2022 (2).

As a source of alternative financing for Canadian farmers, and a manager of a diversified portfolio of Canadian farmland, Bonnefield is often asked what impact rising rates may have on farm operators and farmland values in Canada. We’ve provided some thoughts on this complex relationship in the following sections.

A Recent History of Inflation and Interest Rates in Canada

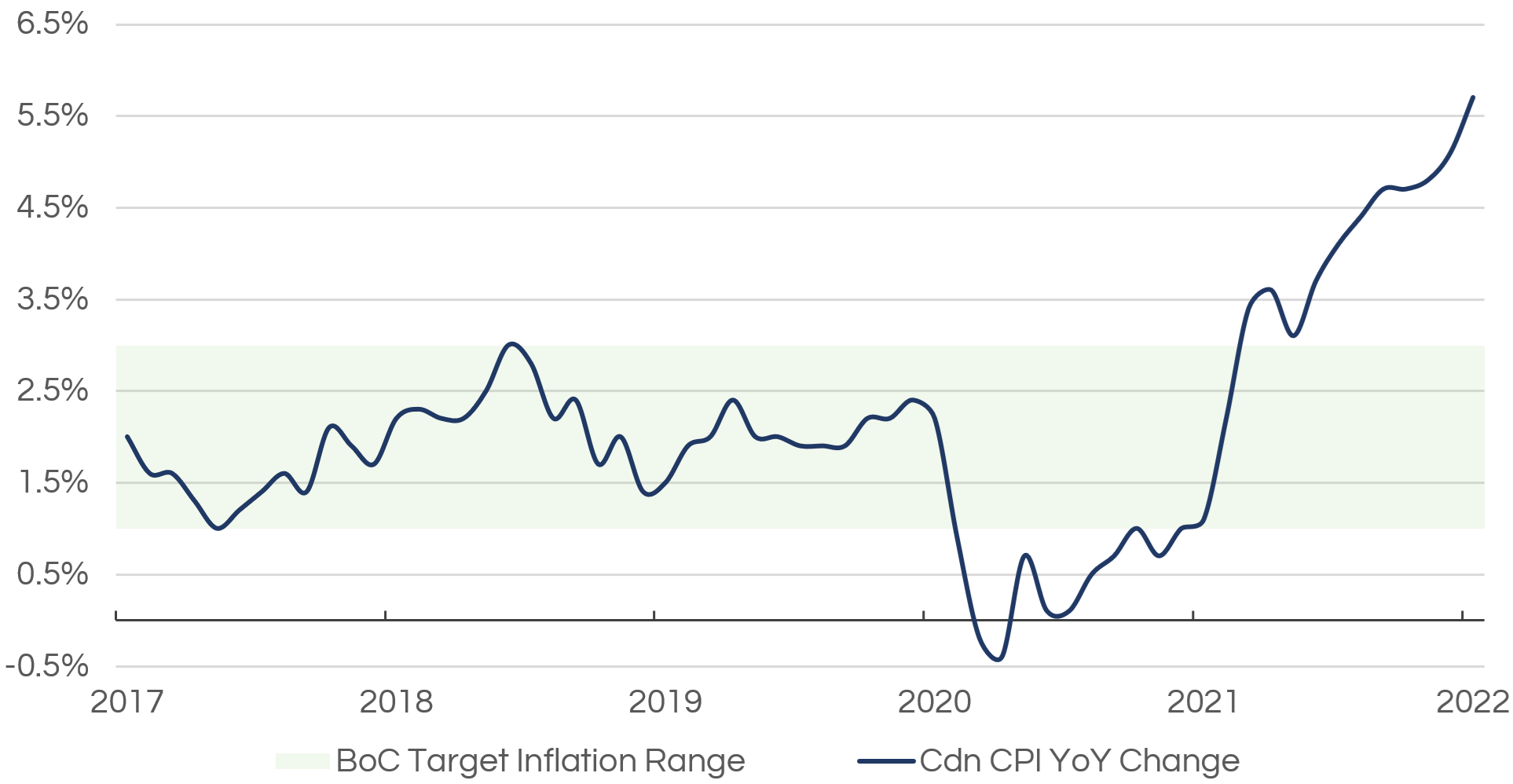

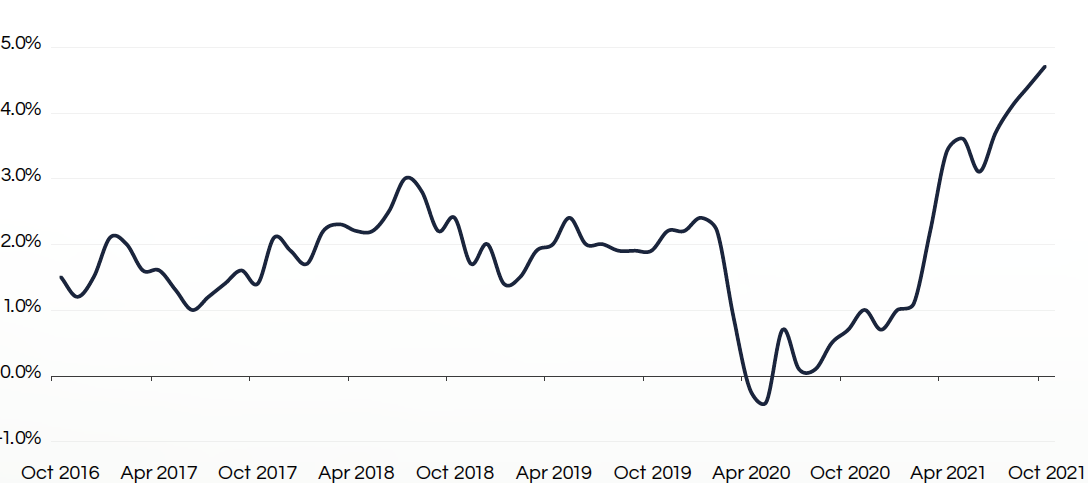

As of February 2022, the Canadian Consumer Price Index (“CPI”; index of all goods including gasoline) rose again to 5.7%, remaining above the Bank of Canada’s target normalized range of 1-3% reaching its highest level since August 1991 (3). Generally, prices begin to increase when the demand for goods and services outpaces the supply of those goods and services in the economy. Price inflation in turn reduces the purchasing power of individuals, which can have a significant impact on the overall standard of living.

When faced with increasing levels of price inflation, central banks have few policy options to cool price increases and to alleviate the financial strain caused by elevated prices for goods and services. A gradual increase in key lending rates, such as the Bank of Canada’s target overnight rate, can help to reduce spending, thus tempering the demand side of the equation and slowly reducing inflationary pressures. Despite a now-lengthy cycle of low rates and the continued effects of the COVID-19 pandemic, it is very apparent that increased interest rates are on the horizon. When asked about the timing of target rate hikes, Tiff Macklem responded to reporters in January 2022, “How far and how fast? Those are decisions we’ll take at each meeting, depending on economic developments, depending on our outlook for inflation, and what we judge is needed to bring inflation back to target.” (1)

Canadian Consumer Price Index (CPI) Monthly 12-Month Percentage Change Data (2016-2022)

Source: Bank of Canada, Statistics Canada.

Interest Rates on Farm Balance Sheets

From a balance sheet perspective, while the principal amount of a loan is not directly affected by a change in borrowing costs, the total amount of capital that must be repaid to lenders over time increases when rates rise. In turn, this increases the overall financial riskiness of farmers’ balance sheets and leads operators to carefully consider whether certain expenditures and investments are necessary.

From a profitability standpoint, the rates charged by financial institutions on traditional loans can represent a substantial expense for farm operators that primarily use debt to fund their operations, much like many other businesses. Interest rate increases are typically used by central banks as a tool to help temper rising inflation, and inflation also causes the cost of key inputs for farming operations (such as fertilizer, seeds, fuel, and equipment) to rise. Combined, an increase in borrowing rates coupled with elevated input costs can put significant pressure on farm profitability. However, as inflationary pressure also affects the market prices for key food commodities, some of that input cost pressure can be offset by increases in farm revenues and incomes.

Interest Rates and Farmland Values

Given the relationship between inflation and interest rates, and farmland’s demonstrated inflation-hedging characteristics, Bonnefield’s investment thesis is that in times of high inflation, Canadian farmland values perform strongly. Historically, farm incomes have increased during inflationary periods and strong farm incomes lead to rising farmland prices.

When valuing farmland, one of the most widely accepted approaches to establishing property values is to divide the rental income that can be generated by a property by a discount rate, which is based on an adjusted “risk-free” interest rate (often a Government of Canada bond yield or, more recently, the Canadian Overnight Repo Rate Average, “CORRA”). This equation, referred to as the capitalization method of valuation, effectively assesses the present value of potential future income generated by a property. Interest rates are a central part of the valuation equation and a higher discount rate (denominator) with no change to the rental income component would decrease the resulting value.

With that said, farm incomes are the single strongest direct drivers of farmland values, and the momentum in market prices for key commodities observed in 2021, and so far in 2022, suggests that incomes will remain healthy in the near-term. Further, while interest rate increases are coming more clearly into view, the overall cost of borrowing is still low compared to historic levels.

Over the years, Bonnefield has observed that when lending is relatively inexpensive and farm incomes are strong, farm operators have been eager to borrow funds to acquire additional land. In 2021, we also saw a high level of transaction activity in the market for Canadian farmland driven by both farmers having ample cash on-hand, as well as pent-up demand after relatively depressed activity in 2020 from the COVID-19 pandemic.

How Could Rising Interest Rates Impact Bonnefield’s Farmland Holdings?

Bonnefield’s core strategy is to invest in a diversified portfolio of prime Canadian farmland on a long-term, fully unlevered basis. We expect that rising interest rates will have a minimal impact on the value of farmland held by our investment partnerships or on the funds’ profitability. Further, as the leading provider of sale leaseback financing to Canadian farmers, Bonnefield’s partnership-based approach to providing an alternative source of capital to the agricultural community has helped many of our farm partners to strengthen their balance sheets by reducing debt. As such, we anticipate that our farmers will weather rising interest rates well. As always, we remain prepared to assist strong Canadian farmers who may have become over-levered by entering into long-term sale leaseback arrangements that allow operators to free up capital, clean up and stabilize their balance sheets, and invest in their businesses.

Having been a trusted partner of farm operators for over 12 years, Bonnefield has seen a number of economic conditions. One thing we know is that farmers are creative and resilient, able to adjust to a wide variety of market conditions in order to maximize the value of their operations. We are confident that this period of inflation and increased interest rates will prove to be no different and Bonnefield is available to support these operators through economic cycles.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.

It is impossible to read the news these days without seeing inflation-related headlines. Canadian inflation rates have generally been low and stable in recent years. However, recent data puts inflation at the forefront of investors’ minds. As countries around the world begin to emerge from the wide-scale restrictions and shutdowns implemented in early 2020 as a result of the COVID-19 pandemic, inflation numbers have steadily crept up with the latest year-over-year Canadian Consumer Price Index (CPI, all items including gasoline; a key inflation measure) coming in at 4.7% for October 2021 – the highest rate since 2003(1).

This is certainly notable, as the Bank of Canada typically targets inflation of 2% over the medium term with its target range being 1-3%(2). In recent years, inflation has hovered at the low end of that range.

Canadian Consumer Price Index (CPI), Monthly 12-Month Percentage Change Data (2016-2021)

Source: Statistics Canada, October 2021

As inflation creeps up, many investors ask what can be done to preserve the long-term value of their assets. Gold is often cited as an asset which provides inflation-hedging characteristics but farmland is increasingly being recognized as having similar characteristics while experiencing less volatility and historical downside protection(3).

Canadian Farmland as an Inflation Hedge

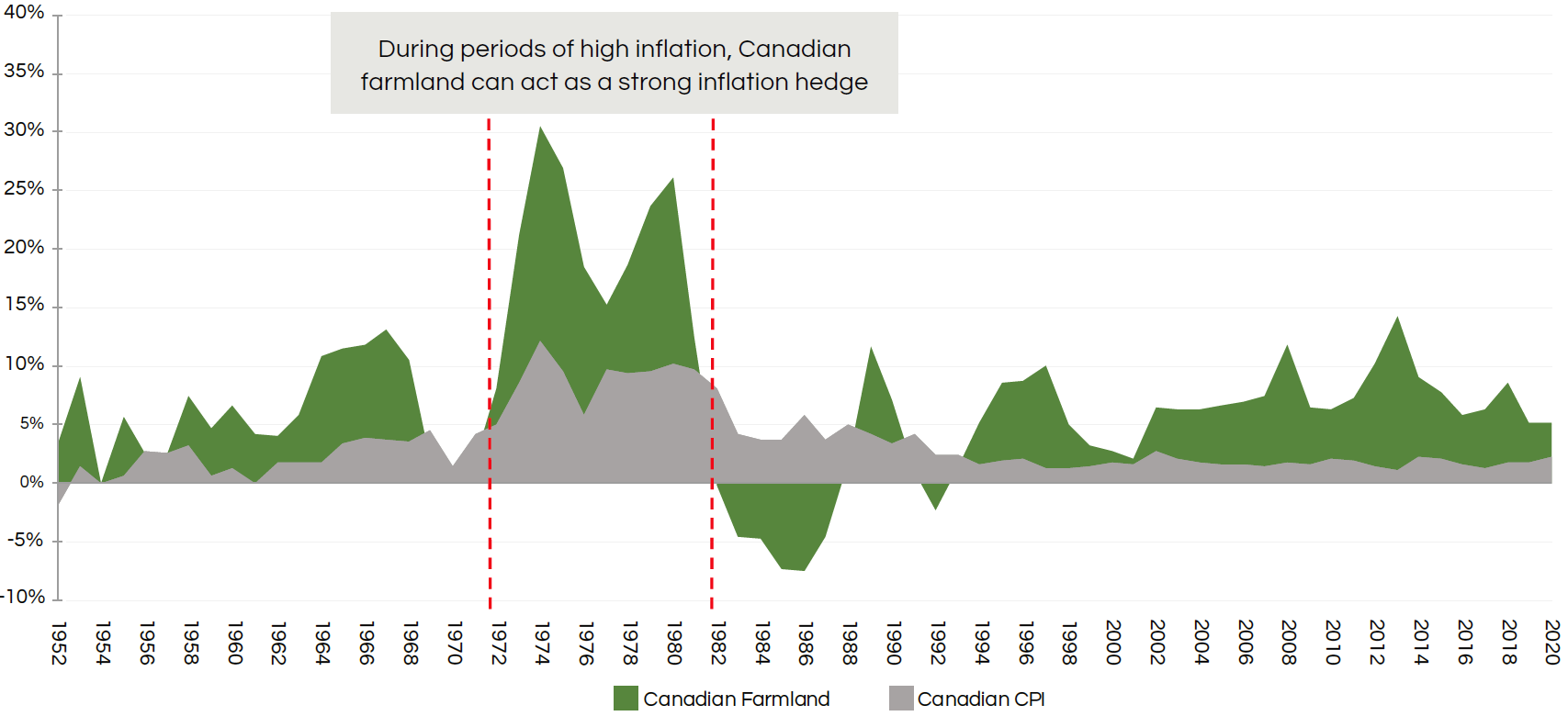

Canadian farmland values have historically demonstrated a strong positive correlation to inflation, as measured by the Canadian Consumer Price Index (CPI), with the relationship being particularly notable in years of high inflation. Between 1952 and 2020, when Canadian CPI rose between 1% and 3% year-over-year, the average year-over-year change in Canadian farmland values was approximately 7%. However, when Canadian CPI increased 5% or more, the average change in Canadian farmland values year-over-year was significantly higher at approximately 16%(4).

This relationship between inflation and farmland values can largely be explained by increasing commodity prices and the dynamic created by increasing global demand for food, driven by continued global population growth and an inherently limited supply of arable land. Simply put, commodity inflation generally increases farm incomes, and as farm incomes increase, so too do farmland values.

We note that in the late 1980s, farmland prices did not increase in line with inflation due to some unique features of the time period. Total absolute debt levels in the Canadian agricultural sector increased at a compound annual growth rate of approximately 15% between 1973 and 1981(5) as farmers took on debt to fund real estate purchases as land values continued to rise. Then, between the late 1970s and early 1980s, we saw rapidly increasing, high interest rates to control inflation, with the Bank Rate reaching as high as 21% in August 1981 (compared to approximately 10% in August 1980)(6). The high interest rates of the early 1980s affected farmland values by decreasing the affordability of traditional loans, including agricultural financing which resulted in a wave of farmers (particularly in Western Canada) entering into insolvency.

The unique confluence of factors that led to a compression of farmland values in the mid- to late 1980s has not recurred since. While there has been some fluctuation, total Canadian farm sector debt levels have generally grown at much more modest levels from the early 1990s onward(7), and interest rates have remained at historic low levels for over a decade.

Historical Canadian CPI and Canadian Farmland Values (1952-2020)

Source: Statistics Canada.

Note: Data represents annual changes from December 1952 – December 2020 in Canadian farmland values and annual change in Canadian CPI. Farmland year over year return data represents land values only.

The current environment seems to be playing out differently compared to the 1980s, with guidance from most central banks remaining accommodative. In its most recent Monetary Policy Report, the Bank of Canada indicated that it expects CPI inflation to ease in 2022 as pandemic-related disruptions to supply gradually begin to fade[7], and appears to be committed to maintaining the policy rate at the lower end to continue stimulating the economy(8).

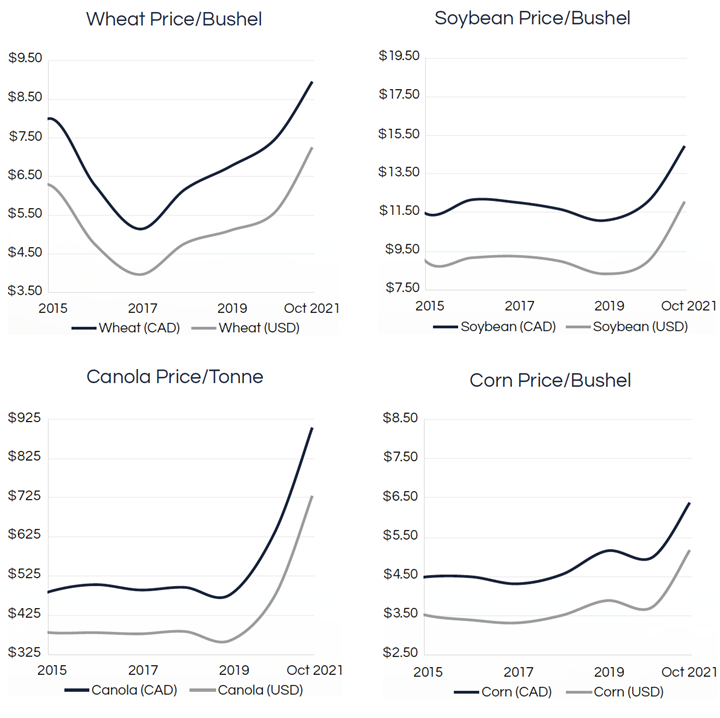

Finally, we anticipate continued strength in market prices for Canada’s key agricultural commodities (wheat, soy, canola, and corn).

Key Agricultural Commodity Prices (2015-2021)

Source: Bank of Canada, Bloomberg News, Grain Farmers of Ontario, ICE Data, OMAFRA.

Strong market prices for these commodities, like the multi-year highs observed in 2021, can translate directly into increased farm incomes that leave farm operators with more cash on-hand and contribute to strong activity in the Canadian farmland market.

Recent Trends in Farmland Values

Farmland is a long-term asset class with limited transaction windows as farmers typically do not buy or sell farmland between seeding in the spring and harvest in late fall. As such, we typically expect values to lag broad market conditions and do not look to quarterly updates as fully reflective of future performance. With that said, as an active farmland owner across Canada, Bonnefield is seeing high and increasing demand for land in some premium farmland regions, supporting strong farmland values.

Farm Credit Canada (FCC) reported in late September 2021 that, despite drought conditions that affected Western Canada during the summer months and a relatively slow overall economic recovery from the COVID-19 pandemic, strength in key commodity prices and the prolonged low interest rate environment continued to support both strong demand and increased prices for Canadian farmland. FCC reported an average year-over-year increase in Canadian farmland values across all provinces of 6.1% as of July 2021, with a notable 15.4% year-over-year increase in farmland values in Ontario, which is home to many of the country’s prime farming regions(9).

Bonnefield’s internal analysis based on third-party appraisals of our properties as well as interactions with industry stakeholders support the themes highlighted in the FCC report. In Western Canada, appraisers noted property value increases of 3-10% in Manitoba, 5-10% in Saskatchewan, and 3-6% for irrigated farmland in Alberta, year-to-date in 2021. In Eastern Canada, we have seen increases in appraised values of between 2-5% in the Maritimes and Northern, Central, and Eastern Ontario. Like data from FCC, our own experience supports the view that high demand among farm operators for land in Southwestern Ontario is resulting in increases to farmland values of upwards of 10%. We note that the overwhelming majority of transactions that we see in the Canadian market occur farmer-to-farmer with prices reflecting farm operator sentiments for future farm incomes and land value appreciation.

Unlike gold, Canadian farmland values appear to be driven by real returns that drive farm profitability. This supports farmland’s role as an attractive asset class for investors looking to benefit from positive long-term value appreciation that outpaces inflation.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction in which an offer or solicitation is not authorized. Any such offer is made only pursuant to relevant offering documents and subscription agreements. Bonnefield funds (the “Funds”) are currently only open to investors who meet certain eligibility requirements. The Funds will not be approved or disapproved by any securities regulatory authority. Prospective investors should rely solely on the Funds’ offering documents which outline the risk factors in making a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax consequences from an investment in the Funds. The Funds are intended for sophisticated investors who can accept the risks associated with such an investment including a substantial or complete loss of their investment.

Those who follow the agricultural industry will be aware of the increasing attention that agriculture technology (AgTech) firms are receiving, and with it, significant investment dollars. In fact, one of Canada’s largest institutional investors, the Ontario Teachers’ Pension Plan (OTPP) recently made its first AgTech investment through its venture capital arm, Teachers’ Innovation Platform. With the spotlight on the AgTech industry, we wanted to review the role that technology has played in agriculture and explore how ongoing innovation can drive industry performance through the lens of a farmland owner / investor.

Technology in Agriculture: A Driver of Productivity & Farmland Values

Innovation and technological advancements in agriculture have been around for as long as farming itself. The search for increased efficiency to meet growing consumer demands is not going away and significant technological advancements have been made in the agriculture industry over the past several decades. Today, technologies such as GPS Guidance for farming equipment and Site-Specific Crop Management practices allow farmers to be more precise and efficient in crop production. As a farmland owner, this raises a key question: how do technological advancements affect producer income and subsequently, farmland values?

For a conventional crop producer, farm income is a function of underlying commodity prices, expected crop yields, and the cost of crop production. Commodity prices are determined by the global market and, while producers can use certain marketing strategies to help reduce risk, individual producers cannot ultimately influence commodity prices. As such, farm operators looking to improve productivity, and thus profitability, can be better served by finding ways to boost crop yields and lower production costs to increase income.

Since farm incomes are a key driver of farmland value, the result of sustainable increases in overall farm profitability can be seen through appreciation of farmland values, making new advancement in AgTech interesting for not only the farm operator but the farmland investor as well.

Examples of AgTech Areas of Focus

Plant Breeding

While longer growing seasons resulting from climate change certainly play a role in increasing crop yields in certain geographies, advances in agricultural technology are also widely acknowledged as being a major driver of improved yields. Notably, there have been significant advancements in plant science and breeding over the past 30 years. Varieties of certain key crops, such as corn, soybeans, and canola can be engineered to mature over a specific number of growing days to accommodate local growing conditions and allow farmers to plan for crop maturity at desired times, or to be more resilient against certain diseases. This allows farmers to select and seed optimal plant varieties that are best suited to their location and the characteristics of their land.

Precision Agriculture

Precision agriculture (also referred to as Site Specific Crop Management) uses aerial and satellite imagery, weather data, and crop health indicators to enable farmers to be more exact in the planting of seeds and the application of fertilizer. For example, variable-rate fertilizer application allows producers to apply the ideal amount of fertilizer to different regions of a single field to maximize crop health and avoid unnecessary overuse of fertilizer. Beyond increasing crop yields, this technology also has considerable benefits from an environmental perspective as it reduces the overall amount of fertilizer required thus preserving supply and limiting unnecessary run-off. Other technologies, such as GPS guidance, have allowed for more accurate planting of crops and fewer wasted acres.

Larger, More Efficient Machinery

Technological advancements have also created significant cost savings in agriculture, and farming operations are larger and more efficient than ever. This is made possible by new technologies such as the large machines that allow producers to plant, fertilize, and harvest greater acreage in less time. Today, large tractors with planting implements spanning over 60 feet in width can cover over 300 acres in a single day, whereas the smaller 15-foot no-till drills of the past would have taken more than four days to cover the same amount of land.

What This Means for Farmland Values

Technological advancements have helped producers to increase yields, reduce costs and have ultimately had a positive impact on farm income and farmland values. As noted in our Q1 newsletter, there has been much excitement in the Canadian farmland market in the first half of 2021, attributable to commodity prices rising to multi-year highs, low transactional activity in 2020, and the prolonged low interest rate environment. However, these factors are cyclical and can shift in a relatively short period of time. In contrast, activities by farm operators and the agriculture sector as a whole, to develop and implement new technologies, increase yields, manage costs, and reduce their environmental footprints are something we believe will support the ongoing capital appreciation of Canadian farmland.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

We are often asked what sets Bonnefield apart as a leading Canadian farmland manager. While there are many qualities that come to mind (our strong 10+ year track record, institutional quality reporting and administration, and our sale-leaseback model that attracts leading farm partners, just to name a few), diversification is one of the most obvious.

Geographic diversification has been a central theme in Bonnefield’s investment thesis since the firm’s inception over a decade ago. As Canada’s leading farmland investment manager, we invest in more Canadian provinces than any other Canadian agriculture-focused asset manager. We apply a granular approach to diversification, investing in over 30 unique growing regions across the country, and ensuring portfolio diversification across multiple climatic regions, crop types and tenant relationships.

Assessing Risk & Return: Sharpe Ratio Analysis

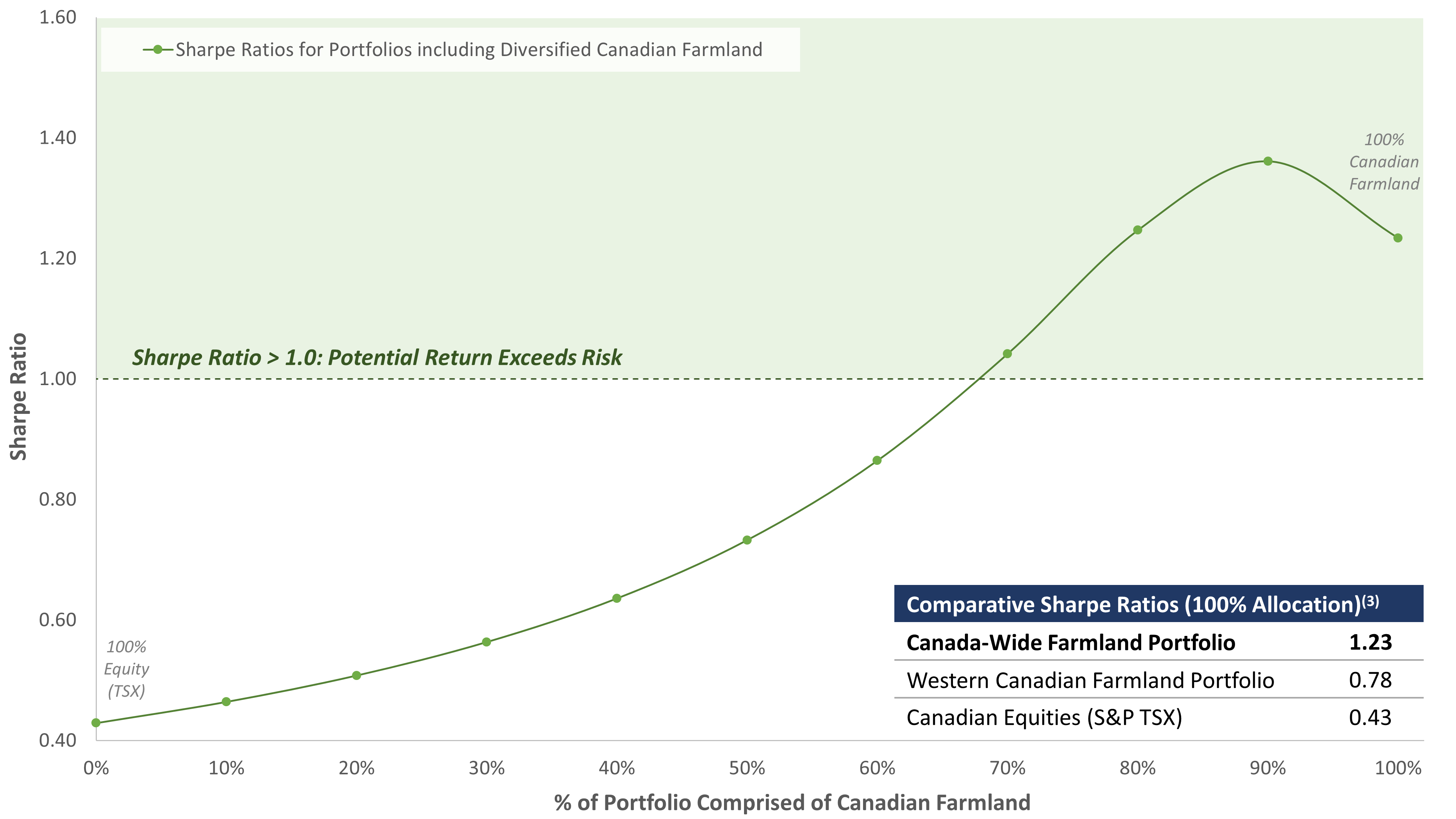

To illustrate the value of diversification in an investment portfolio, we conducted a Sharpe ratio analysis(1) using historical Canadian farmland values between 1985-2019. This type of analysis is a staple of portfolio management theory and a relative measure of the trade-off between risk and return. A higher Sharpe ratio typically suggests a higher potential return per unit of risk taken on and therefore, many investors focus on improving / maximizing the Sharpe ratio of their portfolios.

Risk-Return Profile: Diversified Canadian Farmland in a Portfolio (Sharpe Ratio Analysis)(2)

The first takeaway from this analysis is the positive impact on the Sharpe Ratio as a result of increasing the allocation to Canadian farmland (regardless of its diversification) as opposed to holding only publicly traded equity. With its historically stable return profile, Canadian farmland reduces the volatility of returns and, therefore, improves the Sharpe ratio.

The second takeaway is the relative benefit of holding a portfolio with greater diversification amongst its farmland holdings. As seen in the chart above, portfolios consisting of farmland diversified across most provinces in Canada (Bonnefield currently invests in BC, AB, SK, MB, ON, NB, and NS) demonstrate higher Sharpe ratios, indicative of a favourable risk‐return trade-off, compared to those with farmland limited to only the prairie provinces. This illustrates the relative benefits of maximizing potential diversification within the farmland portfolio.

As noted in our Q1 2020 Newsletter, the Canadian agricultural community has been optimistic since the beginning of 2021 given:

The backdrop of increased feed demand from China;

The reduced crop supply from Brazil and Argentina; and

The Russian export tax on wheat.

Combined with a prolonged period of low interest rates, relatively low transactional activity for Canadian farmland in 2020, and the current multi-year high commodity prices for key crops, we continue to believe that Canadian farmland values are poised for an exciting period of strong growth.

As investors explore the benefits of Canadian farmland within their investment portfolios, we encourage them to consider the relative value of exposure to a well-diversified farmland portfolio to minimize volatility and maximize your potential risk-adjusted returns.

About Bonnefield Financial

Bonnefield is the foremost provider of land-lease financing for farmers in Canada. Bonnefield is dedicated to preserving farmland for farming, and the firm partners with growth-oriented farmers to provide farmland leasing solutions to help them grow, reduce debt, and finance retirement and succession. The firm’s investors are individuals and institutional investors who are committed to the long term future of Canadian agriculture. www.bonnefield.com

(1) Sharpe ratios represent a relative measure potential returns compared to potential risk of an investment, and are calculated by dividing i) the excess return above a selected risk-free rate (i.e., average historical rate of return for an asset/investment less a risk-free rate such as the prevailing rate for a Government or Treasury-issued instrument) by ii) the standard deviation of those historical returns.

(2) Analysis contemplates hypothetical portfolios balanced between i) Canadian equities (S&P TSX index) and ii) Statistics Canada farmland values (weighted equally between selected provinces; Bonnefield’s investment provinces include BC, AB, SK, MB, ON, NS, and NB), between 1985 and 2019.

(3) Noted Sharpe ratios assume 100% allocation of a hypothetical portfolio to each of i) Canadian farmland in Bonnefield’s investment provinces, ii) Canadian farmland in AB/SK/MB only, and iii) Canadian equities (S&P TSX index).

Over the past decade, we have seen increased interest among the investment community in agriculture and farmland as an asset class. Not only are large, sophisticated, institutional investors across the globe evaluating (or already invest in) farmland and agricultural investments, so too, are increasing numbers of non-institutional investors.

Click here to read an article by Bonnefield’s Andrea Gruza that explores how farmland investments provide investors with a diversifying asset with strong ESG characteristics, climate change hedging capabilities and potential to support a move towards a net zero investment portfolio.

(Original article published in the spring 2021 edition of Radius European Investment Journal.)